Clouded Judgement 9.26.25 - Easy Come, Easy Go?

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Easy Come, Easy Go?

I’ve found myself having a similar conversation with a number of investors and founders recently, and wanted to flesh it out a bit into a post. It’s a similar topic to the ERR vs ARR debate. I’m calling this one the “Easy come, Easy go?” debate…

Let’s first start out with an undeniable truth - the fastest growing AI companies are defying the laws of gravity when it comes to scaling. The growth some of these companies are seeing is eye watering. 0-$100m in ARR in less than 12 months! Sometimes faster! There are many reasons this type of growth is possible, but I think it boils down to the fact that many markets in AI are truly greenfield, can demonstrate ROI incredibly quickly, and these together lead to crazy adoption cycles and growth.

Yet despite this, I’ve found myself less “sure” of the durability of these revenues. I’m less “confident” than I probably should be given the trajectory in growth. So why is that? Even when it’s companies that I work with directly, I still find myself having anxiety about what the future will hold (relative to say a company 5 years ago that if they had the same growth trajectory I’d be feeling CERTAIN about the future). This is a question that comes up frequently with investors and founders…

So let’s unpack it. Why should I (or others investors or founders) be feeling anxious despite seeing insane growth? Crazy growth is great. BUT there’s also some “downsides” if not appropriately addressed by founders / companies.

Going 0-$100m (or something like that) in a matter of months probably means:

Your implementation time was very short

Your sales cycle was very short

Your champion made a very fast decision

None of these necessarily seem bad in a vacuum, but they could be canaries in the coal mine. Here are some potential “negatives” with those three bullets listed above

Negatives surrounding short implementation cycles:

Switching costs may be low. This benefited you on the initial sale, but also could cost you if your customer wants to switch to another vendor

It was “too easy” to get up and running

Your product depth may lag adoption

Negatives surrounding short sales cycles:

Buyer enthusiasm may be hype driven

Budgets may be experimental, or procurement could have overbought without realizing it

You were the only vendor evaluated

Negatives surrounding your champion making a very fast decision:

You’re champion may be a junior / mid level person without much political sway

You’re champion isn’t as fully bought in. Maybe they made an emotional decision vs one grounded in research / conviction

If I had to sum all of this up into a couple sentences it would be this: Revenue that is acquired at light speed probably isn’t as sticky. It’s probably not as engrained into the customers workflow or processes (because any software will take time for this to be the case). In other words, revenue acquired quickly can also be lost quickly.

Let’s compare this to a more classic enterprise sale. One that takes 6-9 months. In this type of sales cycle there was probably an in depth RFP conducted where many vendors were compared against one another. Multiple levels of the organization were involved in the decision and are “bought in.” Implementation took a while because it had to be more engrained into other systems and workflows. The entire process took a lot of time and energy, so those responsible have a vested interest to “make it work".” All of these are features, not bugs, of an enterprise sales process. It’s a grind, and it’s hard, but if you make it through the gauntlet of an enterprise sales process you probably come out of it with a level of stickiness.

This is not to say these AI hypergrowth revenue streams are bad…far from it. many will build extremely durable businesses. BUT - I think it’s HYPER important for founders and sales teams of these AI hypergrowth companies to not take their revenue for granted… many of them are PLG-ing their way to massive scale. Companies sign up, expand usage rapidly, and all of a sudden are spending 7+ figures. This will grab the attention of your customer.. What started as a smaller deal will now have the CFOs attention. That CFO will start asking questions. How will this spend trend? Are we getting a volume discount? Who else did we look at to put pricing pressure on the vendor? Could we build this ourselves? Can we trust this startup? etc. And here’s what’s important. If you don’t have a direct, regular, and strong relationship with that company or champion, that 7 figure deal will be at significant risk. You can’t take it for granted. Account management is super important. You need to be proactive about reaching out, making these customers feel special, proactively offering volume discounts, spending time in person, etc.

In some ways, AI companies and founders have it “too easy” and are overlooking the important parts of classic enterprise sales (I say that facetiously, obviously nothing is easy…). Or, they never had to learn the lessons of classic enterprise sales because their business was always up and to the right!

This post was a little bit of a brain dump…If there was one takeaway for founders it’s this - don’t take your revenue for granted, what’s easy to come by could be easy to loose.

Is Triple, Triple, Double, Double Dead?

There was a lot of chatter over X this week on “is triple, triple, double, double dead? It clearly struck a nerve! I don’t have a lot to add, but I will say this. Venture is a game of outliers. Funds are made and hit the top 10% for their vintage if they’re in those outliers. And the reality is, the profile and trajectory of what it means to be an outlier has definitely changed. The goalposts have moved now that companies are scaling MUCH faster than triple, triple, double, double. VCs need outliers. So yes, every VC is searching and hunting for MORE than triple, triple, double, double because it has been demonstrated to exist.

This doesn’t mean triple, triple, double, double is bad. It’s still exceptional. You can build an exceptional business, make tons of money for yourself and your employees by having the triple triple double double trajectory early on. BUT - at the same time, it’s also not what’s most exciting to VCs now that there is a cohort of companies performing much better.

Of course, there are caveats. Many of which I listed above. The insane trajectory may not be as durable. We (VCs) all may be chasing a new growth trajectory that proves to be the wrong one! However, VCs are chasing the outliers, and triple triple double double is no longer an outlier. That’s just the reality. I do think Hemanta comments were taken out of context. I’d imagine he’d agree. Triple triple double double is still very good! And you should be proud as a founder to achieve this. But again (and now I’m just repeating myself…), it’s just not what VCs are hoping to get when there is something better out there.

