Clouded Judgement 6.27.25 - New Rules For a New Game

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

New Rules For a New Game

One of the biggest shifts happening in startups right now is that the old rule of thumbs for how you build a successful software startup just don’t hold in the age of AI. Or at least, they don’t hold if you’re trying to build a breakout company…

So many of these markets are still wide open. And they’re HUGE. Nobody owns them yet. The use cases are new, the distribution channels are new, and the product categories are still forming. That means the biggest risk isn’t building the wrong thing, it’s moving too slowly while someone else figures it out faster.

In a greenfield market, the first company to get real usage becomes the category. They set the norms. They get the feedback loops. They get the mindshare. Once that flywheel starts spinning, it’s hard to catch up. And most importantly, this happens so quickly! Look at how fast Cursor developed mindshare and hit escape velocity in the coding space. How could anyone catch them now? It certainly could happen - but if you blinked you’re already way behind them.

This is a big mindset shift for a lot of founders (and investors). I used to believe pretty strongly in not overcapitalizing your business too early. Wait to hit milestones. Raise in steps. Spend in steps. De-risk things one at a time and move sequentially. I saw too many companies implode in 2020–2021 after raising too much too soon and getting out over their skis. They started doing many things in parallel, didn’t focus, didn’t prioritize the right things, and ended up with an upside down P&L.

But the dynamics now are different. Very different! If you move too slowly, you get leapfrogged. You lose because someone else was willing to make the same bets (or riskier bets!), just faster. And importantly - they iterated faster. That’s the real skill… Smart iteration. Even if the ideas or risks were half-baked. And in a greenfield market, speed matters more than polish. I think there’s a saying that goes something like “perfection is the enemy of good.” Said another way, don't let the pursuit of the perfect plan get in the way of fast execution. Whether it’s polishing a blog post, a product release, or anything else…Speed of execution and iteration is now becoming more important. Don’t wait 3 weeks to get the product marketing perfect…Or the blog post perfect. Get the core message right and ship it! Then iterate.

That means doing things in parallel that used to be sequenced. Spinning up GTM before product-market fit is fully obvious. Running multiple product experiments at once. Making strategic hires before the strategy is fully locked. Spending ahead of the next milestone, not after it. The list goes on! It’s harder than ever to actually have a product roadmap… The world changes so quickly it’s almost better to NOT have a long term roadmap because you might become biased towards executing on that specific roadmap when the world shifts…The roadmap should shift, but by defining a roadmap too early it can be harder to change it…

It’s uncomfortable. It’s VERY uncomfortable for me as an investor / board member. But it might be necessary? This doesn’t mean every startup should go out and raise a $50M Series A and burn $2M/month. But it does mean that for the companies swinging big, the bar has changed and the timelines are compressed. The expectations are higher. The old “best practices” might actually slow you down. This also has implications on the people you hire. You don’t want to hire the “old guard” who only knows how to run the “old guard” playbooks. I think there will be TONS of alpha in hiring the rising generation of sales leaders, marketing leaders, engineering leaders, etc who aren’t encumbered by the old way of thinking of things. Companies used to get to a certain scale, and say “lets go hire the VP of sales from [insert successful public company] with a good linkedin resume.” Now you may not want to! Need folks with a fresh take that can help define the NEW playbooks, not come in and run the old ones..

Of course, this isn’t universal advice. If you’re building a steady, profitable SaaS business, none of this may apply. But if you’re trying to build something that defines a category, the playbook needs to look different.

[Editorial note] Re-reading this post I noticed my own writing style was a bit different! It felt more frantic, lots of shorter sentences, etc. Maybe it’s a reflection of my own mindset shift :)

