I’m writing this weeks edition from Abu Dhabi at 2am, so please excuse any (jet lagged induced) typos. This is my first time in the UAE and it’s been incredible - it’s amazing to see what’s possible with a business friendly government that is massively committed to diversifying their economy. They’re embracing entrepreneurship and it’s clear this region will be (and is already) a major player in the global economy. In business and government, leadership matters!

Earnings Update

So far about half of the cloud software universe has reported Q1 earnings (43 companies in the universe I track). So far 39 have beat Q1 consensus (91%) and 4 have missed. Of the 43 companies to report, 38 gave guidance for Q2. Of those, 20 companies guided Q2 above consensus (53%), and 18 guided below consensus.

The beat / raise trends are slightly better than Q4. In Q4 90% of companies beat consensus estimates (so same as Q1), but only 44% guided ahead of consensus. So we’re seeing a slightly more positive trend in the number of companies guiding above consensus. This is consistent with a lot of the broader commentary on calls that the environment isn’t getting better, but it’s not getting worse.

On a related note - when we look at companies who gave full year 2023 guidance this quarter vs last quarter, on average those companies are not changing their guidance at all (median change in guide is 0%). There are some outliers, but for the universe who’ve reported so far the takeaway is 2023 guides were de-risked. I think it’s unlikely 2023 numbers come down from where they are today. There were a number of companies who beat Q1 who didn’t change full year guidance. It felt like this was a conservative move. As I mentioned last week, the big question now is around 2024 numbers, and if those need to come down. There’s a big question of when the macro headwinds start to ease up, and when we see re-acceleration. The further that gets pushed out, the more likely it is that 2024 numbers will need to come down. The sooner that happens, the more likely 2024 numbers will need to come up.