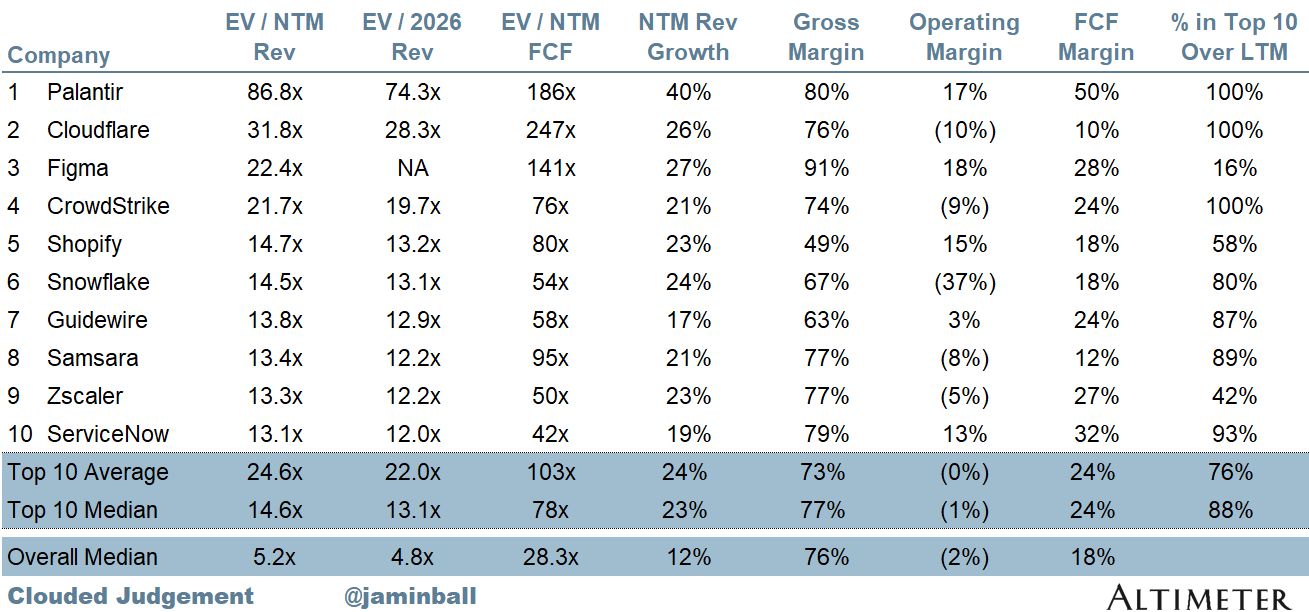

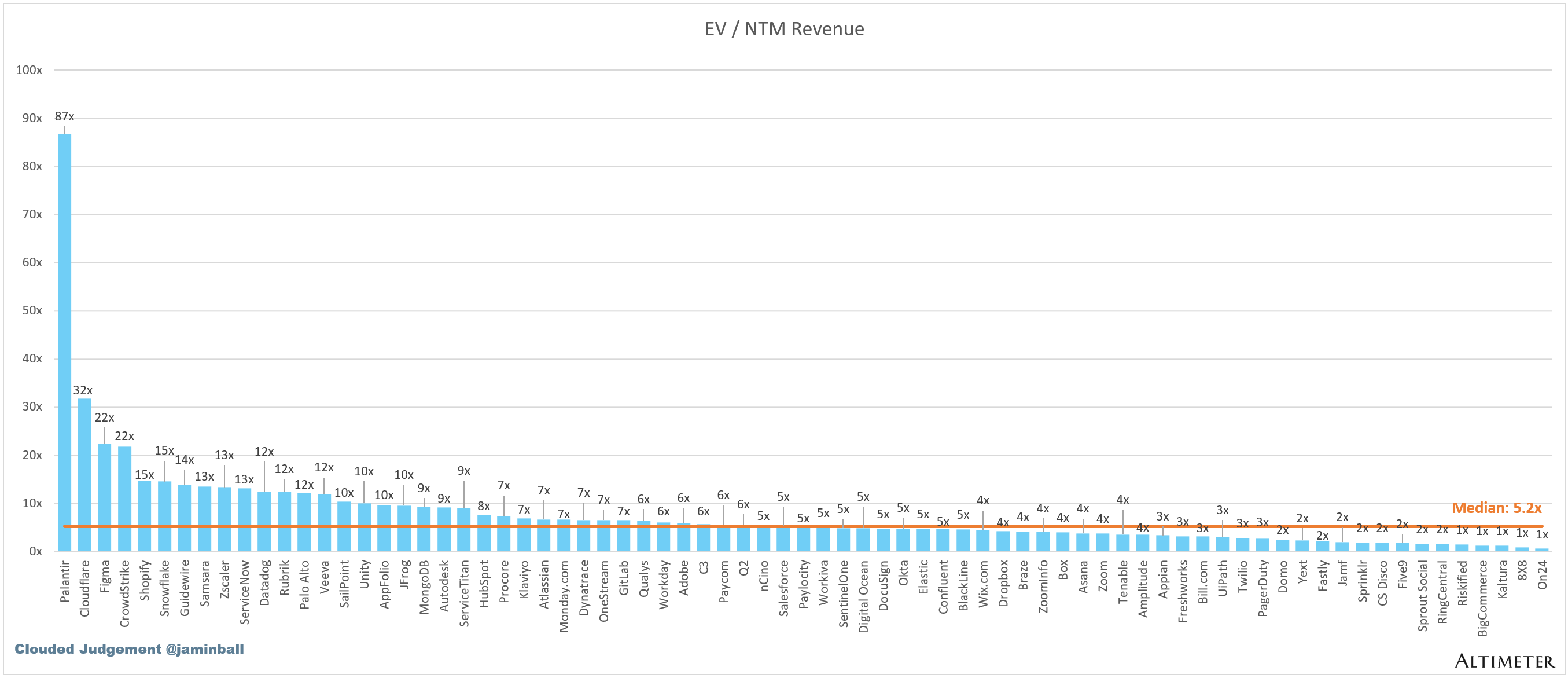

Top 10 EV / NTM Revenue Multiples

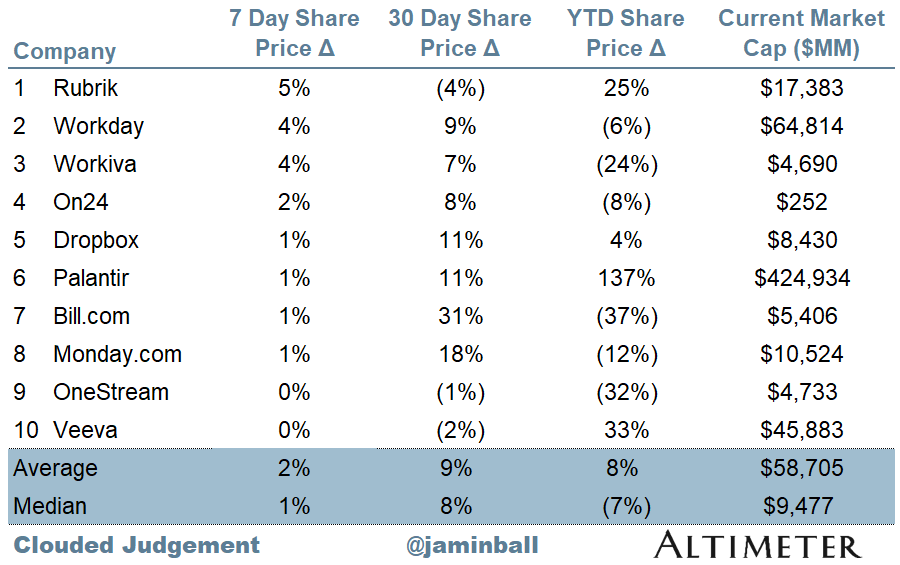

Top 10 Weekly Share Price Movement

