A Look Back at Q4 '22 Public Cloud Software Earnings

Q4 earnings season for cloud businesses is now behind us. The 63 companies that I’ll discuss here (which is not an exhaustive list, but is still comprehensive) all reported quarterly earnings sometime between January 25th – March 30th. In this post, I’ll take a data-driven approach in evaluating the overall group’s performance, and highlight individual standouts along the way. As a venture capitalist, I naturally cater my analysis through the lens of a private investor. Over my years as a VC, I’ve had the opportunity to meet with hundreds of entrepreneurs who are all building special companies. Through these interactions, I’ve built up mental benchmarks for metrics on which I place extra emphasis. My hope is that this analysis can provide startup entrepreneurs with a framework for how to manage their businesses around SaaS metrics (e.g., net retention and CAC payback).

When Will Macro Improve?

The last few quarterly earnings recaps have followed a similar trend - performance getting worse. You can see this in the two charts below. Fewer companies are beating consensus estimates, and the magnitude of the median beat has gone down from ~5% to ~2.5% (first chart). At the same time, forward guides are also weakening. Less than half of the software universe is guiding above consensus, and the median guide has gone from ~2.5% above consensus to ~1% below consensus (second chart). Said another way - despite weak guides, companies aren’t beating estimates

The natural question - when will the market improve? When I look at the below graphic from the latest Morgan Stanley CIO survey I see signs that the market is starting to stabilize (not improve, but not getting worse). For the prior 3 quarters, the number of CIOs expecting downward budget revisions was increasing. In this last quarter, it stayed steady. However, there are still more CIOs who expect downward budget revisions vs upward, but the number expecting upward revisions ticked up, while the number expecting downward revisions stayed the same. Maybe this is the first hint that the market will get better soon?

On the other hand, the economy still feels like it’s on the brink of a larger recession. If we do fall into a deeper recession, we will definitely see a change in the above graphic in future surveys (red bar getting bigger). This moment in time feels either like the calm before the storm, or the stabilization period before things get better (unemployment continues to stay low). We’re undoubtedly set up for a very interesting 2023. Let’s now jump in to the Q4 ‘22 earnings recap.

Q4 Top Performers

If you don’t have time to read the rest of this article, here are the companies who I believe really stood out (from a financial perspective). They represent my “Q4 Top Performers.” This is not an indication of who I think will preform the strongest in the future, but a look-back on who preformed the best in Q4 (based on a formula I use that factors in many different financial variables)

Q4 Revenue Relative to Consensus Estimates

Now let’s dive in to the financial results of Q4 starting with revenue. Beating consensus revenue estimates is the first aspect of a successful quarter. So what are these consensus estimates and who creates them? Every public company has a number of equity research analysts covering them who build their own forecasted models, which combine guidance from the company and their own research / sentiment analysis. The consensus estimates are the average of all the individual analysts’ projections. Generally when you hear “consensus estimates” it refers to revenue and earnings (EPS), but for the purpose of this analysis we’ll just be looking at revenue consensus estimates (as this is the metric these companies are valued off). For every public company the expectation is that they’ll beat consensus estimates, because companies often guide research analysts to the lower end of their internal projections. They do this to set themselves up to consistently beat estimates, demonstrating momentum.

As you can see from the data below most cloud businesses beat the consensus estimates for Q4.

Historically, the median beat of consensus estimates is closer to ~4%. As you can see, the median beat this quarter was 2.8%. So we didn’t see big beats off of weak guidance last quarter.

Next Quarter’s Guidance Relative to Consensus Estimates

Guiding above next quarter’s consensus revenue estimates is the second factor for a successful quarter. Generally, companies will give a guidance range (e.g., $95M -$100M), and the numbers I’m showing are the midpoint. Providing guidance that is greater than consensus estimates is a sign of improving business momentum, or confidence that the business will perform better than previously expected. The concept of guiding higher than expectations is considered a “raise.” When you hear the term “beat and raise” the beat refers to beating current quarter’s expectations (what we discussed in the previous section), and the raise is raising guidance for future quarters (generally it’s annual guidance, but for this analysis we’re just looking at the next quarter’s guidance).

This quarter more than half of cloud software businesses missed next quarters consensus. This is quite interesting. At the same time, the median guidance was 1.1% UNDER consensus

Historically, the median guidance “raise” was in the 2-3% range. This is the second quarter in a row where the median was <0%. The below chart shows what the median guidance raise was in the last 11 quarters. As you can tell, it’s been coming down.

