Clouded Judgement 9.5.25 - Second Mover Advantage

Every week I’ll provide updates on the latest trends in cloud software companies. Follow along to stay up to date!

Second Mover Advantage

A few weeks back I wrote a post about why speed matters so much in the world of AI startups. Companies have to innovate / build quickly or risk irrelevance. Greenfield markets are up for grabs for the first mover. I wanted to write a follow up post that counters my original post :) And instead talk about why a “second mover advantage” exists in AI (and always has).

Google was second gen search (first gen was AltaVista, Lycos, Excite, yahoo, Ask Jeeves). Facebook was second gen social network (MySpace, Friendster). Databricks was second gen data processing (Hadoop was first). Datadog was second gen observability (New Relic, AppDynamics were first)

First movers can have an edge. They define categories, captured early adopters, and scaled before competitors could get get started. An argument can be made that it becomes hard to catch them because building feature parity took years and fighting a competitor with distribution was daunting.

But upon reflecting more, and observing more, the dynamics are a bit different (and especially so with AI). The space is moving so quickly that being early can actually be a handicap. Infrastructure, models, and best practices are changing at such a rapid pace that building too early means locking yourself into (what can ultimately become) fragile foundations. What looks cutting-edge one year can look dated the next, and this is challenging if it’s your foundation!

That’s where second movers come in, and they often have real advantages:

Learning from mistakes. First movers are forced to stumble through undefined standards, new infrastructure, and uncertain customer needs. Second movers get to observe what works, avoid the dead ends, and ship faster against a clearer roadmap.

Pricing and cost structure. When markets are greenfield, first movers often set very high prices. They can, because there is limited competition! That pricing supports their operating expenses, hiring plans, and overall business model. But when competitors enter with better tech and lower prices, it can be difficult for the first mover to respond. Their entire structure relies on maintaining those fat prices, while second movers can stay lean.

Educated buyers. The first wave has to evangelize the market, convincing customers they have a real problem and budget should be allocated. Second movers draft off that work. They enter a market where buyers already “get it” and are actively evaluating alternatives. A better product or pricing model finds a more receptive audience.

Faster catch-up. Historically, it might take years to match the functionality of a first mover. Today, with open-source models, APIs, and increasingly powerful developer tooling, catching up is dramatically faster. The moat of being first is shallower than it used to be.

Timing and ecosystem. Often the first mover is simply too early, before the ecosystem is ready, before customers can adopt, before complementary technologies exist. The second wave often arrives just as adoption curves accelerate and infrastructure matures.

In other words: being first isn’t always being best, especially in AI. The market is still greenfield, the technology stack is still fluid, and the pace of iteration is unlike anything we’ve seen before. Which is why the second wave of startups may actually have the bigger opportunity. And the way I view it, the second mover has the advantage over “third mover”

Now feels like the most exciting time to invest in AI startups, markets are starting to show maturity, customers are beginning to adopt at scale, and the real winners may not be the ones who were first, but the ones who arrived at the right time with the right product.