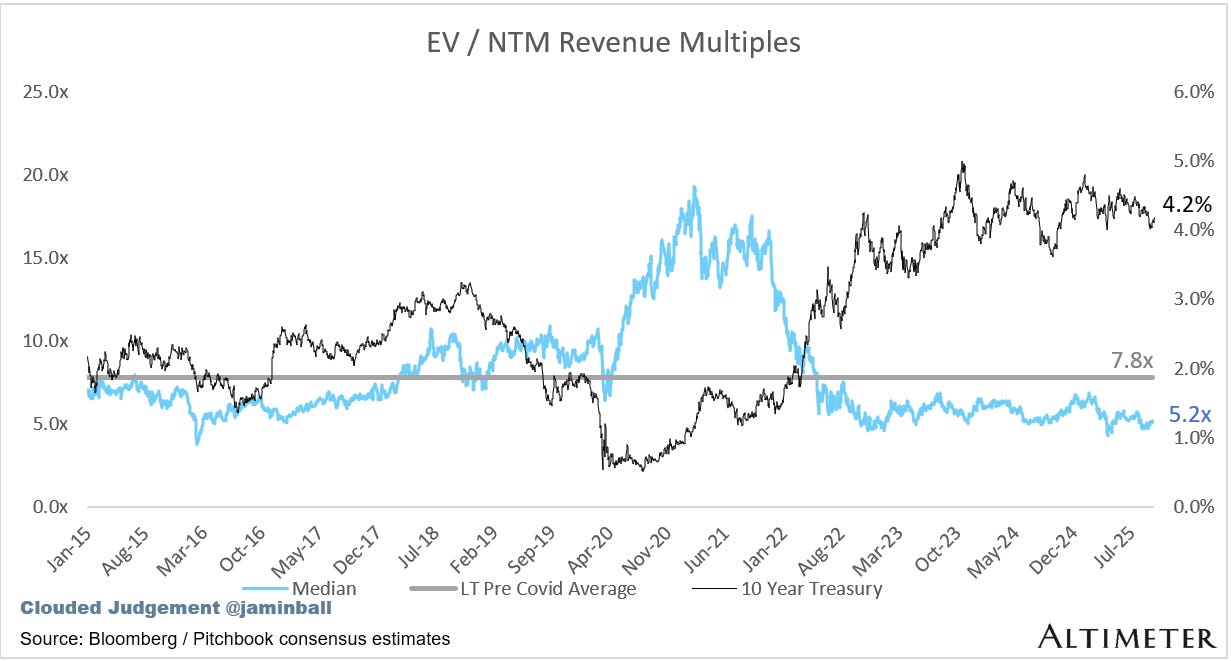

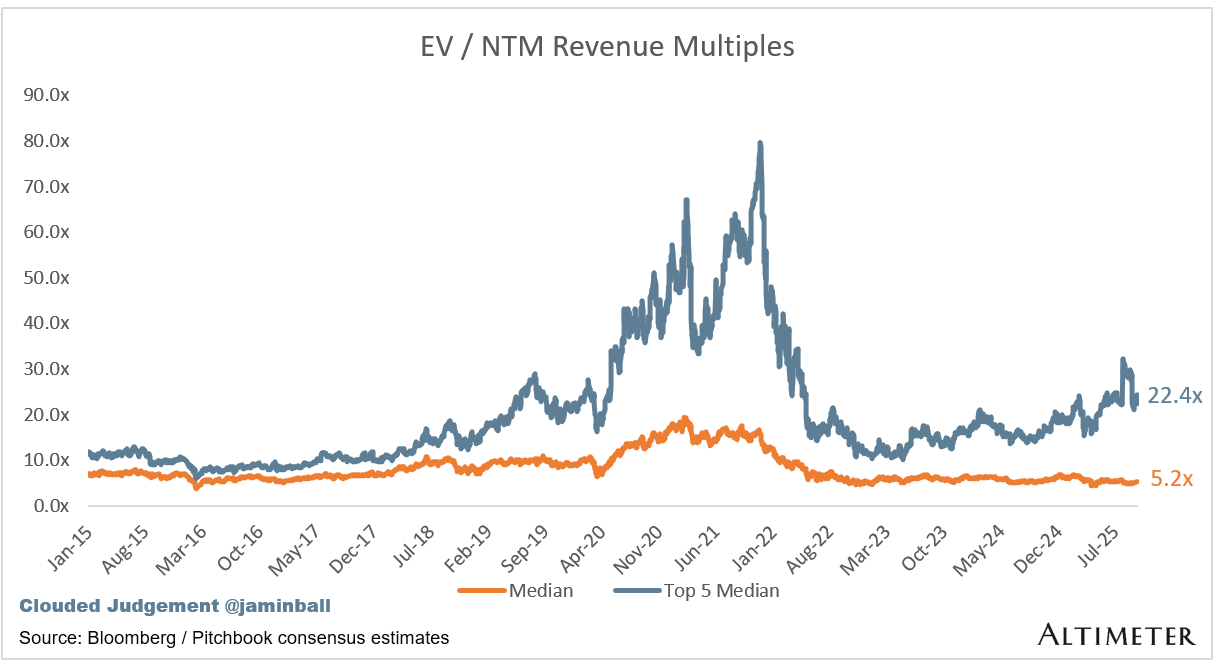

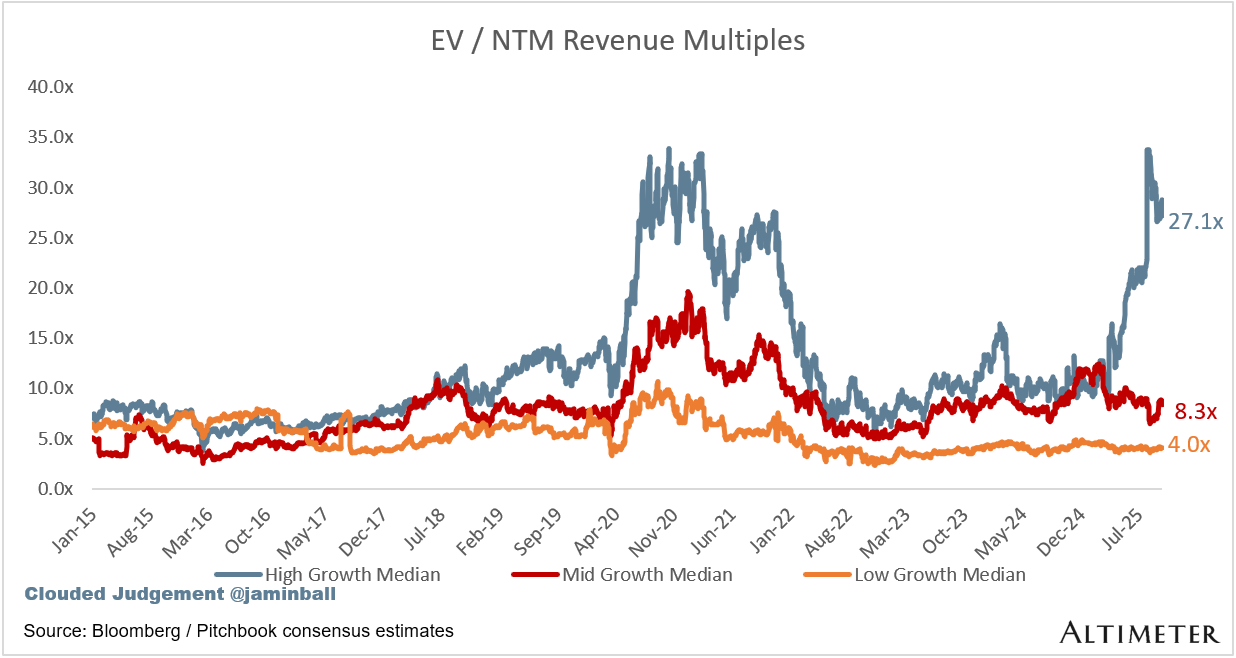

Update on Multiples

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 5.2x

Top 5 Median: 22.4x

10Y: 4.2%

Bucketed by Growth. In the buckets below I consider high growth >25% projected NTM growth, mid growth 15%-25% and low growth <15%