Growth

Demonstrating high growth is the third aspect of a successful quarter. This metric is more self-explanatory, so I won’t go into detail. The growth shown below is a year-over-year growth for reported quarters. The formula to calculate this is: (Q4 ’22 revenue) / (Q4 ’21 revenue) - 1. One call out - Alteryx grew GAAP revenue >70% this year, but ARR grew 31%. ARR is more representative of how the business is preforming, so I’m snowing ARR growth for them below

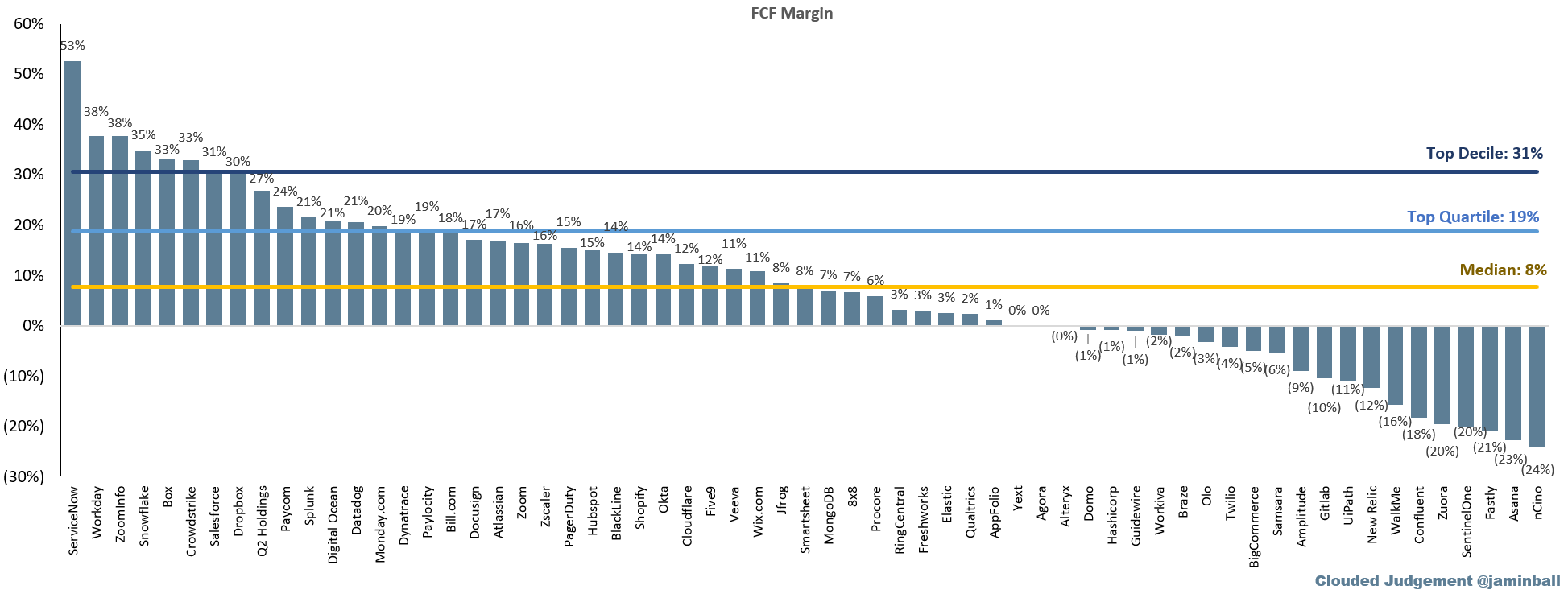

FCF Margin

FCF is an important metric to evaluate in SaaS businesses. Profitability is often the big knock against them, however many generate more cash than you might imagine. I’m calculating FCF by taking the Operating Cash Flow and subtracting CapEx and Capitalized Software Costs. The big caveat in FCF – it adds back the non-cash expense of SBC. This is controversial, as it harms shareholder returns by increasing the number of shares outstanding over time (dilution). This matters a lot more when stock prices are going down, and management teams often grant additional shares to make employees whole (thus increasing dilution even more)

Net Revenue Retention

High net revenue retention is the fourth aspect of a successful quarter, and one of my favorite metrics to evaluate in private SaaS companies. It is calculated by taking the annual recurring revenue of a cohort of customers from 1 year ago, and comparing it to the current annual recurring revenue of that same set of customers (even if you experienced churn). In simpler terms — if you had 10 customers 1 year ago that were paying you $1M in aggregate annual recurring revenue, and today they are paying you $1.1M, your net revenue retention would be 110%. The reason I love this metric is because it really demonstrates how much customers love your product. A high net revenue retention implies that your customers are expanding the usage of your product (adding more seats / users / volume - upsells) or buying other products that you offer (cross-sells), at a higher rate than they are reducing spend (churn).