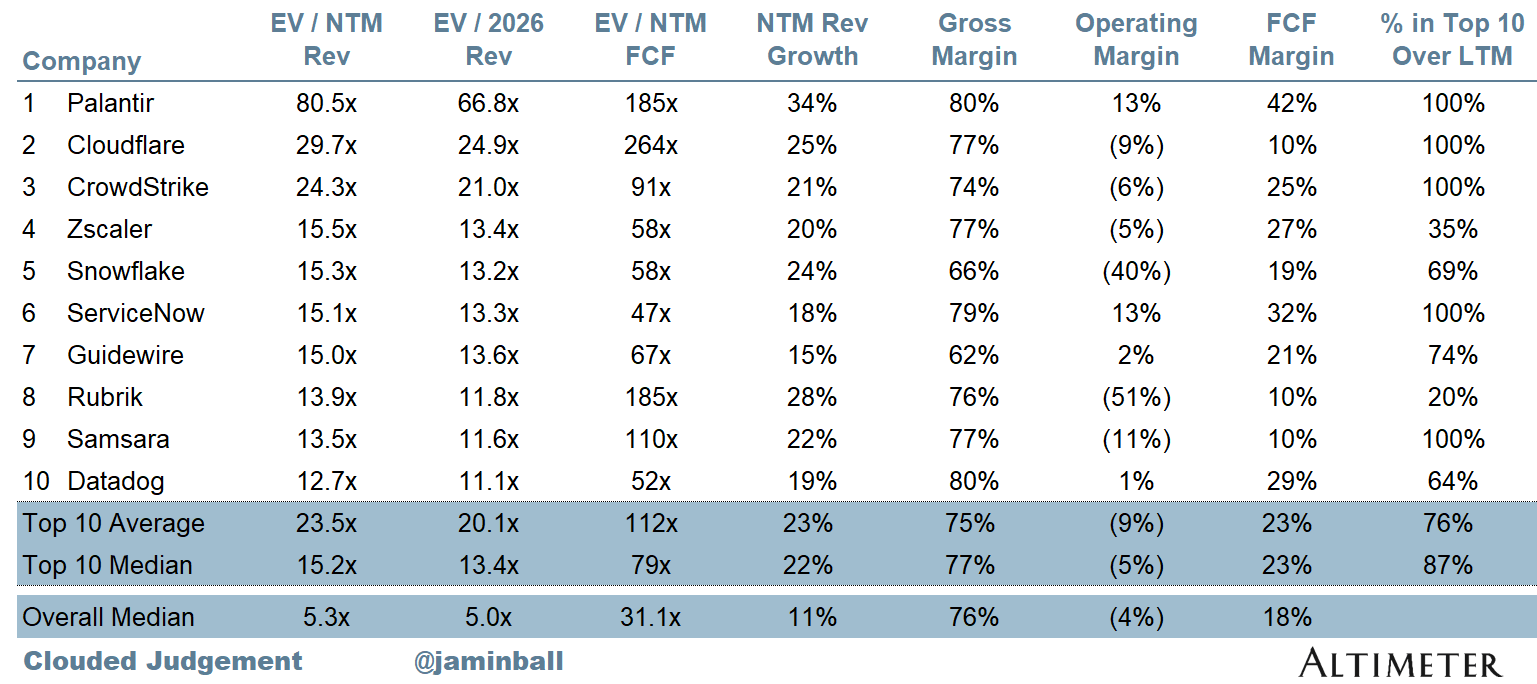

Top 10 EV / NTM Revenue Multiples

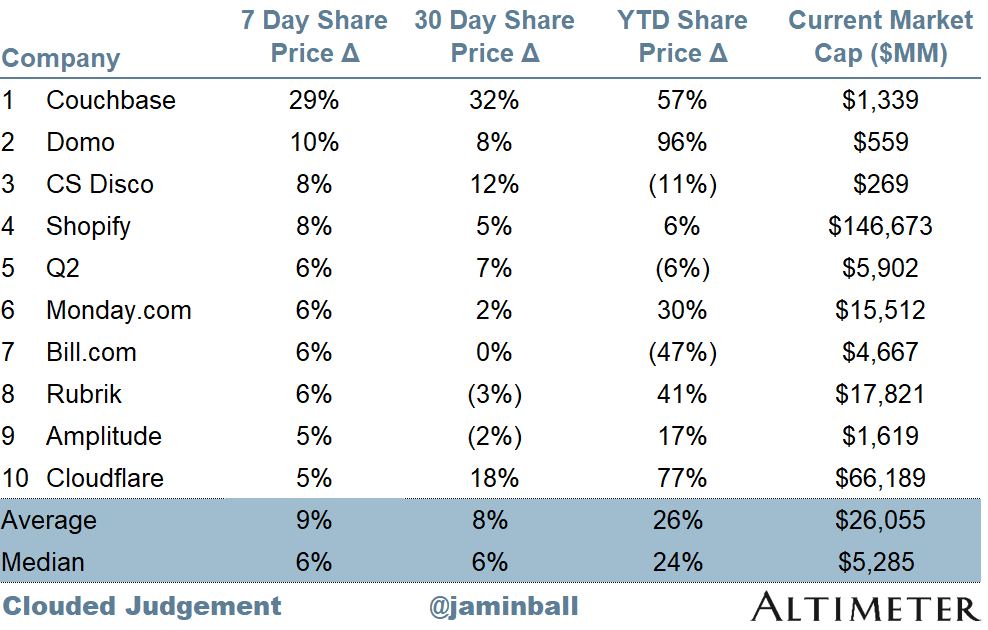