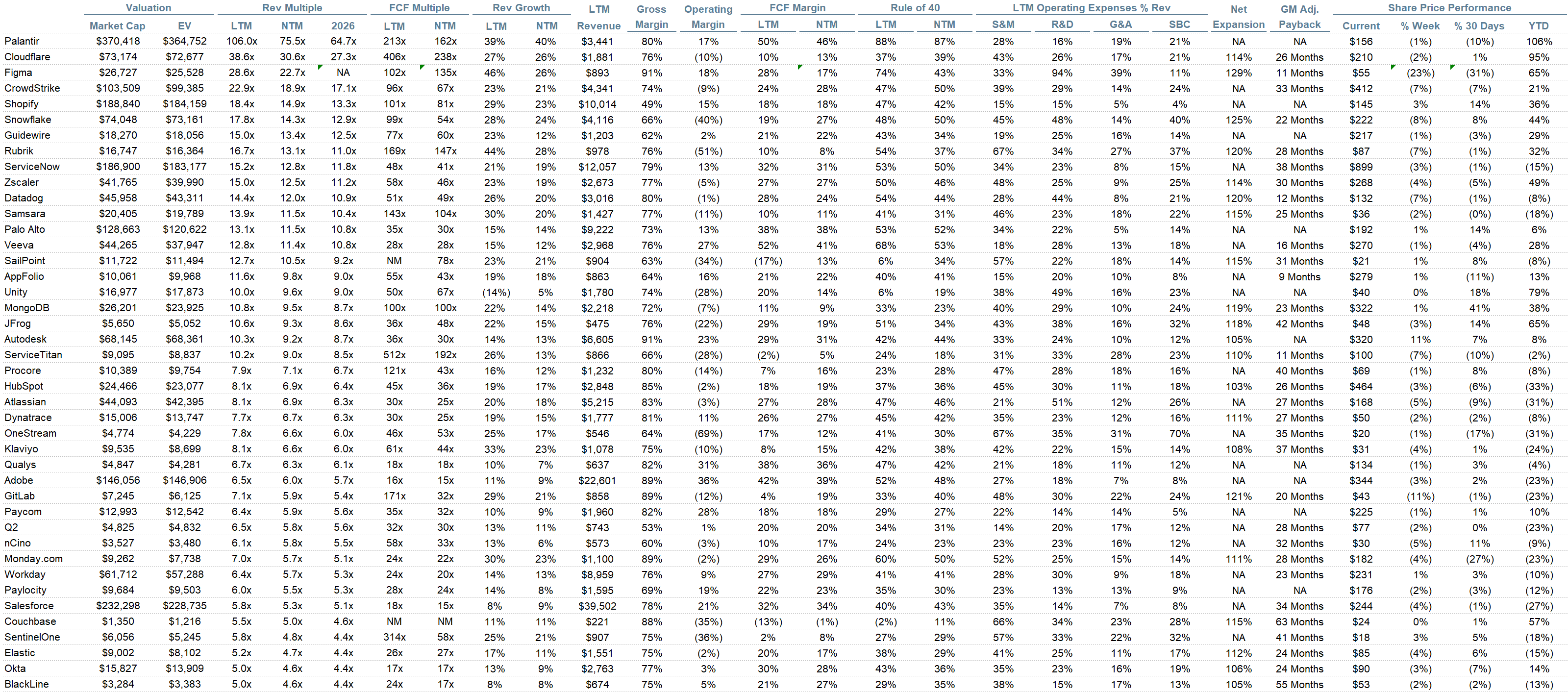

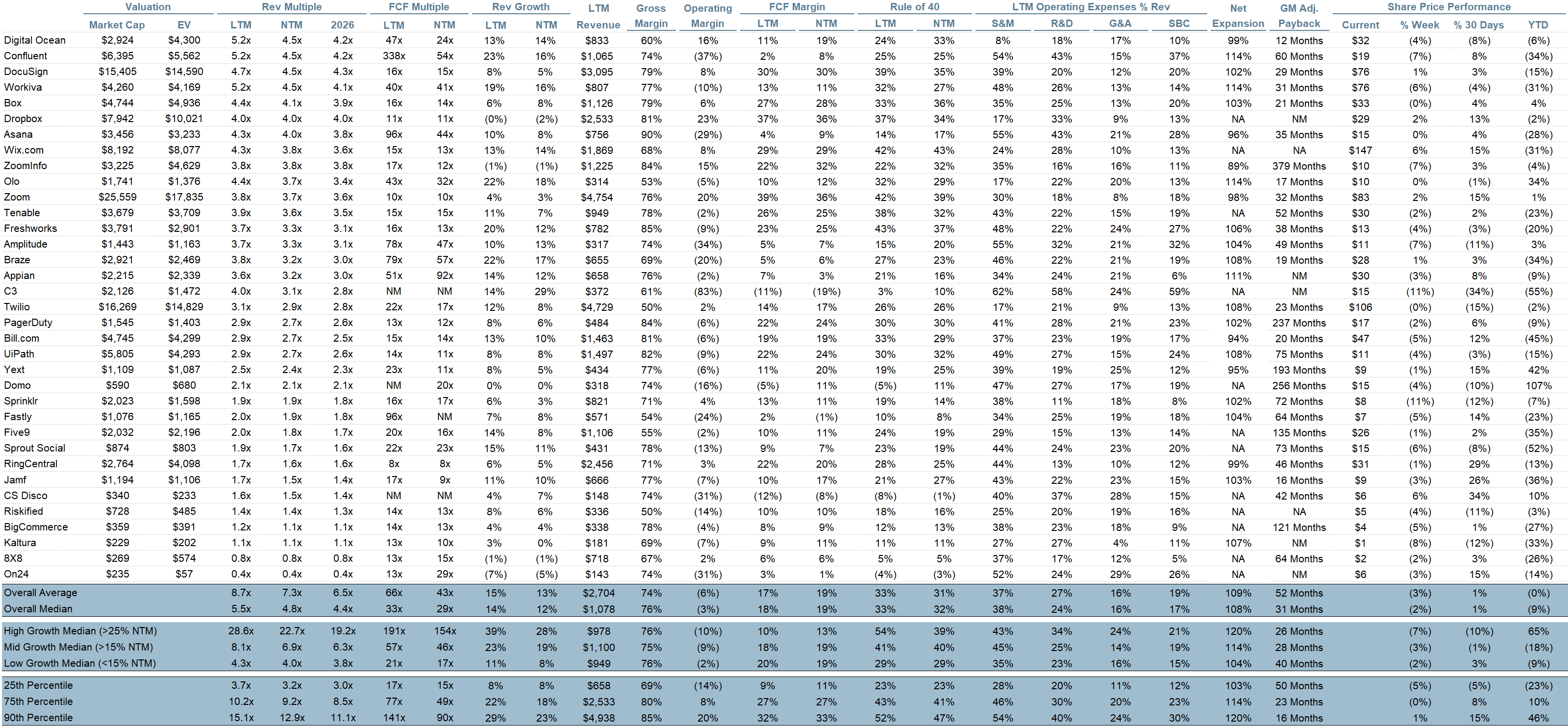

Quarterly Reports Summary