Here’s why this metric is so significant: It shows how fast you can grow your business annually without adding any new customers. As a public company with significant scale, it’s hard to grow quickly if you have to rely solely on new customers for that growth. At $200M+ ARR, the amount of new-logo ARR you need to add to grow 30%+ is significant. On the other hand, if your net revenue retention is 120%, you only need to grow new logo revenue 10% to be a “high growth” business.

I’ve looked at thousands of private companies, and over time have come up with benchmarks for best-in-class, good, and subpar net revenue retention. Not surprisingly, these benchmarks match up relatively well with the numbers public companies reported. I generally classify anything >130% as best in class, 115% — 130% as good, and anything less than 115% as subpar. For businesses selling predominantly to SMB customers, these benchmarks are all slightly lower given the higher-churn nature of SMBs. I consider >120% best in class for companies selling to SMBs (like Bill.com). Here’s the data from Q4:

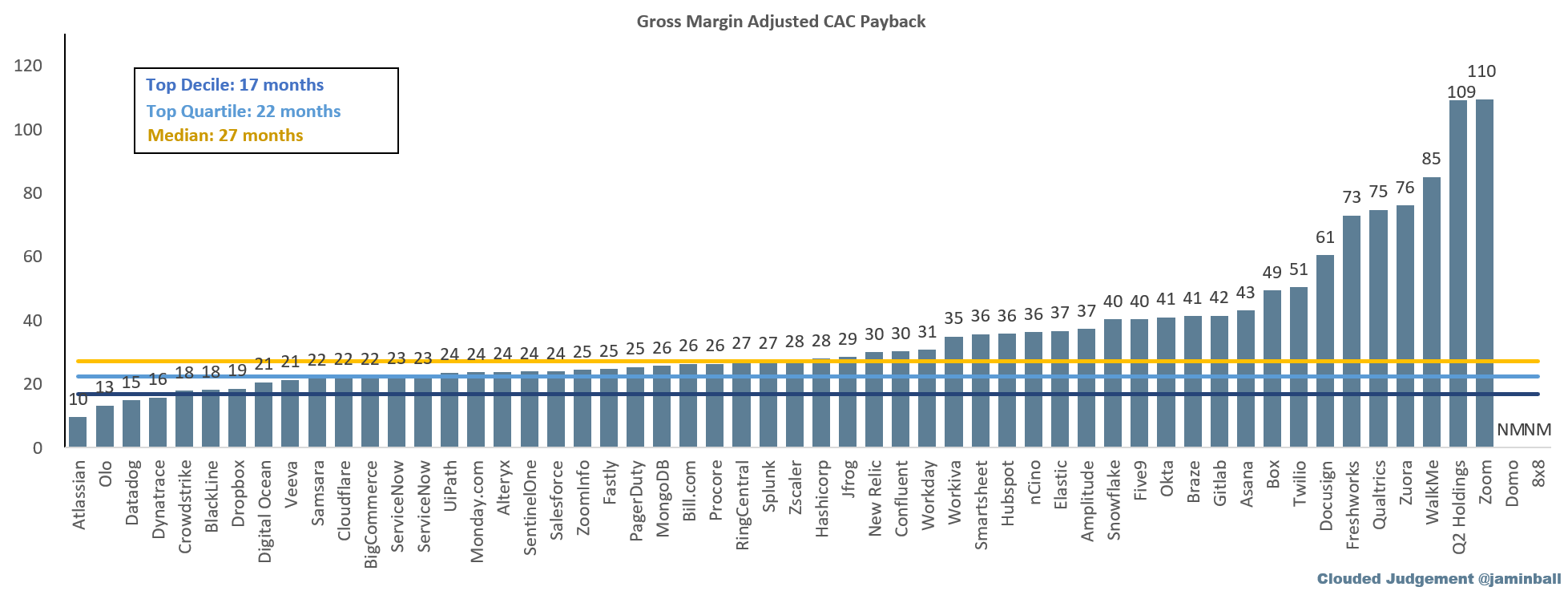

Sales Efficiency: Gross Margin Adjusted CAC Payback

Demonstrating the ability to efficiently acquire customers is the fifth aspect of a successful quarter. The metric used to measure this is my second-favorite SaaS metric (behind net revenue retention) : Gross Margin Adjusted CAC Payback. It’s a mouthful, but this metric is so important because it demonstrates how sustainable a company’s growth is. In theory, any growth rate is possible with an unlimited budget to hire AEs. However, if these AEs aren’t hitting quota and the OTE (base + commission) you’re paying them doesn’t justify the revenue they bring in, your business will burn through money. This is unsustainable. Because of the recurring nature of SaaS revenue, you can afford to have paybacks longer than 1 year. In fact, this is quite normal.

All that said, Gross Margin Adjusted CAC Payback is relatively simple to calculate. You divide the previous quarter’s S&M expense (fully burdened CAC) by the net new ARR added in the current quarter (new logo ARR + Expansion - Churn - Contraction) multiplied by the gross margin. You then multiply this by 12 to get the number of months it takes to pay back CAC.

(Previous Q S&M) / (Net New ARR x Gross Margin) x 12