Top 10 Weekly Share Price Movement

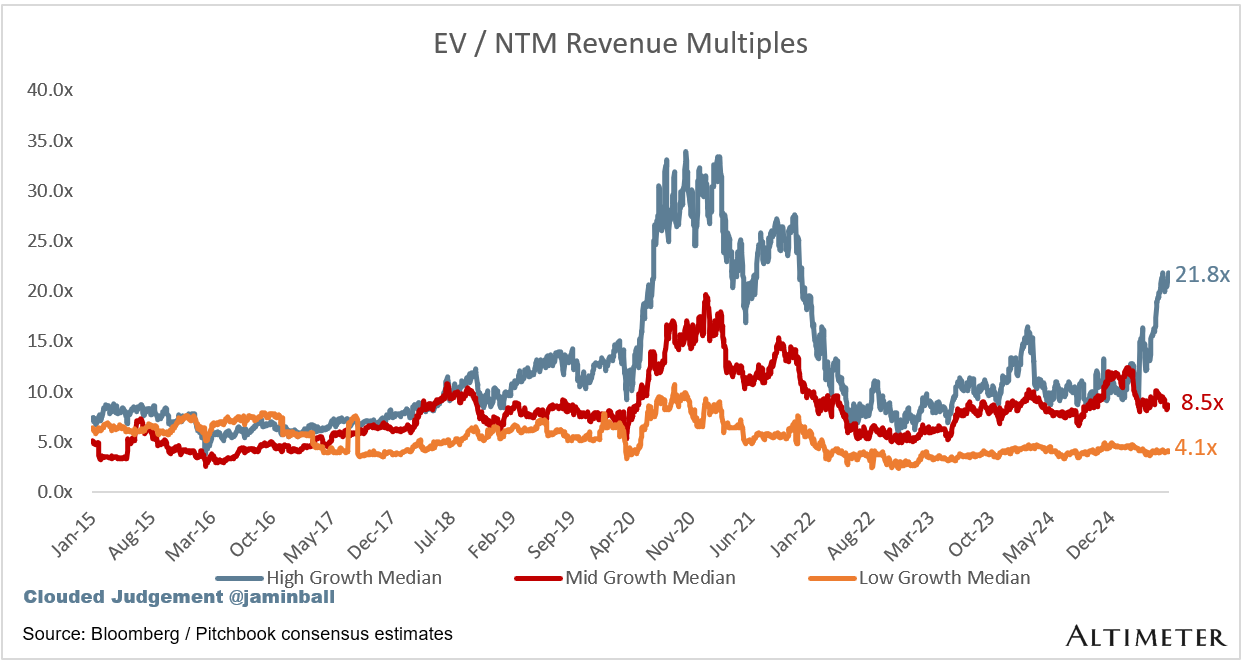

Update on Multiples

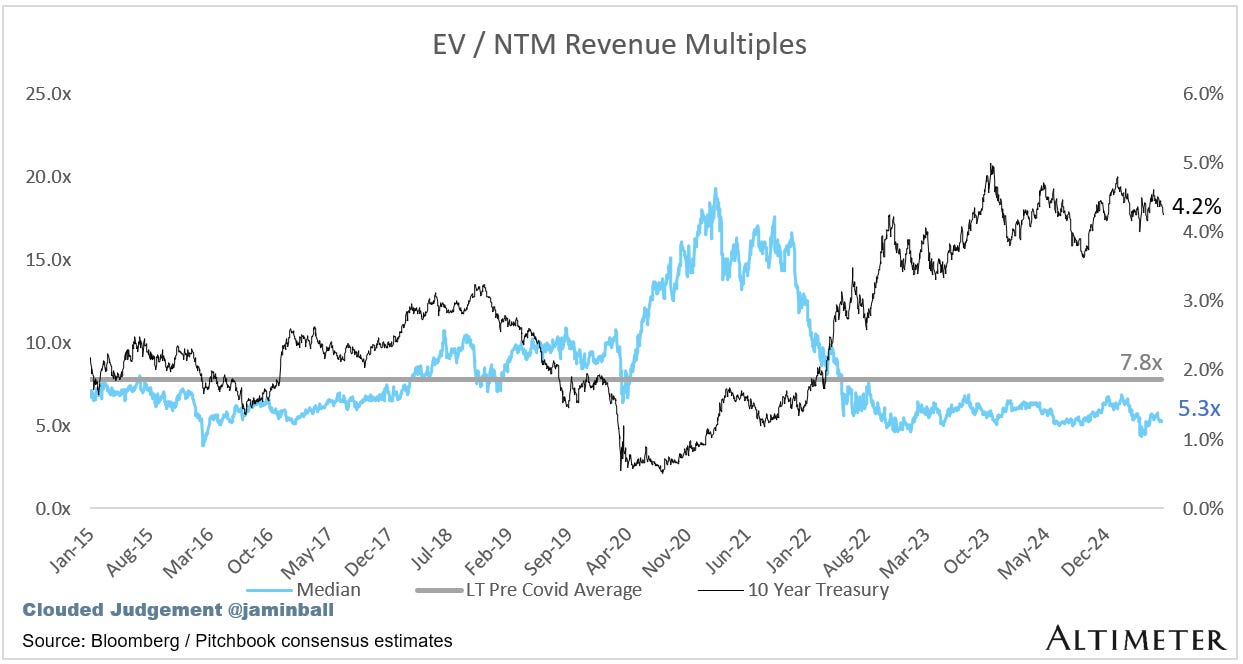

