Clouded Judgement 1.10.25 - Rising Rates

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Rising Rates

The 10Y is up to 4.7%. When the Fed started cutting the fed funds rate in September ‘24, the 10Y was at 3.7%. So while the Fed is cutting rates, the 10Y is rising! This might seem odd at first, but there are some pretty clear reasons why this is happening. Here’s what’s going on:

Higher Inflation Expectations

One big reason the 10Y is climbing is that people are expecting inflation to stick around. Even with the Fed’s rate cuts, prices haven’t really cooled off. Wages have been growing at over 4% year-over-year, showing how tight the labor market still is. Plus, oil prices have bounced back, with Brent crude topping $90 a barrel, which makes everything from transportation to manufacturing more expensive. And while supply chain issues aren’t as bad as they were a couple of years ago, some sectors are still feeling the pinch. All this adds up to investors wanting higher yields on long-term bonds to make up for the bite inflation takes out of their returns.

Strong Economic Growth

The economy has been surprisingly strong, which is another reason the 10Y is up. In Q3 2024, GDP grew at an annualized 3.2%, thanks to consumers who are still spending and businesses that are still investing. On top of that, consumer sentiment is the best it’s been since early 2022, showing that people are feeling pretty good about where things are heading. The job market is also rock solid, with unemployment sticking around 3.6%. When the economy is doing this well, people tend to move their money into riskier investments instead of safe bets like Treasuries, which pushes yields higher. Plus, strong growth makes it less likely that the Fed will cut rates aggressively in the future, adding even more upward pressure on the 10Y.

Trump Tariffs and Supply Chain Costs

Then there are the Trump tariffs, which are back and expected to make an impact. These tariffs hit imports like electronics, machinery, and consumer goods, making them more expensive for U.S. businesses. A 15% tariff on $300 billion worth of Chinese goods could drive up costs for everything from smartphones to industrial equipment. Companies usually pass those higher costs onto consumers, so prices go up across the board. On top of that, the tariffs could mess with supply chains, leading to inefficiencies and higher shipping costs. All of this fuels inflation worries, and when inflation is a concern, investors want higher yields to protect their money over the long haul.

In summary - the rise in the 10Y Treasury yield, even as the Fed is cutting rates, boils down to a few key factors: sticky inflation expectations, strong economic growth, and the inflationary effects of Trump’s tariffs. It’s a reminder that long-term rates aren’t just about what the Fed is doing—they’re also shaped by the bigger economic picture. As investors and policymakers try to navigate these challenges, we’re likely to see even more twists and turns in the bond market.