High Growth Median: 27.1x

Mid Growth Median: 8.3x

Low Growth Median: 4.0x

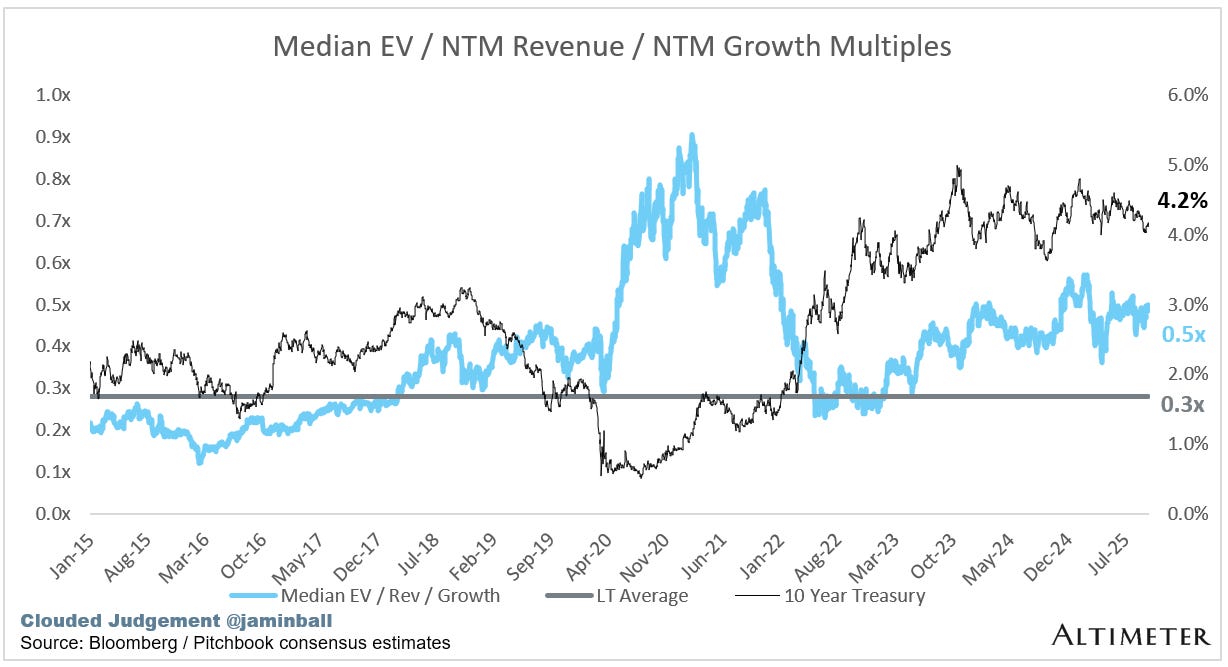

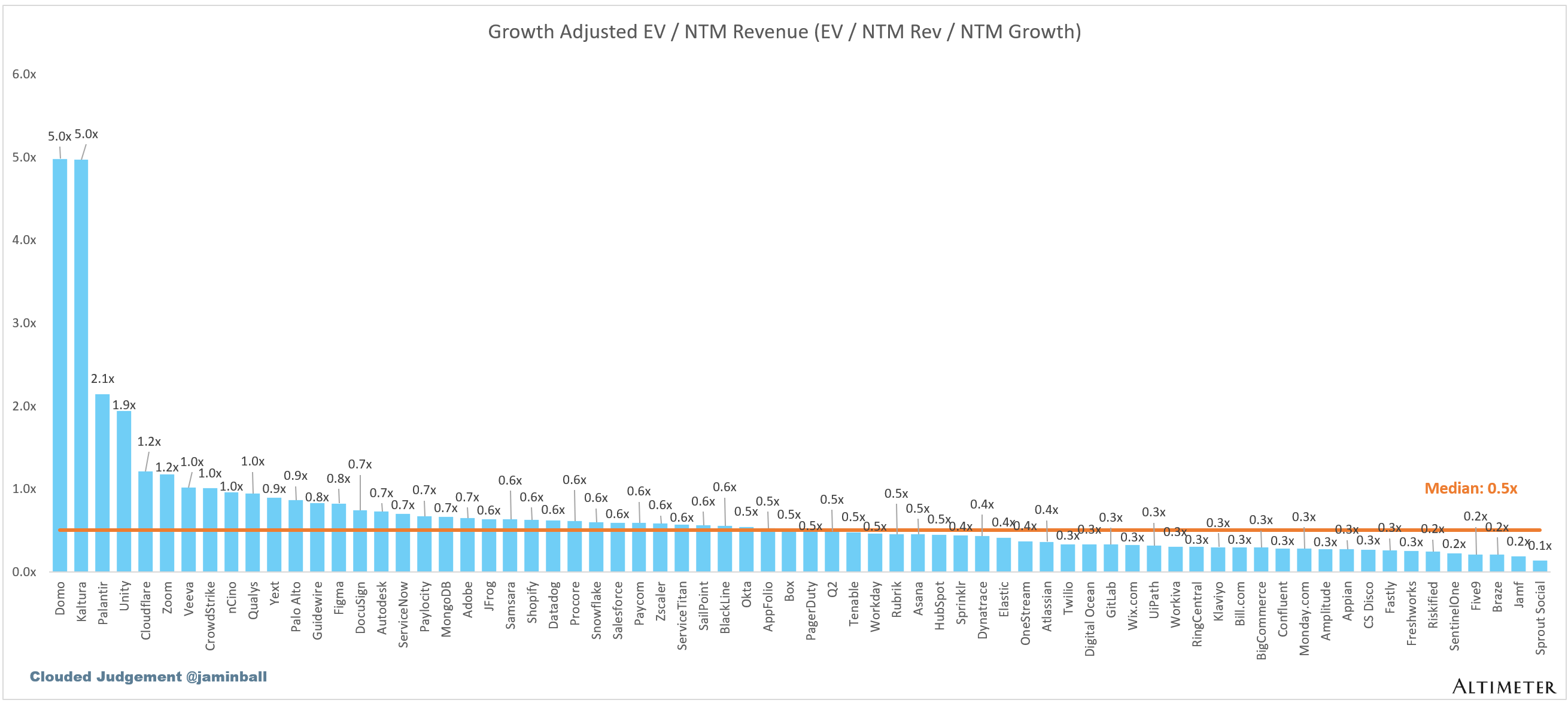

EV / NTM Rev / NTM Growth

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. So a company trading at 20x NTM revenue that is projected to grow 100% would be trading at 0.2x. The goal of this graph is to show how relatively cheap / expensive each stock is relative to its growth expectations.