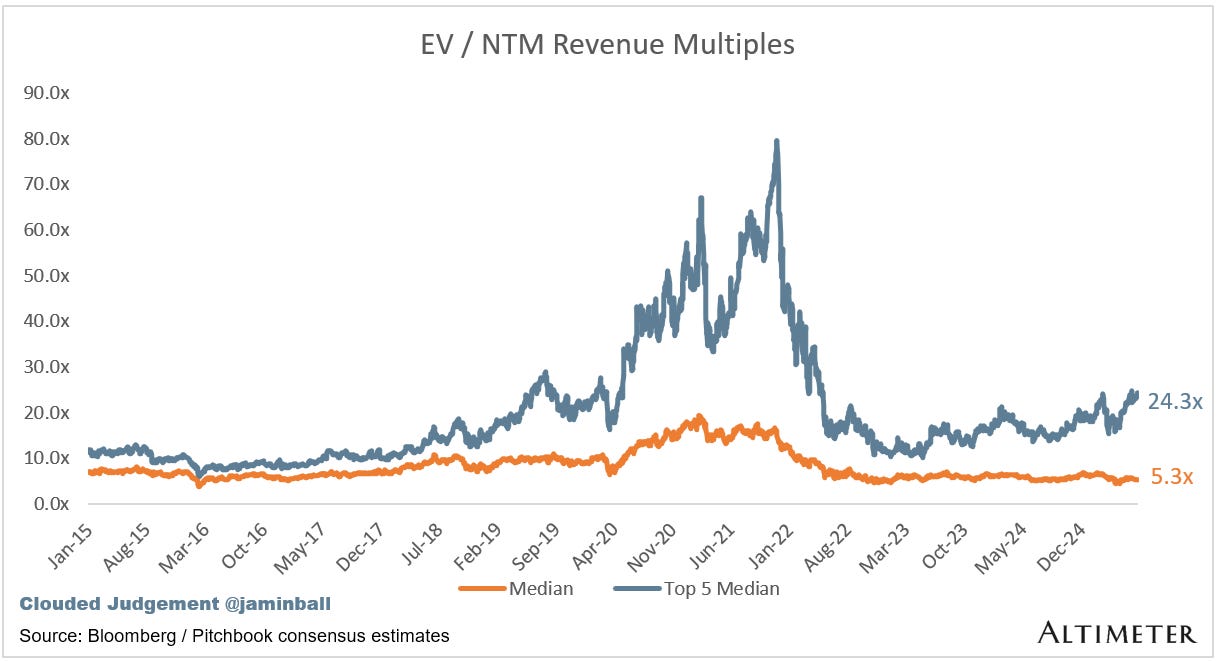

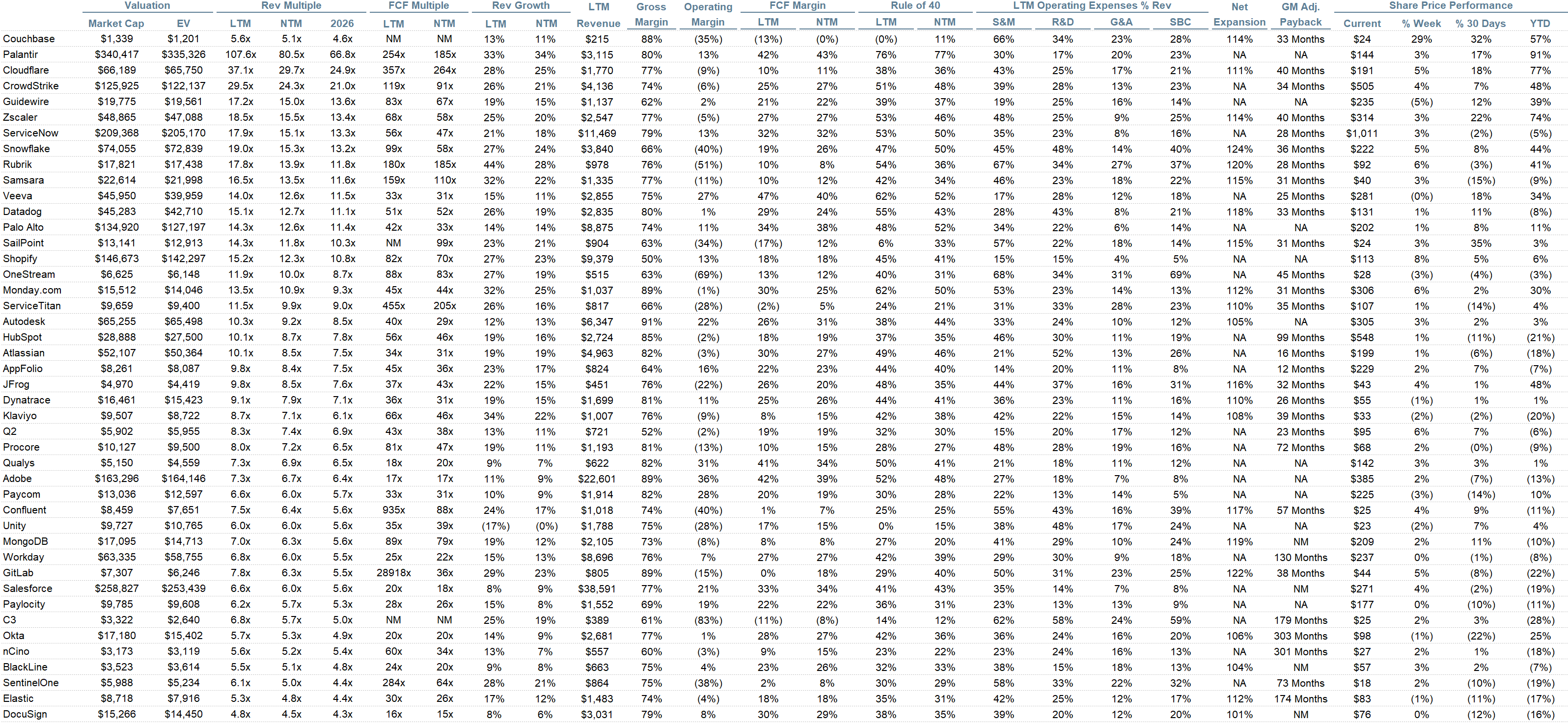

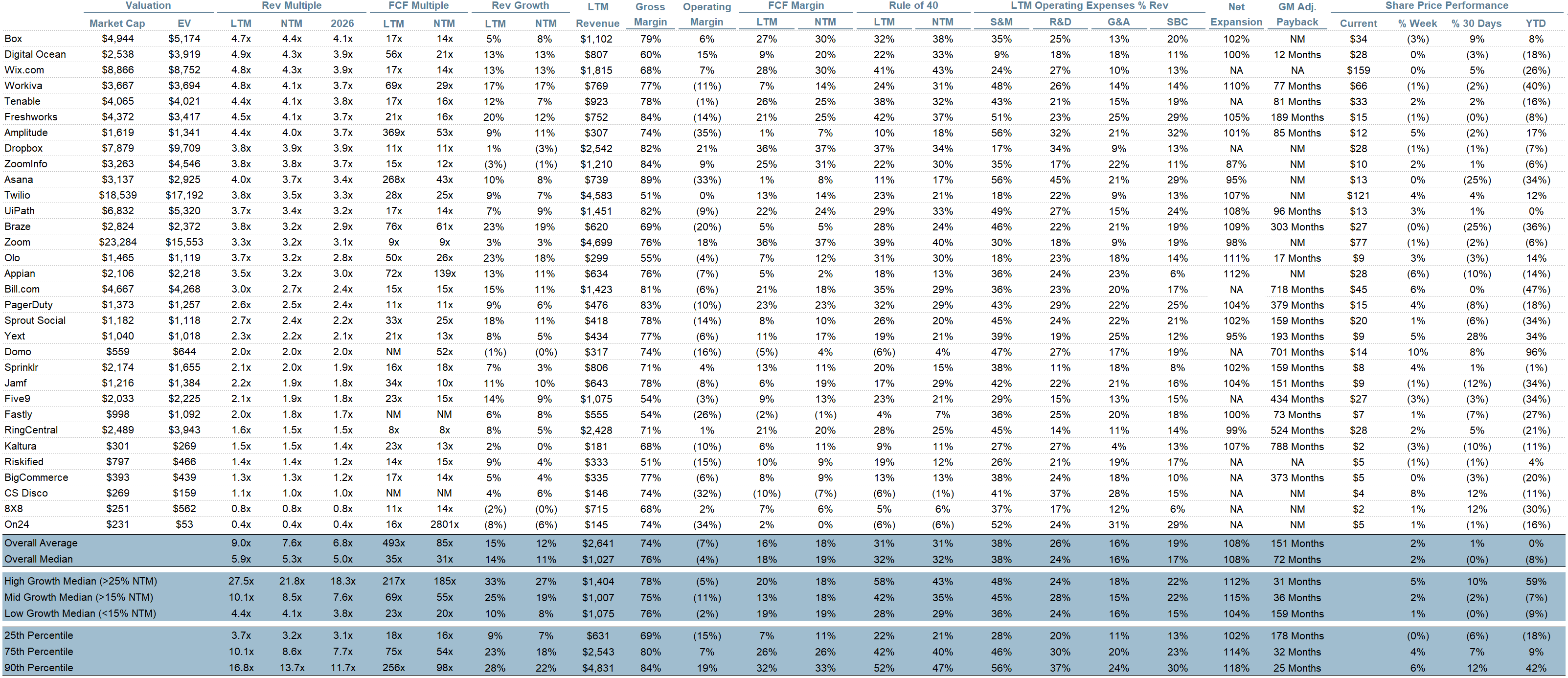

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 5.3x

Top 5 Median: 24.3x

10Y: 4.2%

Bucketed by Growth. In the buckets below I consider high growth >25% projected NTM growth, mid growth 15%-25% and low growth <15%