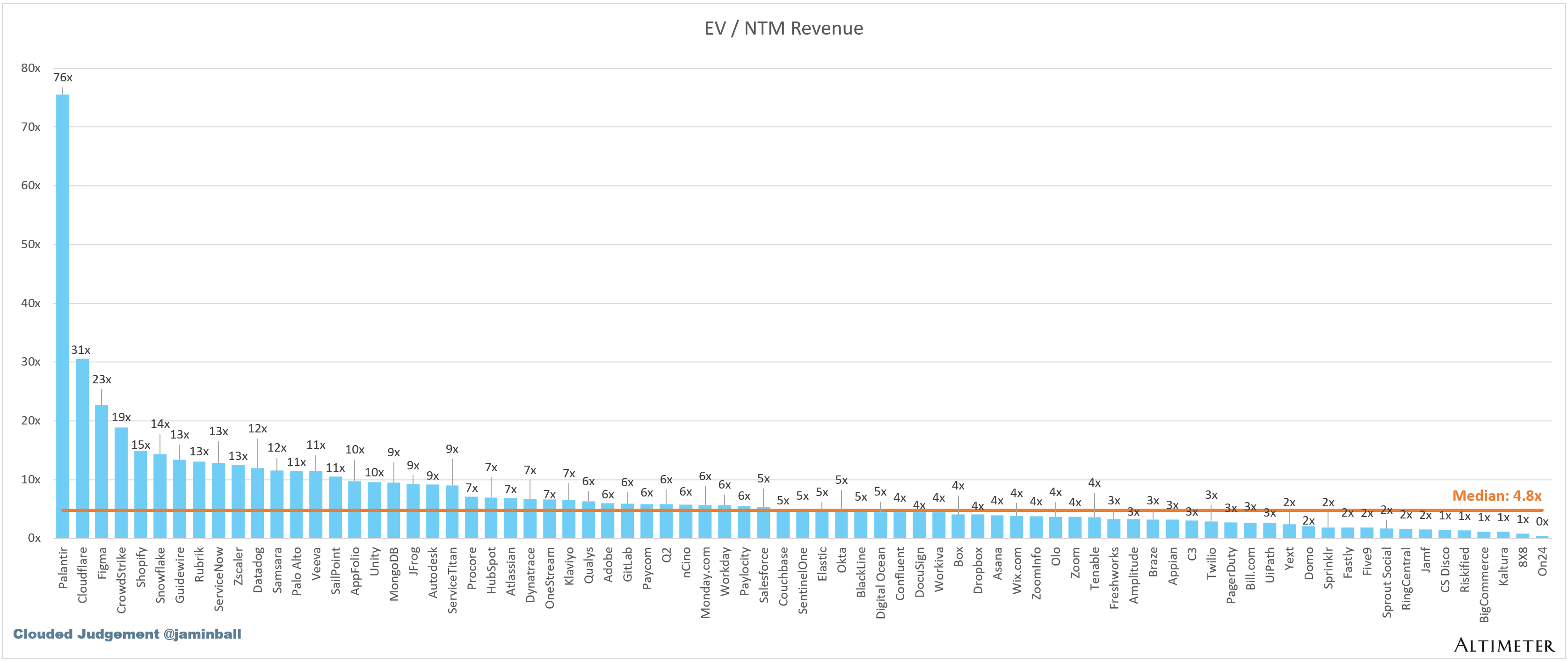

Top 10 EV / NTM Revenue Multiples

Top 10 Weekly Share Price Movement