Quarterly Reports Summary

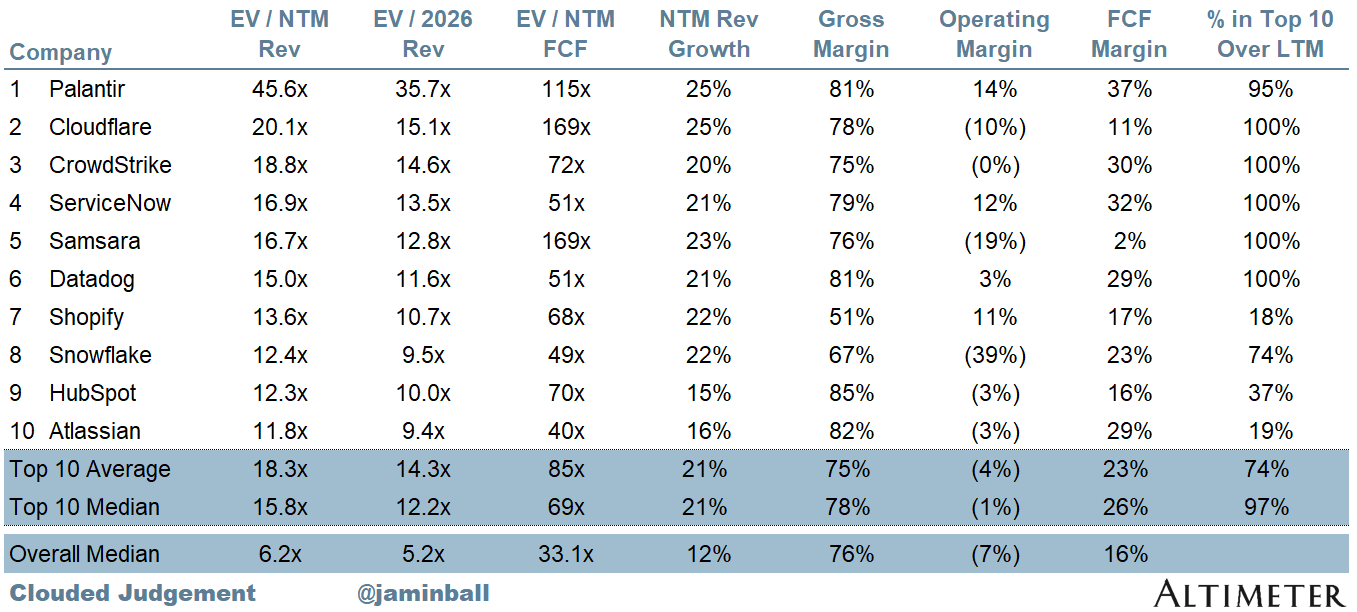

Top 10 EV / NTM Revenue Multiples

Top 10 Weekly Share Price Movement

Update on Multiples

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 6.2x

Top 5 Median: 18.8x

10Y: 4.7%

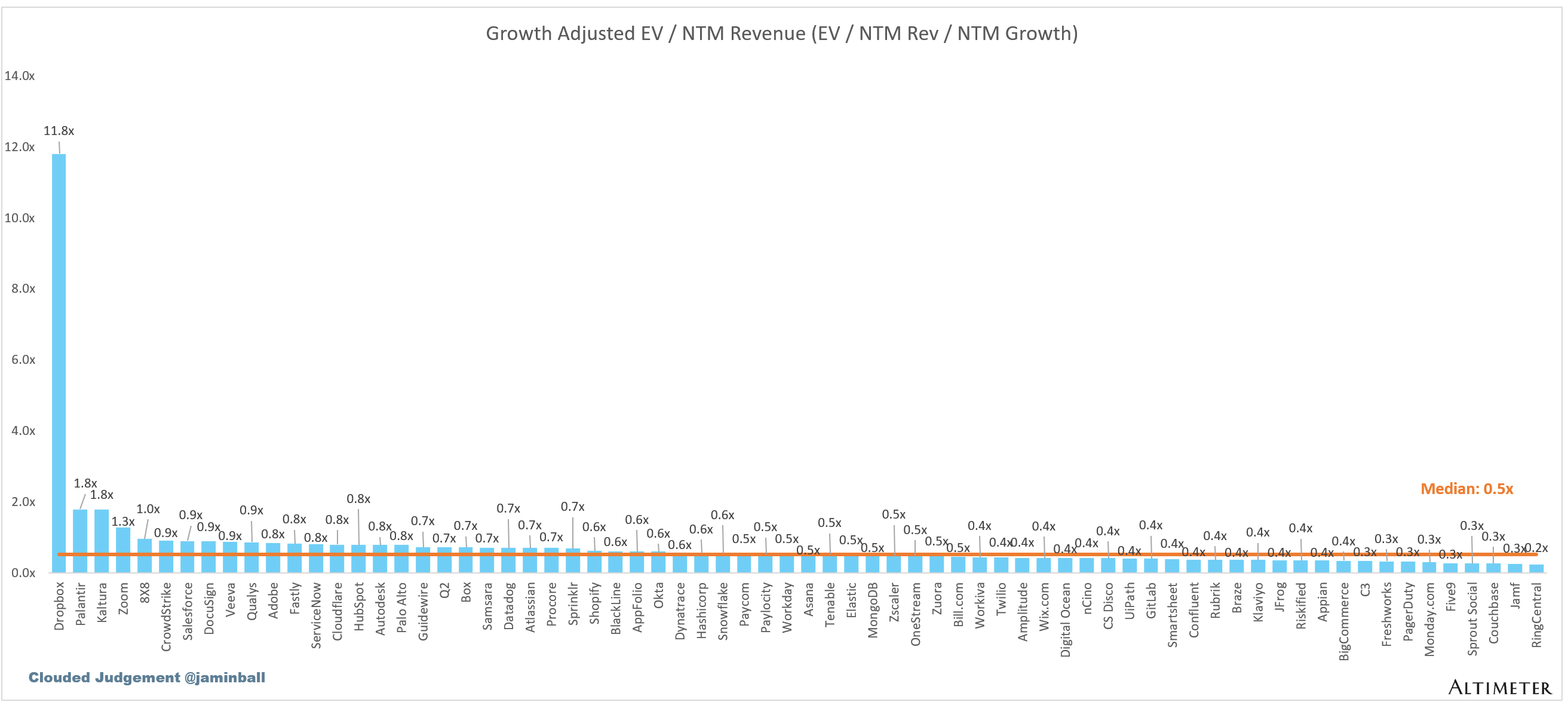

Bucketed by Growth. In the buckets below I consider high growth >27% projected NTM growth (I had to update this, as there’s only 1 company projected to grow >30% after this quarter’s earnings), mid growth 15%-27% and low growth <15%