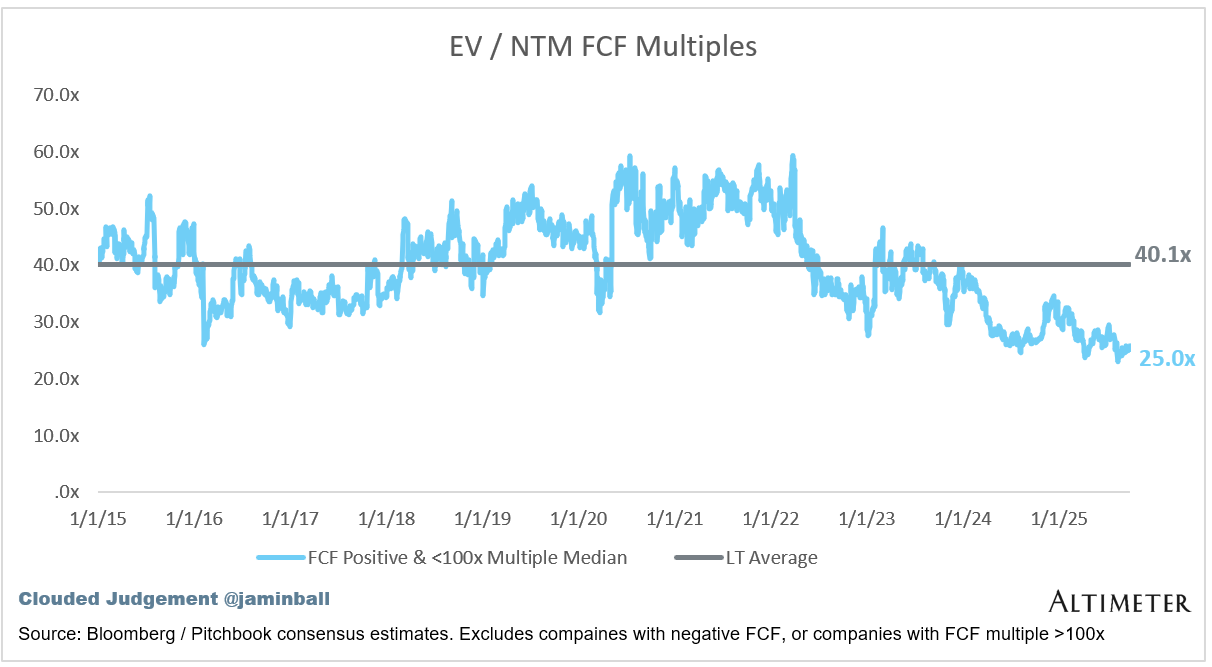

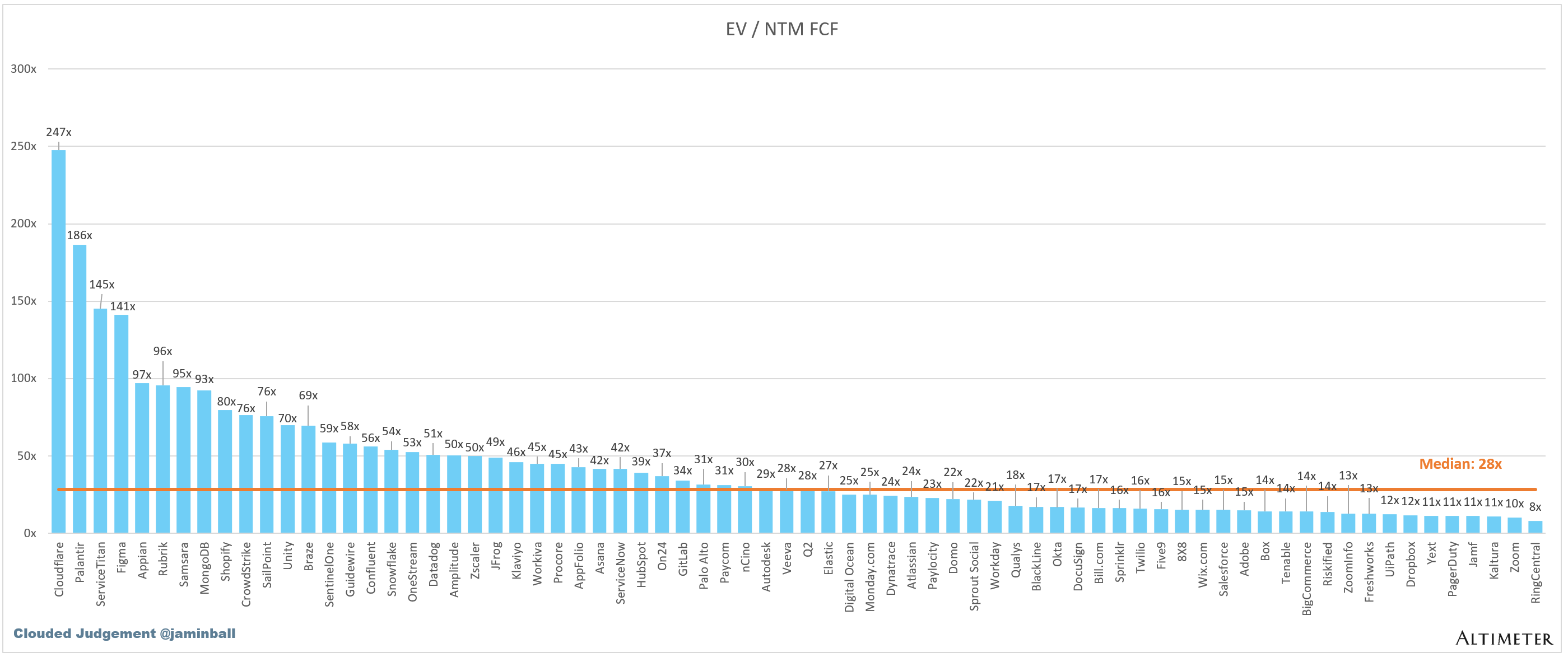

EV / NTM FCF

The line chart shows the median of all companies with a FCF multiple >0x and <100x. I created this subset to show companies where FCF is a relevant valuation metric.