A simpler way to calculate net new ARR is by taking the current quarter’s ARR and subtracting the ending ARR from one quarter prior. Similar to net revenue retention, I’ve built up benchmarks to evaluate private companies’ performance. I generally classify any payback <12 months as best in class, 12–24 months as good, and anything >24 months as subpar. The public company data for payback doesn’t match up as nicely with my benchmarks for net revenue retention. The primary reason for this is that public companies can afford to have longer paybacks. At $200M+ ARR, businesses have built up a substantial base of recurring revenue streams that have already paid back their initial CAC. Their ongoing revenue can “fund” new logo acquisition and allow the business to operate profitably at paybacks much larger than what private companies (with smaller ARR bases) can afford.

Most public companies don’t disclose ARR (and when they do, it’s often not the same definition of ARR as we use for private companies). Because of this we have to use an implied ARR metric. To calculate implied ARR I take the subscription revenue in a quarter and multiply it by 4. So for public companies the formula to calculate gross margin adjusted payback is:

[(Previous Q S&M) / ((Current Q Subscription Rev x 4) -(Previous Q Subscription Rev x 4)) x Gross Margin] x 12

Here’s the payback data from Q4. Not every company reports subscription revenue, so they’ve been left out of the analysis (or I’ve estimated their % subscription revenue). Some software companies also have seasonality in the “payback.” Because many companies don’t actually disclose ARR I’m calculating a swag of ARR based on subscription rev.

Change in 2023 Consensus Revenue Estimates

Tying all of these metrics together is another one of my favorites: the change in revenue consensus estimates for the 2023 calendar year. Heading into Q4 earnings, analysts had expectations for how each business would perform in 2023. After earnings, that perception either changed positively or negatively. It’s important to look at the magnitude of that change to see which companies appear to be on better paths. Analysts take in quite a bit of information into their future predictions — exec commentary on earnings calls, current quarter results, macro tailwinds / headwinds, etc., and how they adjust their 2023 estimates says a lot about whether the outlook for any given business improved or declined.