High Growth Median: 9.6x

Mid Growth Median: 10.4x

Low Growth Median: 4.4x

EV / NTM Rev / NTM Growth

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. So a company trading at 20x NTM revenue that is projected to grow 100% would be trading at 0.2x. The goal of this graph is to show how relatively cheap / expensive each stock is relative to their growth expectations

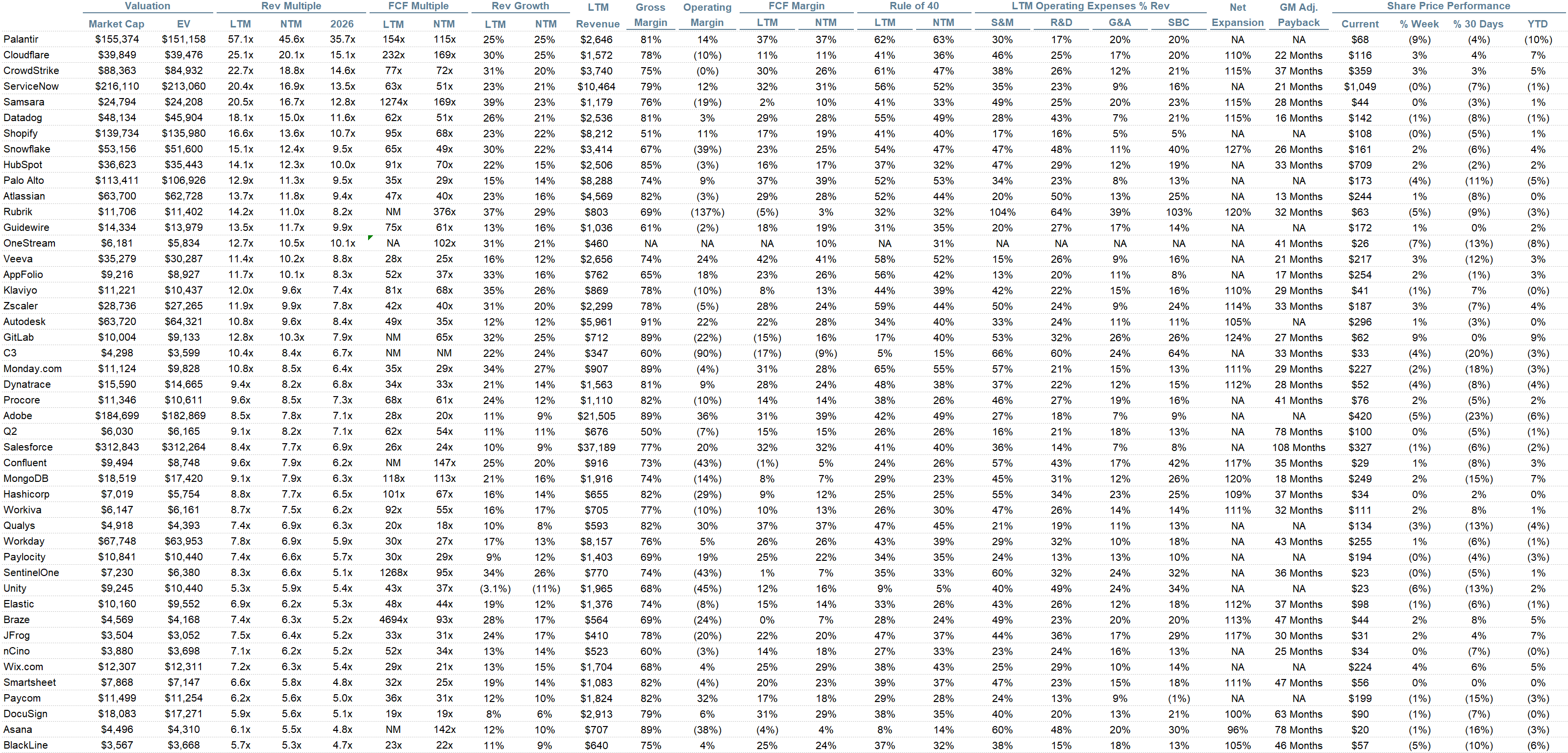

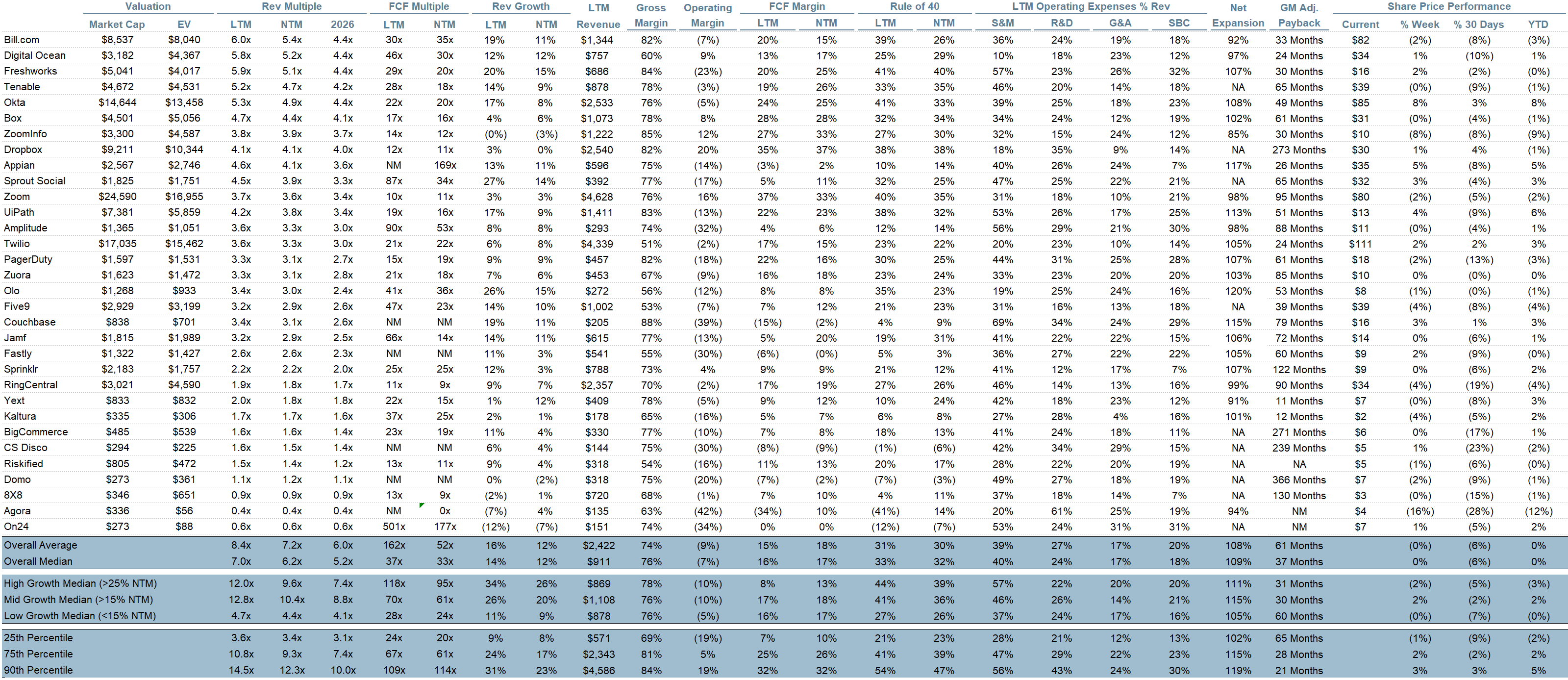

EV / NTM FCF

The line chart shows the median of all companies with a FCF multiple >0x and <100x. I created this subset to show companies where FCF is a relevant valuation metric.

Companies with negative NTM FCF are not listed on the chart

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Operating Metrics

Median NTM growth rate: 12%

Median LTM growth rate: 14%

Median Gross Margin: 76%

Median Operating Margin (7%)

Median FCF Margin: 16%

Median Net Retention: 109%

Median CAC Payback: 37 months

Median S&M % Revenue: 40%

Median R&D % Revenue: 24%

Median G&A % Revenue: 17%

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12 . It shows the number of months it takes for a SaaS business to payback their fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Sources used in this post include Bloomberg, Pitchbook and company filings

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

I'm hoping someone can chime in more on how to think about that adjusted gross margin payback period. It's wild to see that for most companies, it will take 30 months for their gross profit from new ARR added in a specific quarter to exceed the quarterly spend on sales & marketing that quarter? On the surface, it seems like this would be an unsustainable CAC, and positive net income would never be achieved? You used to hear about the rule of 3 back in the day, where the lifetime value of a customer had to be 3X the CAC. If it takes 30 months just for gross profit to equal CAC, would it take 10 years for a customer to generate a lifetime value equal to 3X the CAC?

Is another factor driving the ten year higher the expectation that rates may actually have to be increased in the near future? So might be smart to hold off on buying a T Bill if that is going to happen? Hence treasury has to goose rates to bring them in now.