Clouded Judgement 6.18.21

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

FOMC

On Wednesday we got commentary from the Federal Open Market Committee (FOMC). This was one of their 8 regularly scheduled meetings per year. At a high level, the Federal Reserve controls 3 aspects of monetary policy - open market operations, reserve requirements, and the discount rate. The FOMC is responsible for open market operations, and consists of 12 members.

Everyone had eyes on the commentary around interest rates. The results? 7 officials see rate hikes by end of 2022 (vs 4 from the March meeting). In general, the tone was “hawkish.” Generally a monetary hawk is someone who advocates for keeping inflation low -> tight monetary policy. One tool the government can use to fight inflation is higher interest rates. The oppose (dovish) advocates for expansionary monetary policy (lower rates, increased money supply).

Right after the meeting we saw a sell off in growth names (mid day Wednesday). However, this didn’t last. On Thursday just about every growth software name was up big (after most opened up the day slightly down). The WCLD index fund was up >3%. Why? In many ways this was the opposite of a “short squeeze.” When the FOMC commentary implied a quicker timeline to rising rates, everyone expected growth names to drop more than they did. When the result wasn’t nearly as negative as expectations, there was more urgency to get back into growth names (or as my colleague put it “a bit of a rush to get back onside). Given the uncertainty around inflation, there has been more money sitting on the sidelines for growth software. However, if tighter monetary policy wasn’t going to affect growth multiples in the same way people imagined, what will? It’s always tough to predict if / when growth software multiples will return to historical levels. For now, they’ve proved somewhat resilient to tighter monetary policy expectations. We’ll see what happens from now until Q2 earnings, and if the market reaction on Thursday influences the next FOMC meeting.

Top 10 EV / NTM Revenue Multiples

We have a new #1!

Top 10 Weekly Share Price Movement

Update on Multiples

SaaS businesses are valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 15.9x

Top 5 Median: 45.7x

3 Month Trailing Average: 14.9x

1 Year Trailing Average: 15.2x

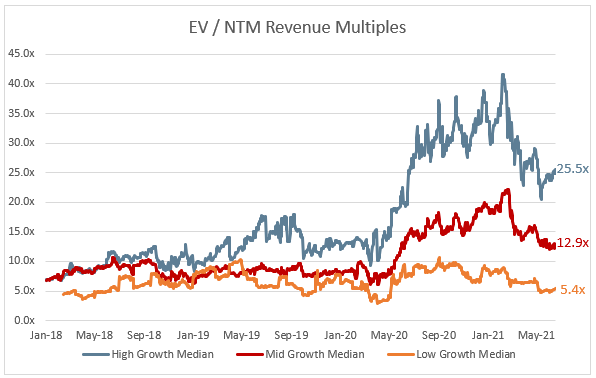

Bucketed by Growth. In the buckets below I consider high growth >30% projected NTM growth, mid growth 15%-30% and low growth <15%

High Growth Median: 25.5x

Mid Growth Median: 12.9x

Low Growth Median: 5.4x

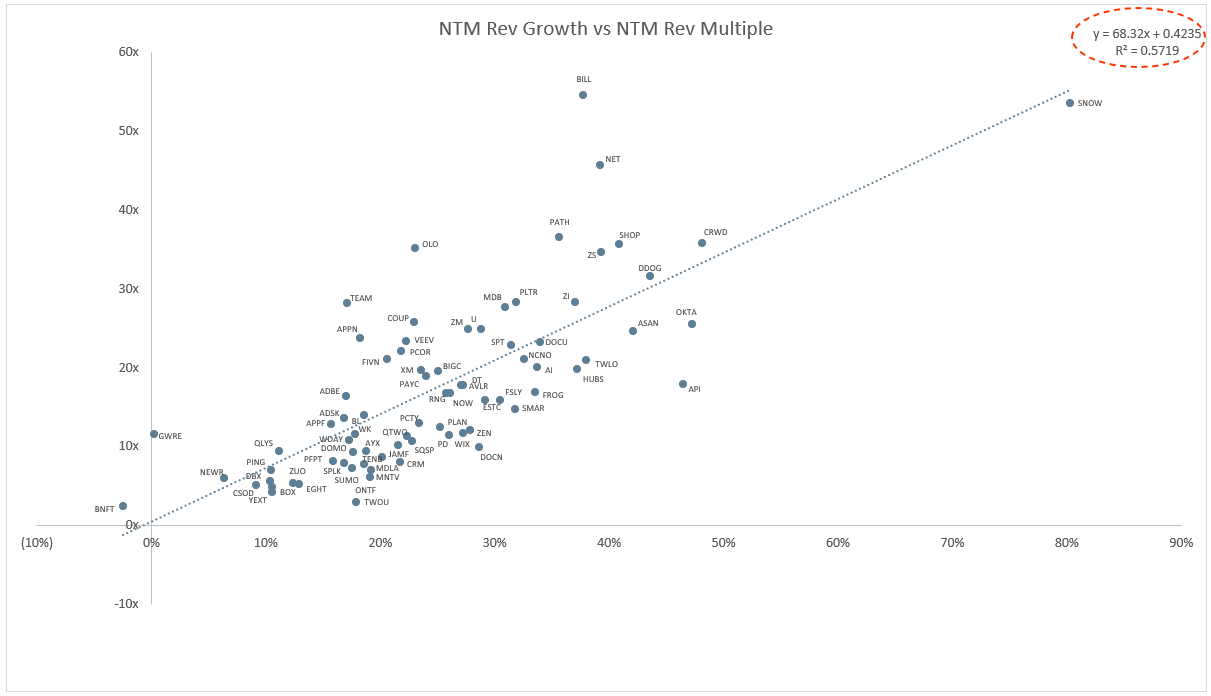

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Growth Adjusted EV / NTM Rev

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. The goal of this graph is to show how relatively cheap / expensive each stock is relative to their growth expectations

Operating Metrics

Median NTM growth rate: 23%

Median LTM growth rate: 30%

Median Gross Margin: 74%

Median Operating Margin (13%)

Median FCF Margin: 10%

Median Net Retention: 118%

Median CAC Payback: 24 months

Median S&M % Revenue: 43%

Median R&D % Revenue: 25%

Median G&A % Revenue: 18%

Comps Output

Rule of 40 shows LTM growth rate + LTM FCF Margin. FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12 . It shows the number of months it takes for a SaaS business to payback their fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.