Clouded Judgement 8.25.23 - The Ground Truth of the 10Y and Interest Rates

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

The 10Y and Software Valuations

Much has been written about the 10Y, and interest rates more broadly, and their impact on software valuations. However, there’s a lot to unpack there. Interest rates aren’t simply 1 “thing.” They’re a basket of instruments with different maturities / durations set by different forces. They’re all related, but also independent, from one another. At the most base level interest rates are the ground truth of software valuations. As rates rise, valuations fall (mathematically). This is because ground truth for a company’s valuation is the present value of future cash flows. For software companies, a very high weighting of those cash flows come from outer years (as opposed to generating them now). So when rates rise, we discount a higher percentage of those future cash flows more heavily given higher rates. Time value of money dictates that $1 in the future is worth less with higher rates as the discount rate rises.

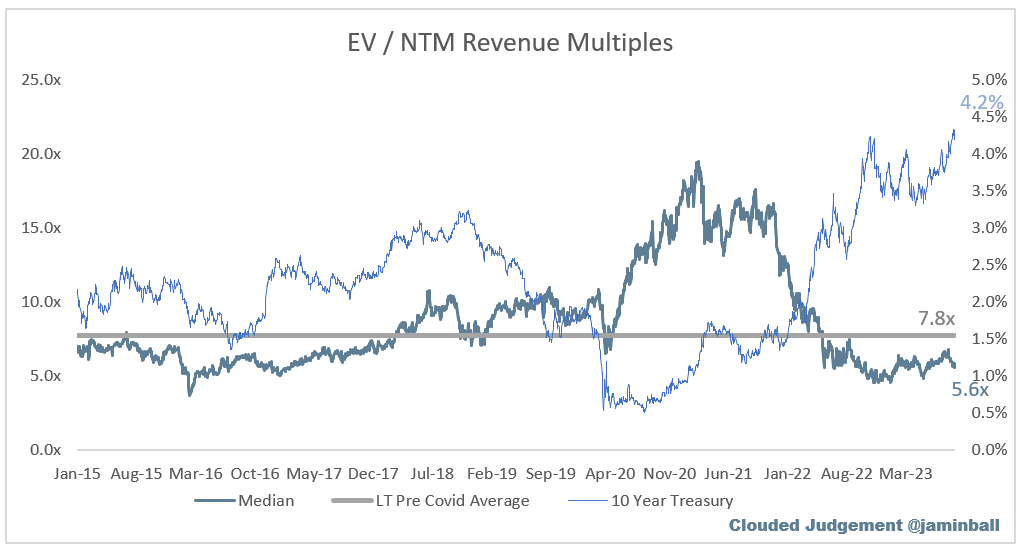

However, when we look at the correlation between interest rates and software valuations over a long period of time they’re actually not that correlated. The R^2 of the median software multiple and 10Y rate going back to 2015 is 0.35. That’s a pretty low correlation over a long period of time. Instead, moves in valuations and rates tend to be HIGHLY correlated in small bursts (generally when there’s a directional or velocity change in 10Y movement). If we look at the last month, the R^2 of rates and multiples jumps to >0.7. Why is this? Fundamentally the rationale for the move in the 10Y (and what’s going on around the economy then) matters A LOT more than simply the absolute change in the 10Y.

Let’s unpack that. From the beginning of May to the end of July software stocks took off. It was the summer of love! On 5/2 the median software multiple was 5.0x and the 10Y was 3.4%. On 7/31 the median software multiple was 6.8x and the 10Y was 4.0%. Said another way, in a 3 month window rates ROSE almost 20% while multiples EXPANDED 36%! So as rates rose, valuations…rose?! Huh?!

