Clouded Judgement 1.20.23 - Belt Tightening Double Whammy

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Belt Tightening Double Whammy

Had an interesting conversation with some colleagues this week that I wanted to share. We were reflecting on the last couple years in the context of today’s belt tightening. In summary, we viewed the “arc” of the last few years as the following: during Covid, the top down mandate was “modernize.” Digital Transformations were running rampant. This also coincided with a period of cheap capital and low rates. The push to modernize quickly combined with the period of cheap capital lead to sloppy processes. There wasn’t always the appropriate amount of oversight and excess and redundancy was built in everywhere. However, today we’re now in a period of belt tightening - companies are specifically looking for optimizations. Had we not gone through 2020-2022 there would still be excess to remove. However, we did go through that period. So we’re now seeing optimizations from normal belt tightening, and then incremental optimizations to work out the excess from sloppy digital transformation processes from the prior couple years. What does this mean? We could see the reverse effects of Covid pull-forward - a double whammy of belt tightening. We could be in for a rocky year, but then we have commentary like we got from the ServiceNow CEO yesterday. More on that below.

Overall, this year will undoubtedly be the year of dispersion. It’s easy to optimize non-mission critical spend, or spend that can be consolidated elsewhere.

ServiceNow CEO Commentary

Bill McDermott gave an interview this week where he sounded very bullish on the year ahead. This is in contrast to most of the other commentary we’ve heard. You can listen to the full interview in the link above (it’s short, only ~5 minutes). In it he said “we’re very optimistic about 2023…not a chance for an IT recession in 2023…we’re hiring (when asked about a company like Salesforce who just announced a reduction in force).” Overall, he painted a different picture about 2023 than the consensus narrative.

One other interesting chart I came across from Morgan Stanley was their job posting analysis on ServiceNow. Like many trend chats over the last few years, interesting to see the mean reversion going on:

Top 10 EV / NTM Revenue Multiples

Top 10 Weekly Share Price Movement

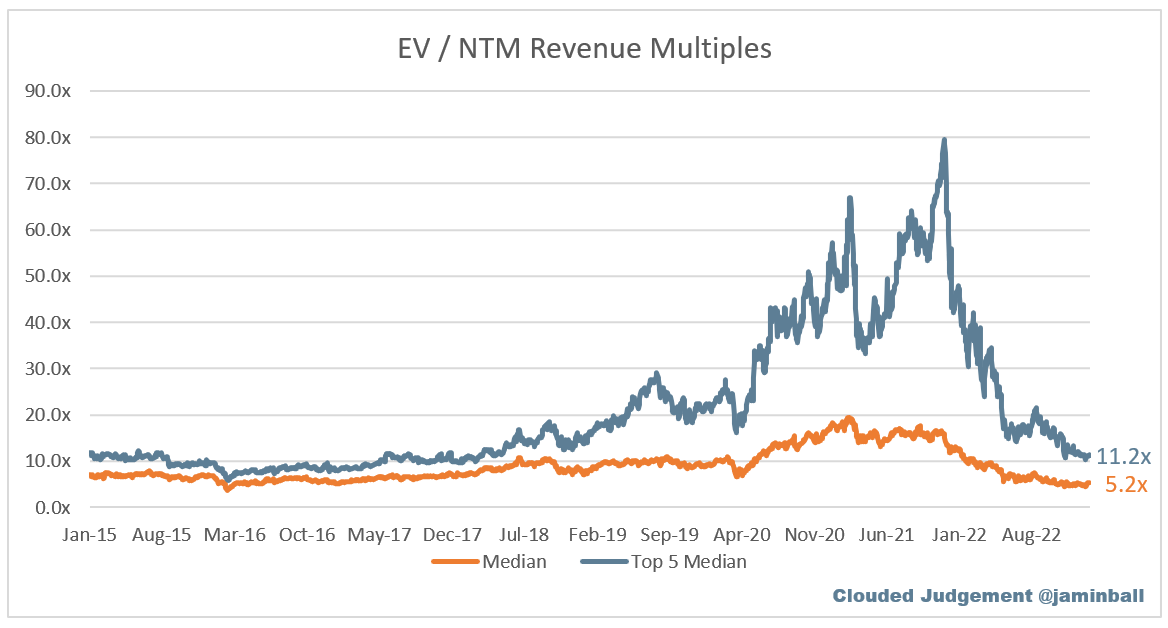

Update on Multiples

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 5.2x

Top 5 Median: 11.2x

10Y: 3.4%

Bucketed by Growth. In the buckets below I consider high growth >30% projected NTM growth, mid growth 15%-30% and low growth <15%

High Growth Median: 9.3x

Mid Growth Median: 5.6x

Low Growth Median: 2.9x

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Growth Adjusted EV / NTM Rev

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. The goal of this graph is to show how relatively cheap / expensive each stock is relative to their growth expectations

Operating Metrics

Median NTM growth rate: 17%

Median LTM growth rate: 29%

Median Gross Margin: 74%

Median Operating Margin (25%)

Median FCF Margin: 0%

Median Net Retention: 119%

Median CAC Payback: 38 months

Median S&M % Revenue: 48%

Median R&D % Revenue: 28%

Median G&A % Revenue: 20%

Comps Output

Rule of 40 shows LTM growth rate + LTM FCF Margin. FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12 . It shows the number of months it takes for a SaaS business to payback their fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Coupa is now a private company. Should you remove it from some of the above analysis, given that it is no longer publicly reporting current financial information?

I’m so glad I found this newsletter. So informative and simple. Love the insights.