High Growth Median: 21.8x

Mid Growth Median: 8.5x

Low Growth Median: 4.1x

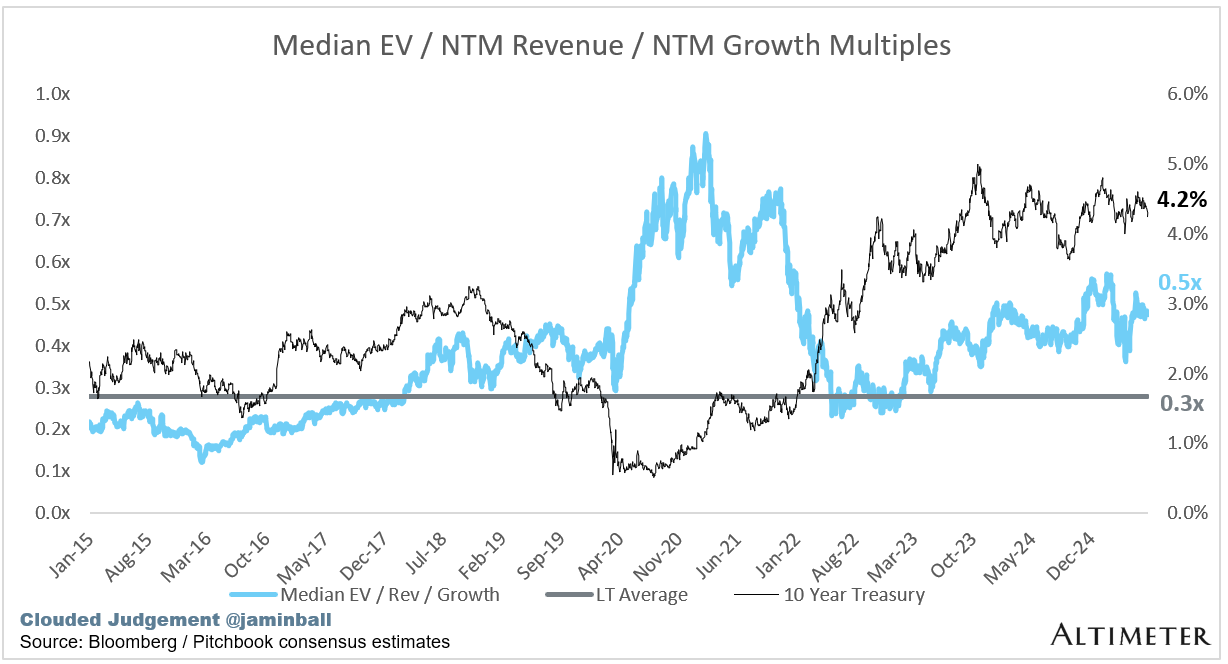

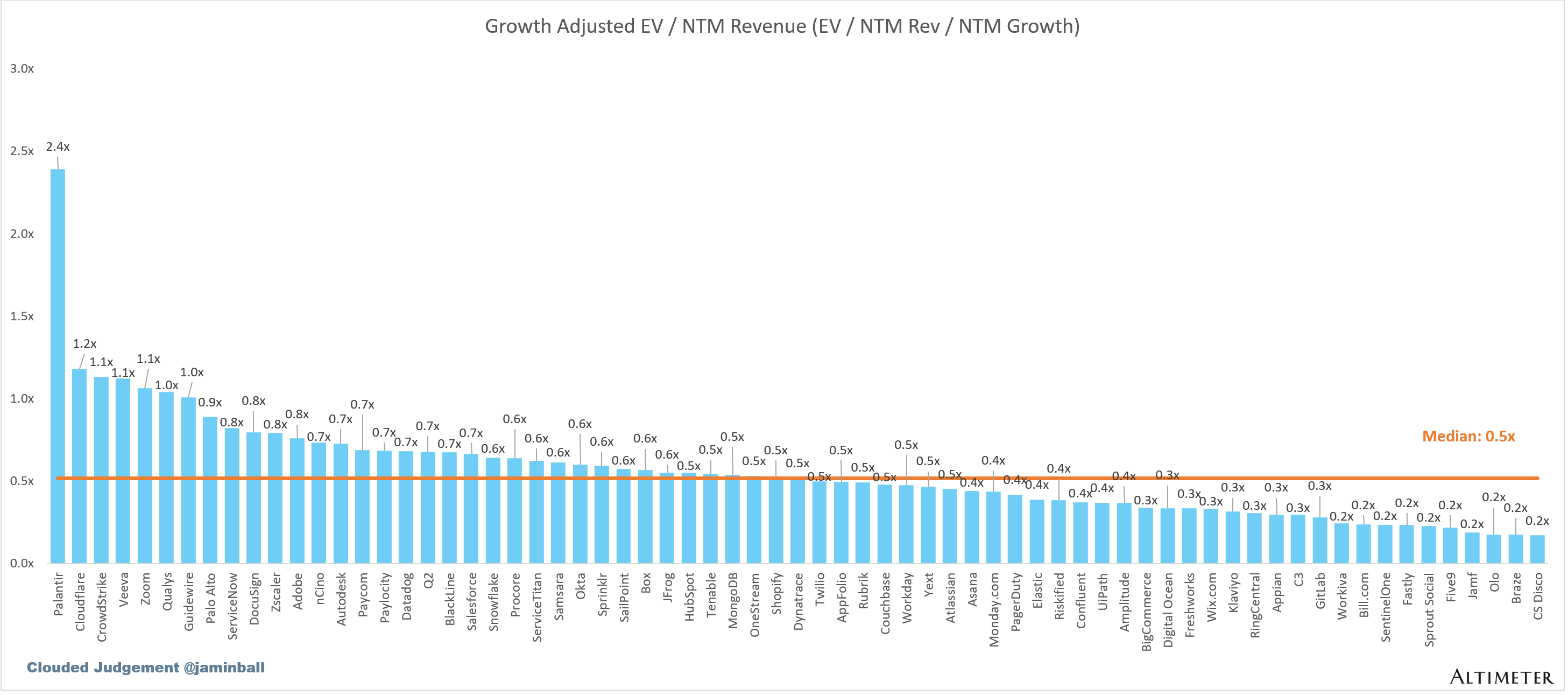

EV / NTM Rev / NTM Growth

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. So a company trading at 20x NTM revenue that is projected to grow 100% would be trading at 0.2x. The goal of this graph is to show how relatively cheap / expensive each stock is relative to its growth expectations.