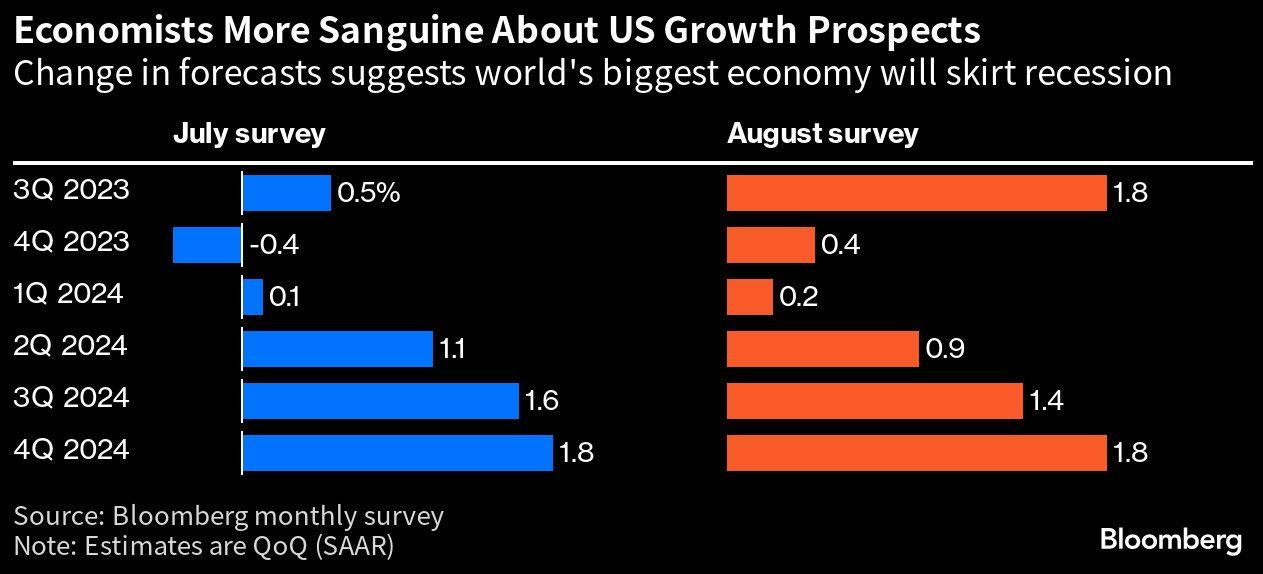

This gets back to my point earlier - the rationale for the change in rates matters a lot more then the absolute change. So what happened in May / June / July? The consensus narrative became the economy was going to avoid a recession, and the goldilocks soft landing would play out. Look at the chart below. We’ve seen quite positive changes in sentiment around the economy (GDP growth). Important to keep in mind these survey’s are lagging indicators.

Rates then rose as the assumption was a robust economy could withstand higher rates, and the Fed would go down this path to permanently squash inflation. The larger point though - the tailwind of business re-acceleration from a soft landing outweighed the valuation headwind from higher rates. So equities rose despite higher rates. Said another way - the reason rates were rising was actually a positive!

Contrast that with what happened over the last month as the 10Y rose from 3.75% to 4.3%. The median multiple fell from 6.8x to 5.7x. So what changed? Well, the rational for the interest rate rise was different this time. There was now a perceived structural change in rates. I won’t go into all of the detail here, but the TLDR is that as the government bank account (the TGA) has shrunk, government debt has also ballooned - the implication is that the government will have to raise money in order to pay off the interest expense on their debt (as well as fund other obligations). They don’t have that cash in their bank account, so the way the government raises money is by selling treasuries to banks (banks give the government money in return for treasuries with a yield). The government then uses this cash to pay off interest expenses (which is becoming a growing portion of their overall spend). What happens here is that as banks buy treasuries, they give up their cash reserves (which they would have otherwise used to lend out to other banks or consumers for things like mortgages). This happens across the board at all banks. As their supply of reserves goes down, classic supply / demand economy 101 effects kick in and rates go up. When something becomes scarce, and the demand stays steady, the price goes up. Capital for loans are becoming more scarce, so the price (ie the rate / cost to borrow) goes up. This is a structural reason that people believe rates will rise. And what’s fascinating here is this structural reason can become detached from the Fed Funds rate. The Fed could cut the fed funds rate and we could see the 10Y rise for exactly this reason. The Fed Funds rate is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. However, the government will still need to sell treasuries to fund operations (of which interest expense on ballooning debt is becoming a greater portion). This is happening no matter what happens to the Fed Funds rate. At the risk of beating a dead horse (but it’s worth emphasizing), we could see the Fed CUT the fed funds rate, but the 10Y continue to rise for the structural reasons described above. If this wasn’t enough - there is now also increasing talk of a recession coming back on the table. China economy is imploding, real economy showing signs of cracking (look at some retailers who’ve recently reported earnings like Macy’s, Ducks Sporting Goods and Foot Locker, or T Mobile announcing yesterday a large layoff), student debt payments restarting soon, housing at it’s most unaffordable levels in decades, etc. The worst case here is that we have a hard landing as the lag effect of rate hikes kicks in. This would cause the Fed to cut the Fed Funds rate, but what if the 10Y stays high (and goes higher) for the structural reasons I mentioned above. Not good. For what it’s worth, this isn’t my base case - I’m more optimistic on the future, but wanted to lay out this case as a possibility.