Companies with negative NTM FCF are not listed on the chart

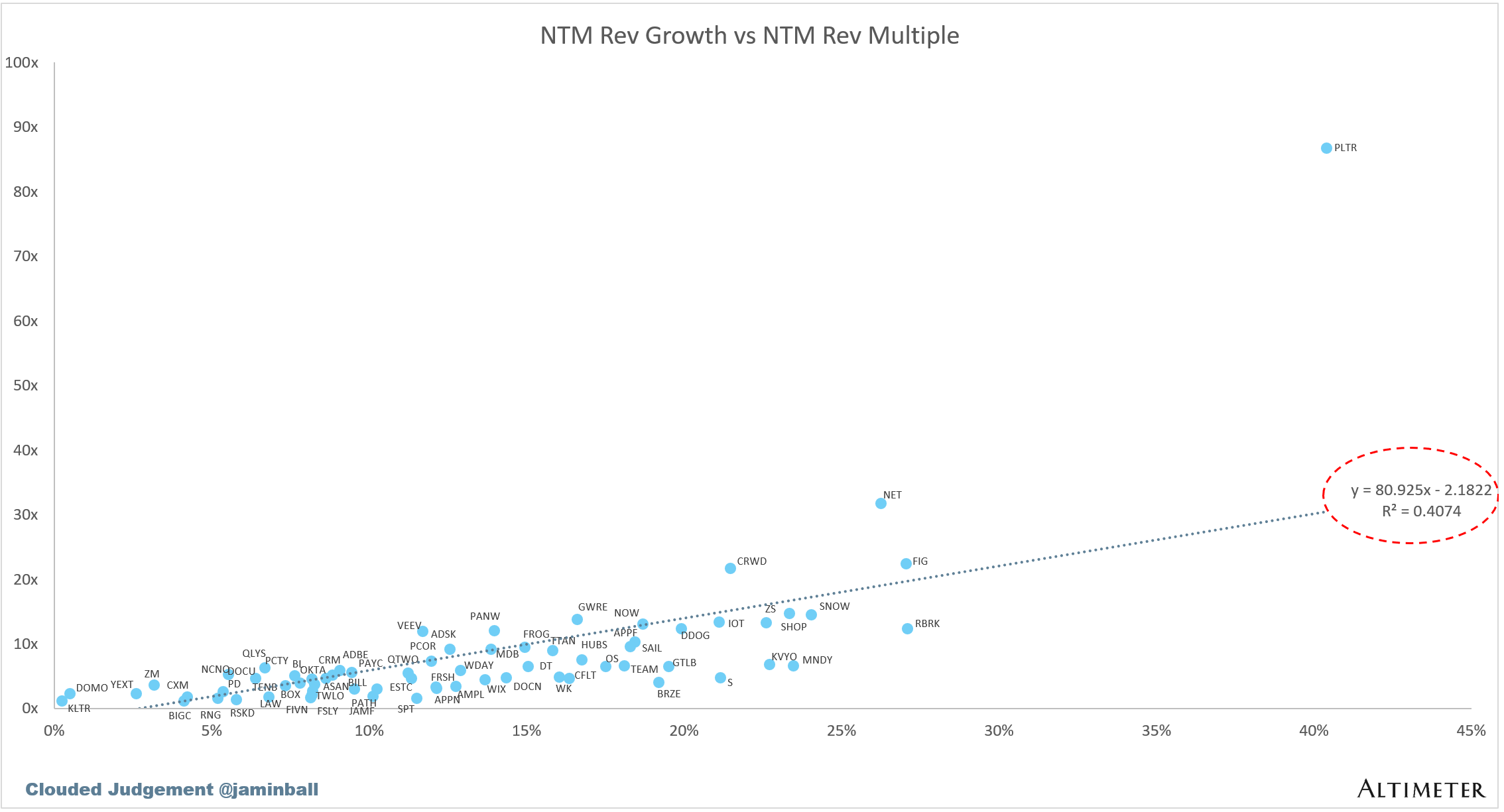

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Operating Metrics

Median NTM growth rate: 12%

Median LTM growth rate: 14%

Median Gross Margin: 76%

Median Operating Margin (2%)