Quarterly Reports Summary

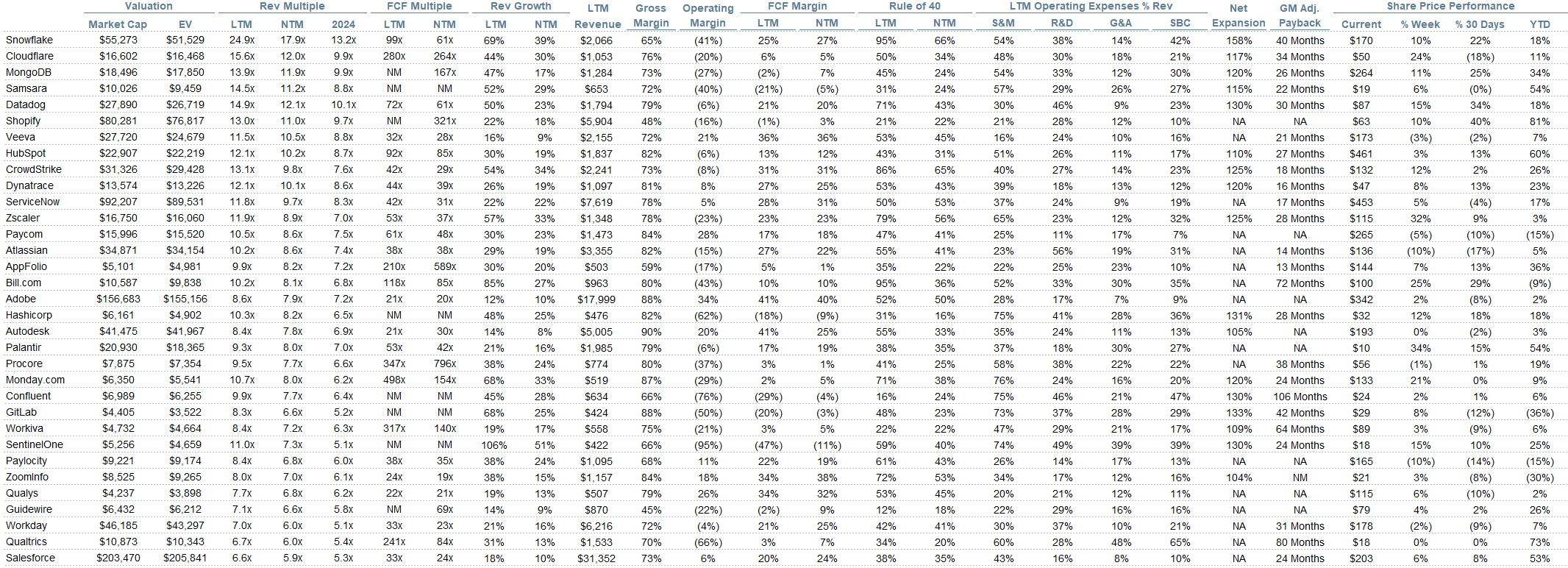

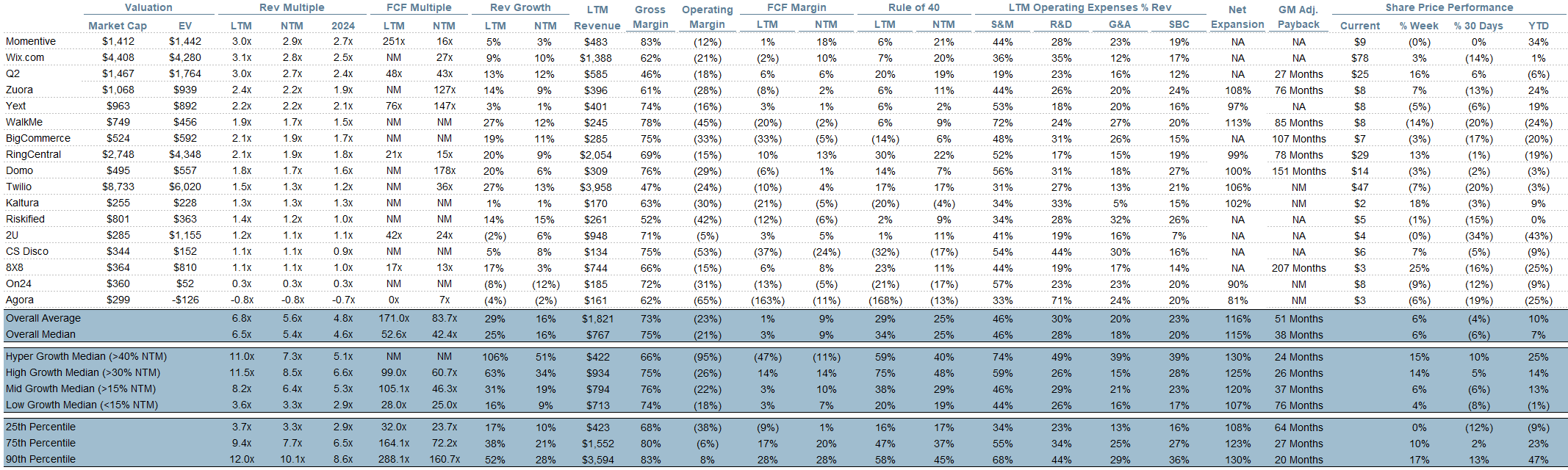

Top 10 EV / NTM Revenue Multiples

Top 10 Weekly Share Price Movement

Update on Multiples

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 5.4x

Top 5 Median: 12.0x

10Y: 3.4%

Bucketed by Growth. In the buckets below I consider high growth >30% projected NTM growth, mid growth 15%-30% and low growth <15%