I’ve thrown a lot at you, but in summary:

The rationale for rates going up in May / June / July was positive - the economy was looking good. So software valuations rose

The rationale for rates going up over the last month has been negative - structural forces are pushing 10Y higher despite incremental data on the economy worsening. So software valuations have fallen

If you’d like to read more of a deep dive on the structural implications or rates rising (this all comes back to liquidity), I wrote a long form piece in June on exactly this topic. You can read the full article here

To hit this point home - I’ve talked today about how rates rising can have opposite effects on software valuations given the rationale for the move. The same can be true for rates falling. Rates can fall for two reasons:

Economy strong and inflation coming down. This implies we don’t need to keep rates so restrictive (as inflation falls and rates stay constant real rates actually go up and become even more restrictive), so the Fed would lower rates. And with a strong economy, lower rates would push valuations up (as business fundamentals would remain strong as well)

Economy weak and heading into a recession. Rate would get cut to stimulate the economy and help us get out of a recession, however unfortunately the headwind of a recession and deteriorating fundamentals would be greater than tailwind of lower rates and stocks would fall (even as rates fall).

This will be important to keep in mind in the future IF rates fall. What’s the reason for the move vs the absolute move?

Maybe next week I’ll put a post together on how real rates correlate with software valuations. Real rates are just the 10Y rate - 10Y inflation expectations (simplification).

Snowflake / Consumption Trends

This weeks post has been way more macro heavy than usual. Now on to some software content…Snowflake was one of the first companies to report a Q2 who’s quarter ended in July. So we got a glimpse of 1 incremental month of data. Overall, I’d say it was a big net positive. Their tone suggests we’re really turning a corner. In Frank’s opening remarks he said: “In Q2, we continue to execute in an unsettled macro environment but with incremental improvement in general sentiment and engagement.” Later Scarpelli said: “In May, we saw a return to growth with strength continuing into June and July. From a booking standpoint, we saw promising signs of stabilization with new bookings outperforming our expectations.”

In July specifically, it sounds like customers across the board started to proactively engage more around new deals / contracts. Scarpelli said: “the contracting actually feels the sentiment really seemed to change in July with customers really reengaging with us. And so -- and I think we'll have good bookings, but that doesn't equate to consumption. It takes time for the consumption to come in.” It’s important to highlight the part at the end - it takes time to go from contract to usage / consumption (and thus recognized revenue).

They did say their largest customers continue to be a growth headwind with more scrutiny around costs. So we’re definitely not out of the woods yet around optimization headwinds, we’re getting to a better place.

Overall I’d say Snowflake’s was an incremental data point that macro headwinds are definitely not getting worse, and may in fact be starting to show signs of easing up