Median FCF Margin: 18%

Median Net Retention: 108%

Median CAC Payback: 32 months

Median S&M % Revenue: 37%

Median R&D % Revenue: 24%

Median G&A % Revenue: 15%

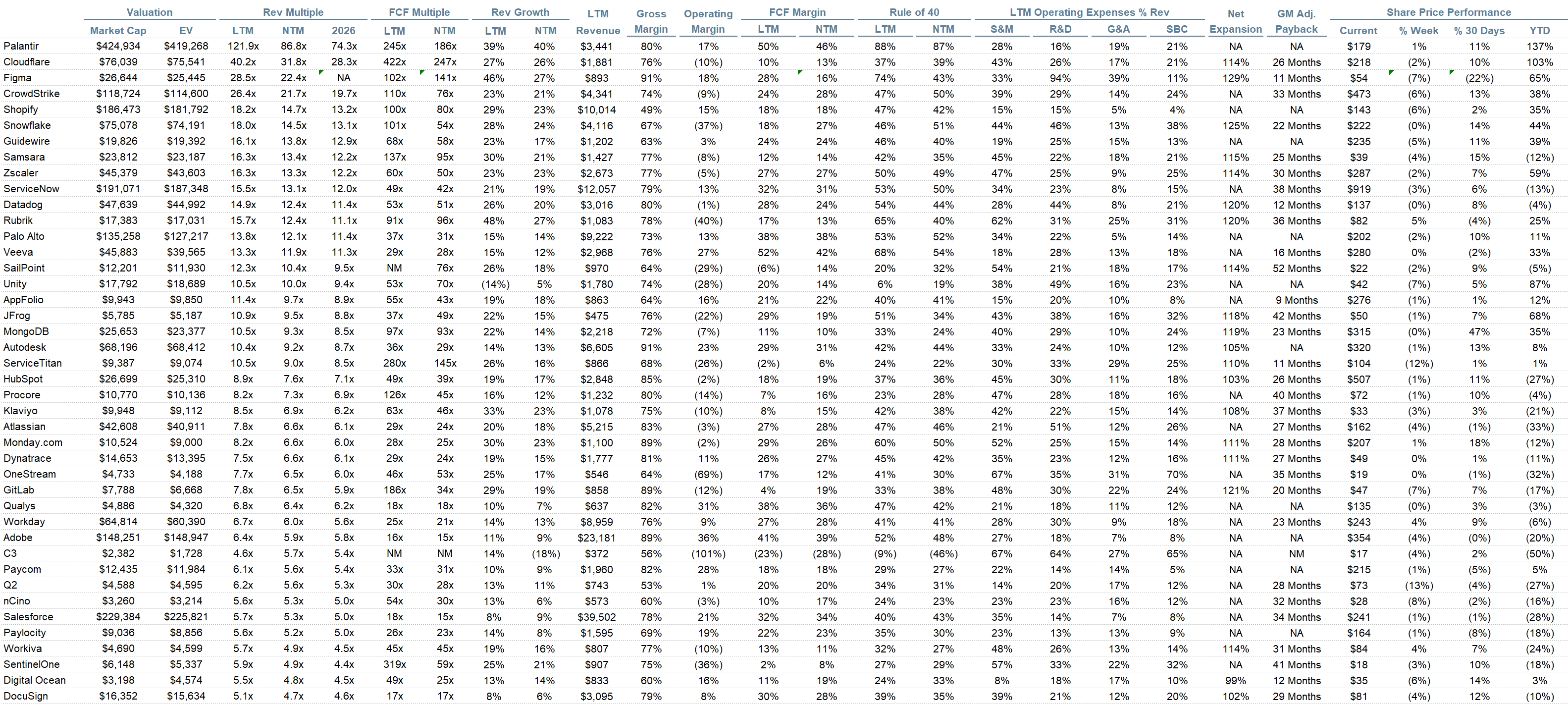

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12. It shows the number of months it takes for a SaaS business to pay back its fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Sources used in this post include Bloomberg, Pitchbook and company filings

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Really insightful take on revenue durability in hyper-growth AI companies - the point about not taking revenue for granted resonates. As these companies scale, managing cash flow, working capital, and trade credit becomes critical to sustaining that growth. TCLM offers practical frameworks for B2B finance leaders navigating these challenges. You might find it useful.

(It’s free)- https://tradecredit.substack.com/subscribe

Hyper growth: Fads are a thing, especially in uncertain times like now. During Covid Zoom grew like crazy. But after that spurt of adoption they have not leveraged their bigger footprint all that well so look like a one shot wonder. During the dot-com boom telcos sold IRUs (Internal Revenue Units or essentially their fiber optic lines) like crazy, only calling these asset sales leases. When you see a company selling the silver to make the quarter, that is a good time to sell. Similarly, the thing to watch for now not only with VC but actually for all of AI is real customer success. So enjoy the ride but watch like a hawk for real payback. Unfortunately, in times of great change the most successful applications will tend to be the most unexpected, so just watching casts the biggest net. Success here matters because really the bigger problem is some sort of cash flow will be needed to fund the $T data center build-out or our bond market, and dollar and economy will be toast.