High Growth Median: 8.5x

Mid Growth Median: 6.4x

Low Growth Median: 3.3x

EV / NTM FCF

Companies with negative NTM FCF are not listed on the chart

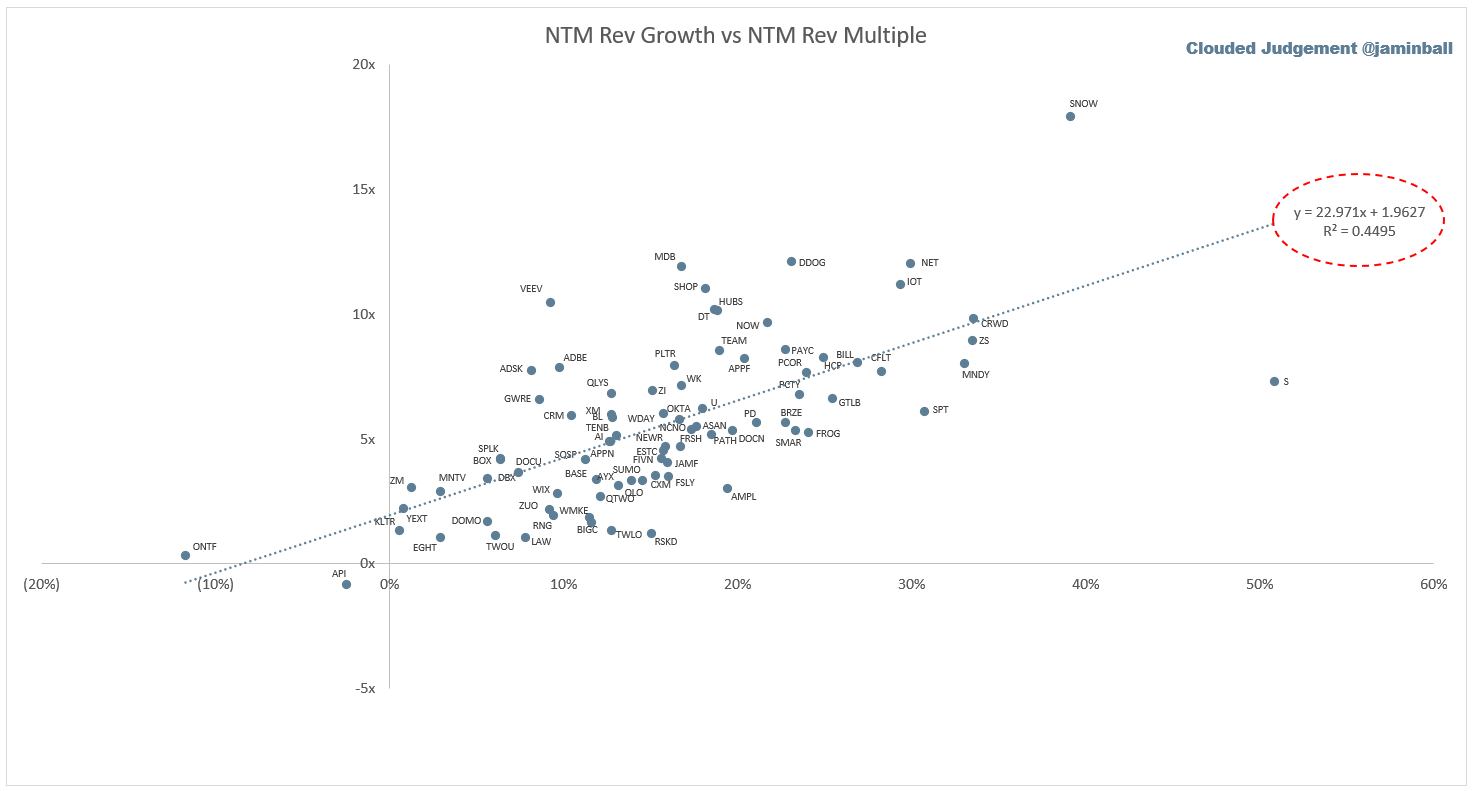

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

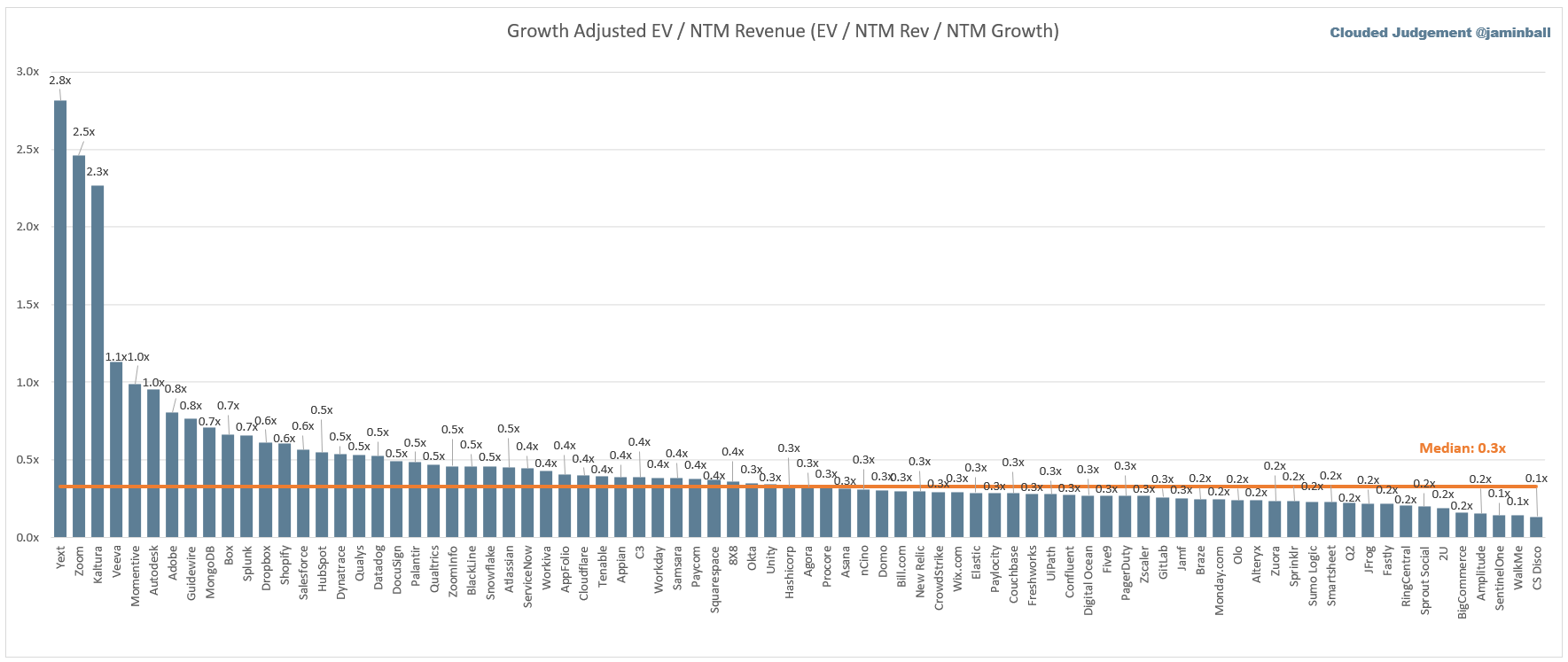

Growth Adjusted EV / NTM Rev

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. The goal of this graph is to show how relatively cheap / expensive each stock is relative to their growth expectations

Operating Metrics

Median NTM growth rate: 16%

Median LTM growth rate: 26%

Median Gross Margin: 75%

Median Operating Margin (21%)

Median FCF Margin: 2%

Median Net Retention: 116%

Median CAC Payback: 30 months

Median S&M % Revenue: 47%

Median R&D % Revenue: 28%

Median G&A % Revenue: 18%

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12 . It shows the number of months it takes for a SaaS business to payback their fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Thanks for regular insightful writeups

Thank you for your brilliant insights Jamin, sir.