Quarterly Reports Summary

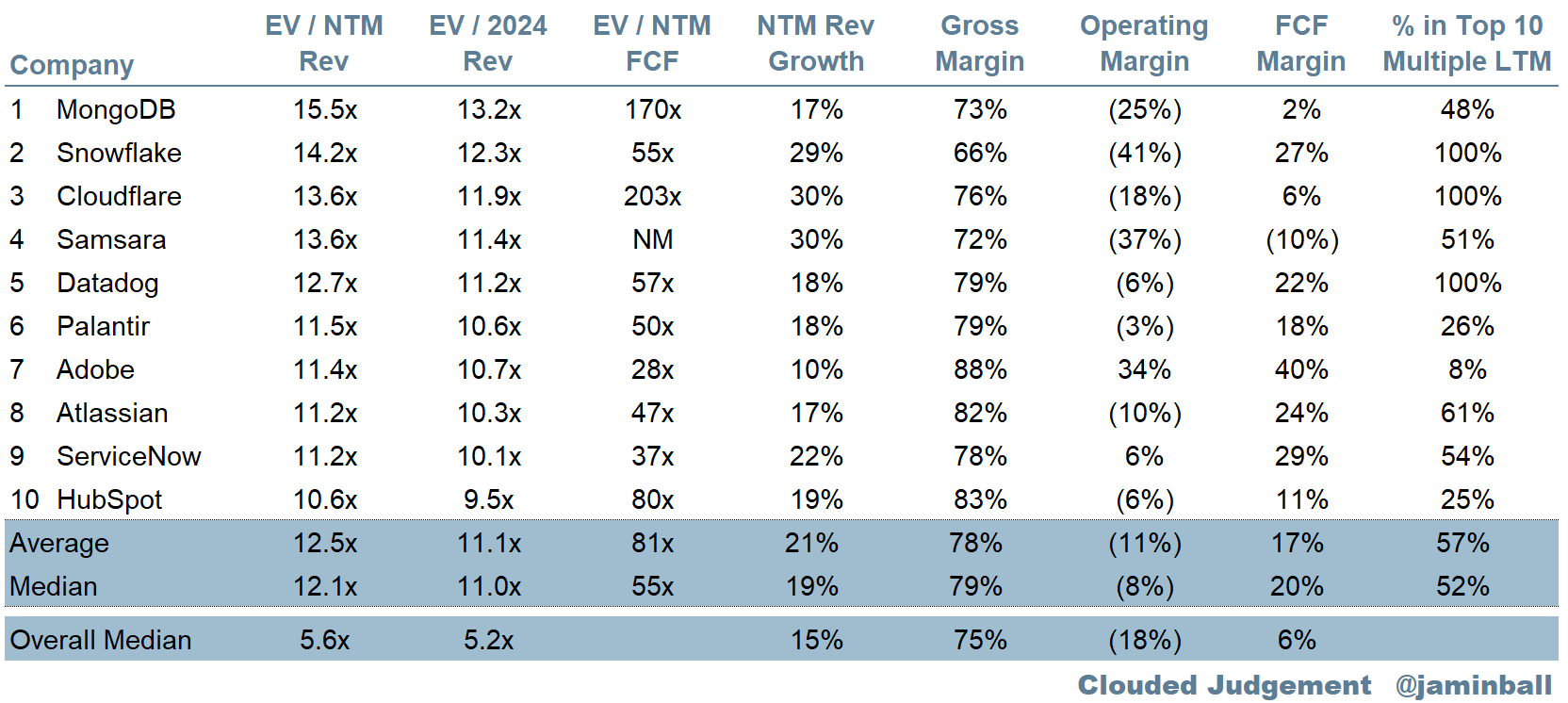

Top 10 EV / NTM Revenue Multiples

Top 10 Weekly Share Price Movement

Update on Multiples

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 5.6x

Top 5 Median: 13.6x

10Y: 4.2%

Bucketed by Growth. In the buckets below I consider high growth >30% projected NTM growth, mid growth 15%-30% and low growth <15%

High Growth Median: 10.0x

Mid Growth Median: 8.1x

Low Growth Median: 3.7x

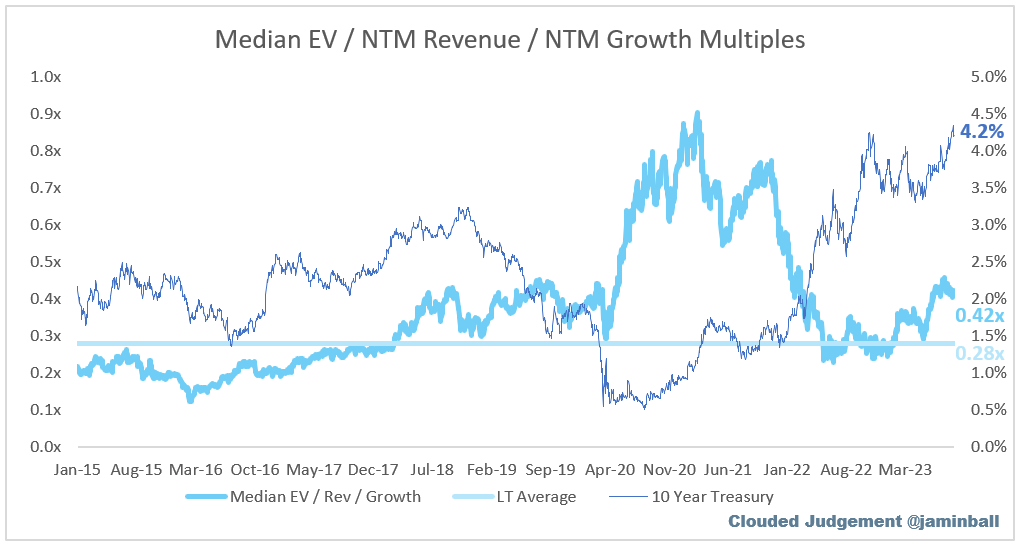

EV / NTM Rev / NTM Growth

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. So a company trading at 20x NTM revenue that is projected to grow 100% would be trading at 0.2x. The goal of this graph is to show how relatively cheap / expensive each stock is relative to their growth expectations