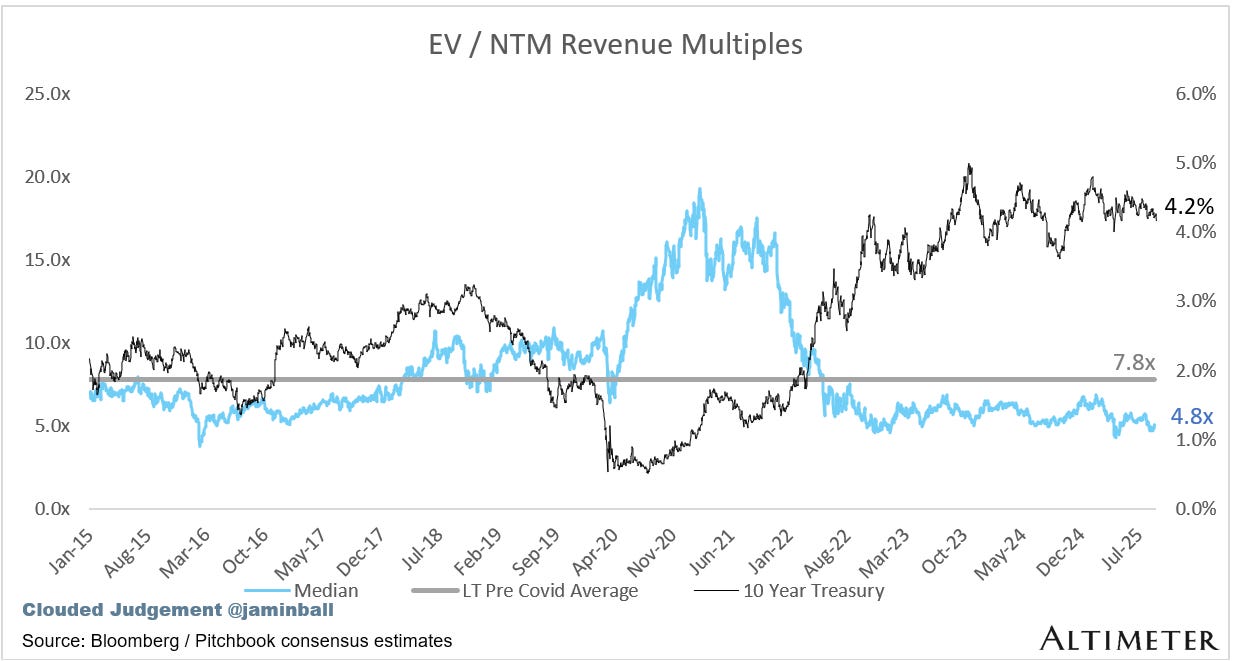

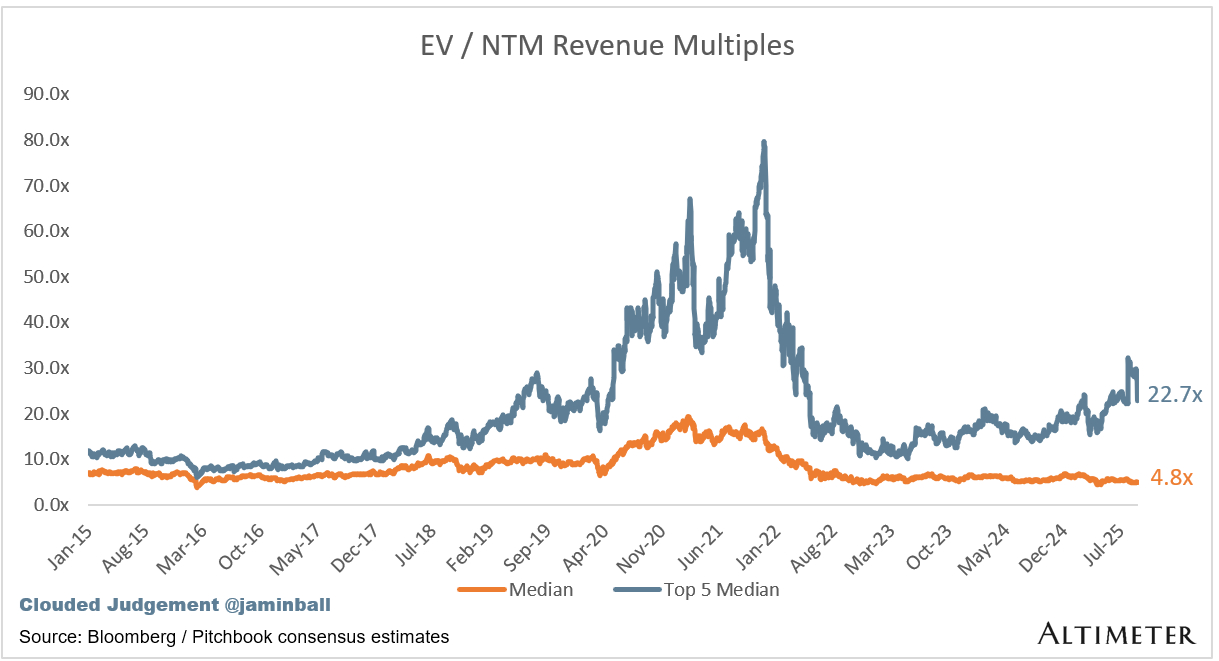

Update on Multiples

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