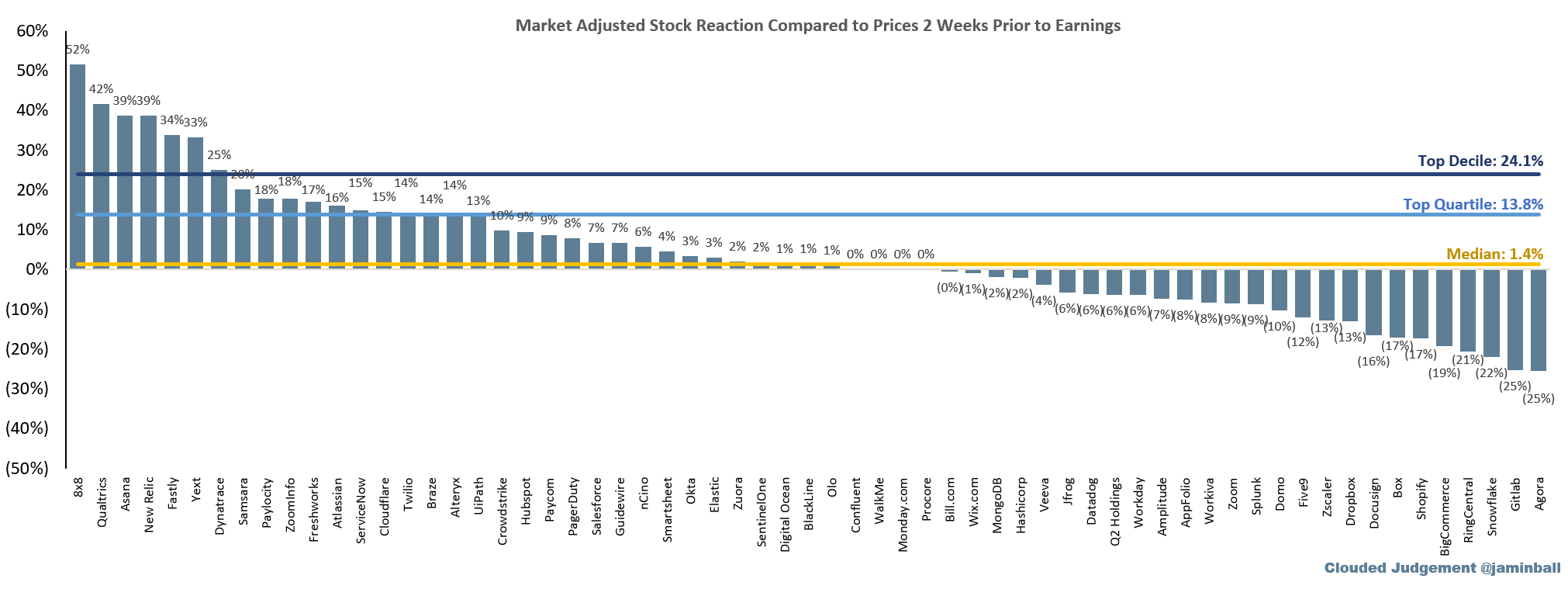

Change in Share Price

At the end of the day what investors care about is what happened to the stock after earnings were reported. The stock reaction alone doesn’t represent the strength of a company’s quarter, so the below data has to be viewed in tandem with everything discussed above. Oftentimes the buy-side expects a company to perform well (or poorly), and the company’s stock going into earnings already has these expectations baked in. In these situations the stock’s earnings reaction could be flat. However, it’s still a fun data point to track.

What I’ve shown below is the market-adjusted stock price reaction. This means I’ve removed any impact of broader market shifts to isolate the company’s earnings impact on the stock. As a hypothetical example: Let’s say a day after Qualtrics reported earnings their stock was up 4%. However the market that day (using the Nasdaq as a proxy) was up 1%. This implies that even without earnings Qualtrics would likely have been up 1%. To calculate the specific impact of earnings on the stock we need to strip out the broader market’s movement. To do this we simply subtract the market’s movement from the stock’s movement: (% Change in Stock) - (% Change in Nasdaq)

However, some of this data can be quite misleading. Many of the companies saw a big change in their stock prices leading up to earnings. Either a run up, or a draw down from market factors. In the below graph I’m looking at how the stock compared to 2 weeks prior to earnings. The data is below:

Wrapping Up

This quarter has been a wild ride for SaaS businesses. Multiples have compressed significantly back below historical averages as rates have gone up.

Here’s a summary of the key stats for each category we talked about, and how the “Big Winners” performed. Hopefully this provides a blueprint for every entrepreneur out there reading this post on how to preform as an elite public company.

The Data

The data for this post was sourced from public company filings, Wall Street Research and Pitchbook. If you’d like to explore the raw data I’ve included it below. Looking forward to providing more earnings summaries for future quarters! If you have any feedback on this post, or would like me to add additional companies / analysis to future earnings summaries, please let me know!

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Would be nice if you include table like data which can be processed and not a screen shot which is useless for any analysis. Thanks.

Apologies if I got this wrong but for your gross margin CAC Payback formula why are you multiplying by 12 if your S&M and new ARR is quarterly?

For public software companies your formula is using annualized new ARR but using quarterly S&M expense and then multiplying this by 12?