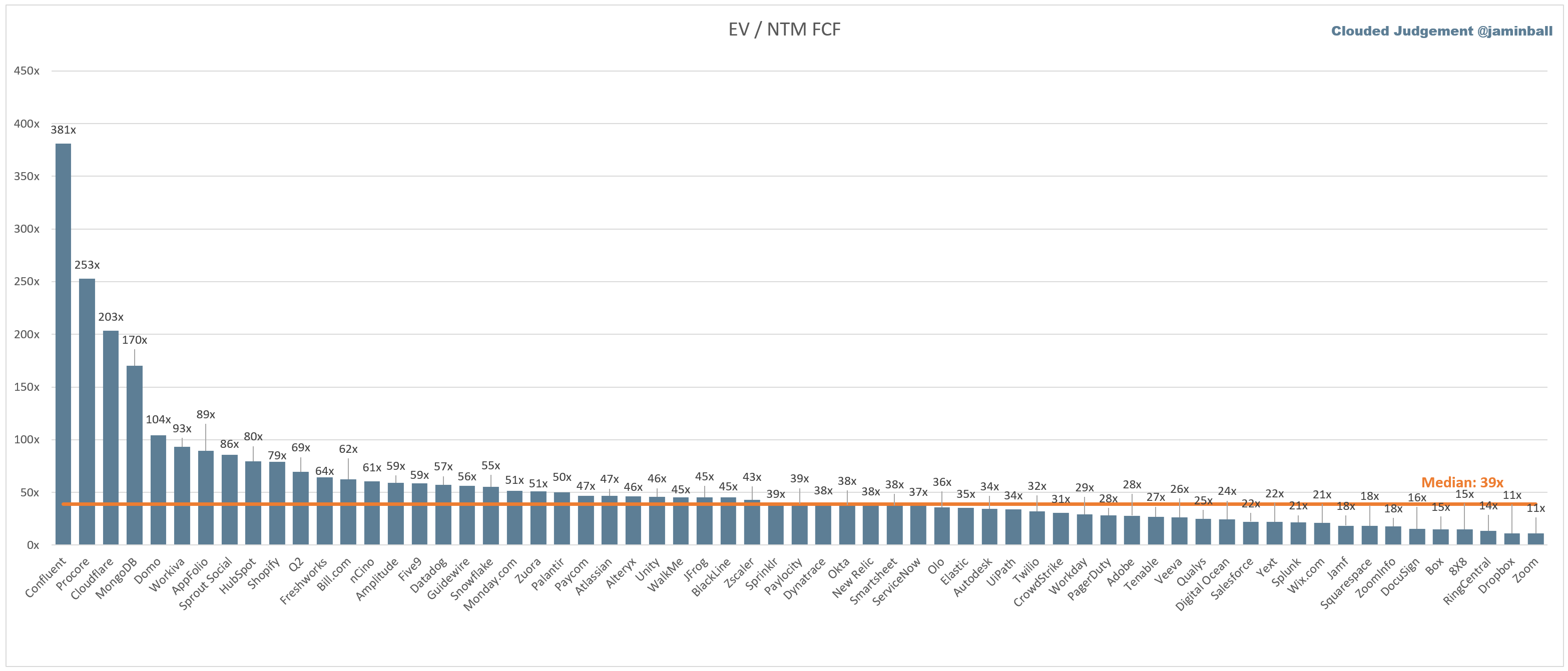

EV / NTM FCF

Companies with negative NTM FCF are not listed on the chart

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Operating Metrics

Median NTM growth rate: 15%

Median LTM growth rate: 23%

Median Gross Margin: 75%

Median Operating Margin (18%)

Median FCF Margin: 6%

Median Net Retention: 115%

Median CAC Payback: 44 months

Median S&M % Revenue: 44%

Median R&D % Revenue: 27%

Median G&A % Revenue: 17%

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12 . It shows the number of months it takes for a SaaS business to payback their fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Excellent content, thank you!

Especially good one today