 4.8x

Top 5 Median: 22.7x

10Y: 4.2%

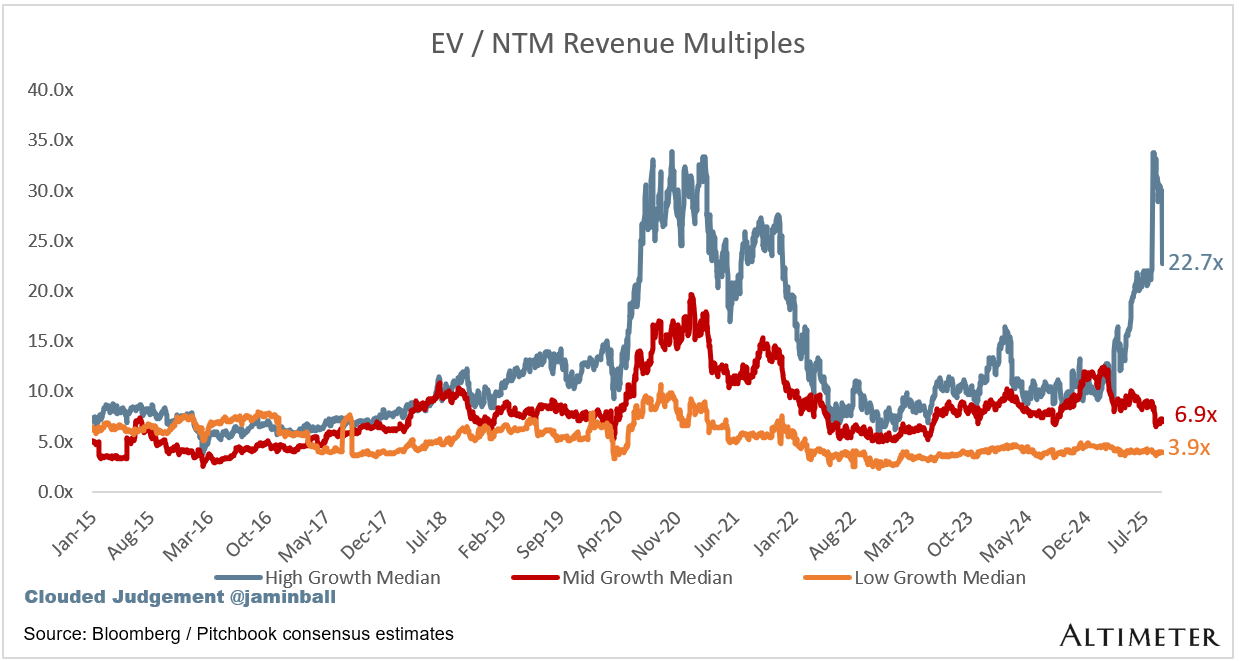

Bucketed by Growth. In the buckets below I consider high growth >25% projected NTM growth, mid growth 15%-25% and low growth <15%