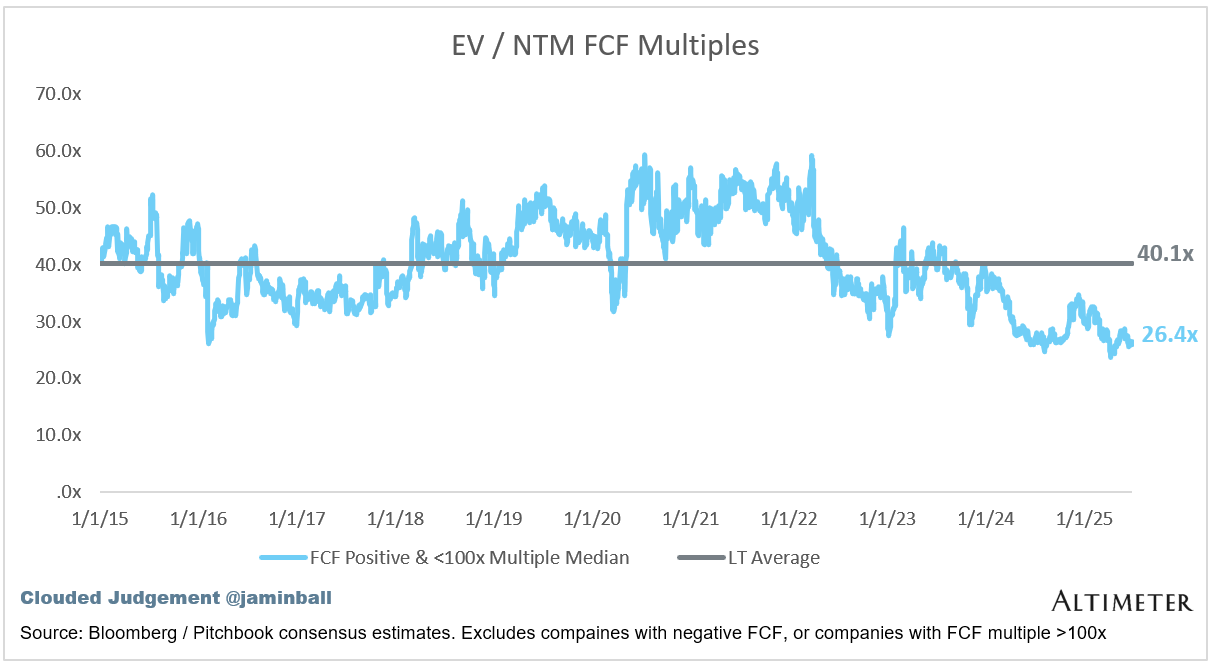

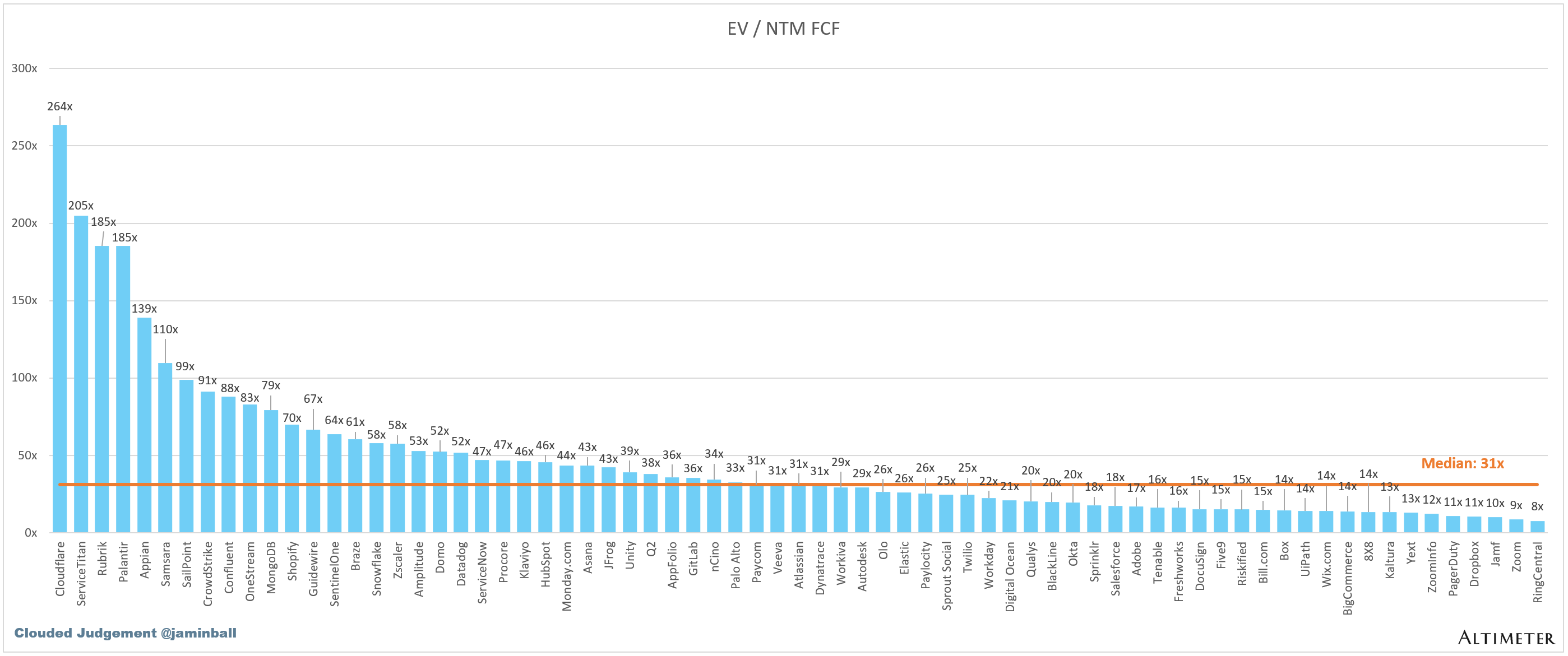

EV / NTM FCF

The line chart shows the median of all companies with a FCF multiple >0x and <100x. I created this subset to show companies where FCF is a relevant valuation metric.

Companies with negative NTM FCF are not listed on the chart

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Operating Metrics

Median NTM growth rate: 11%

Median LTM growth rate: 14%

Median Gross Margin: 76%

Median Operating Margin (4%)

Median FCF Margin: 18%

Median Net Retention: 108%

Median CAC Payback: 72 months

Median S&M % Revenue: 38%

Median R&D % Revenue: 24%

Median G&A % Revenue: 16%

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12. It shows the number of months it takes for a SaaS business to pay back its fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Sources used in this post include Bloomberg, Pitchbook and company filings

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.