High Growth Median: 22.7x

Mid Growth Median: 6.9x

Low Growth Median: 3.9x

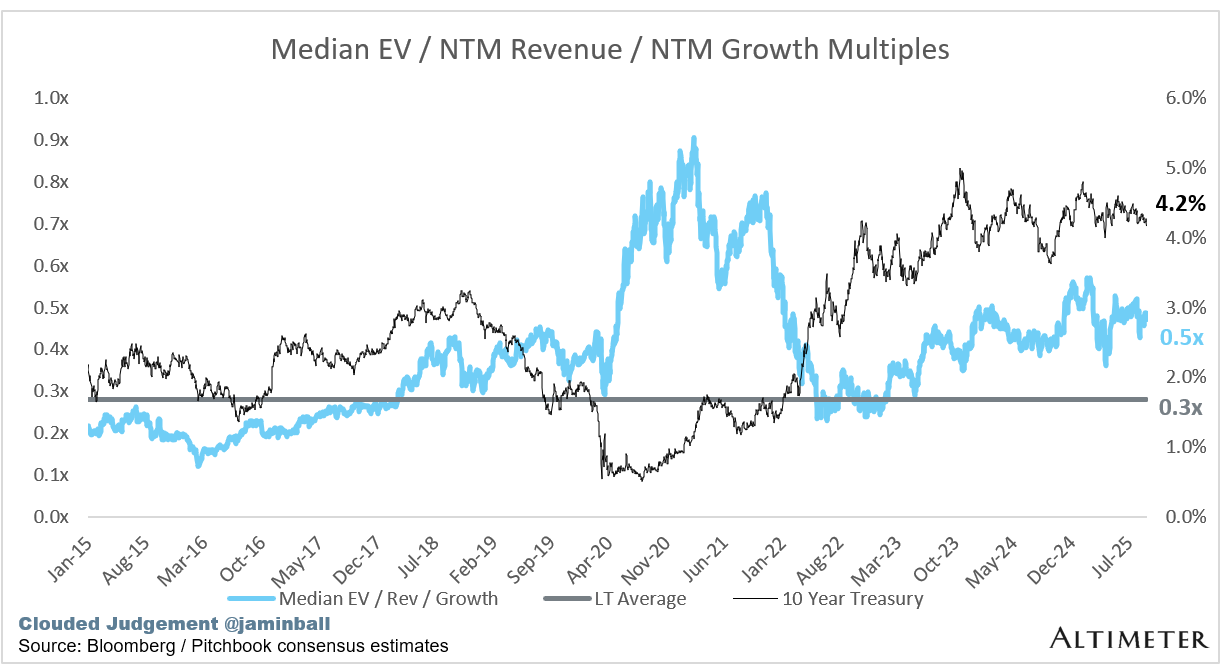

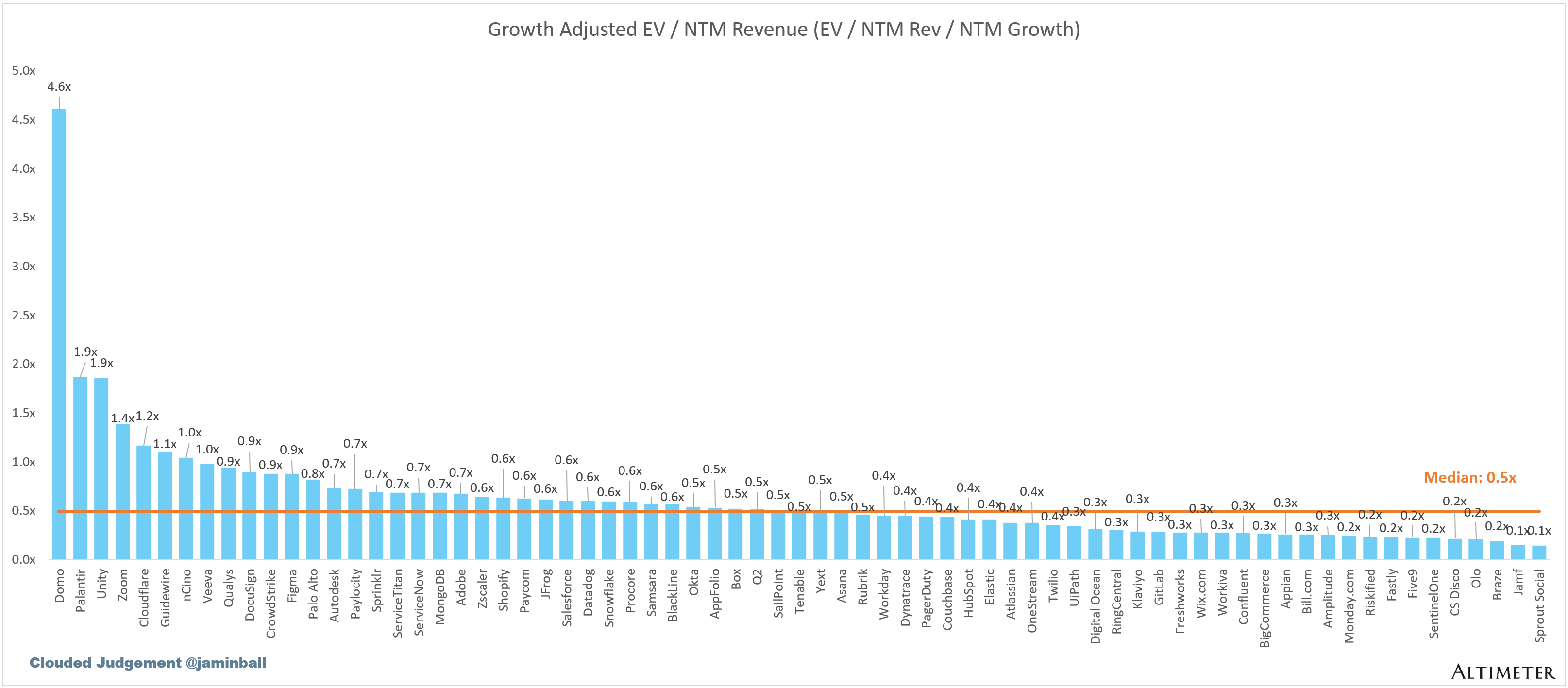

EV / NTM Rev / NTM Growth

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. So a company trading at 20x NTM revenue that is projected to grow 100% would be trading at 0.2x. The goal of this graph is to show how relatively cheap / expensive each stock is relative to its growth expectations.

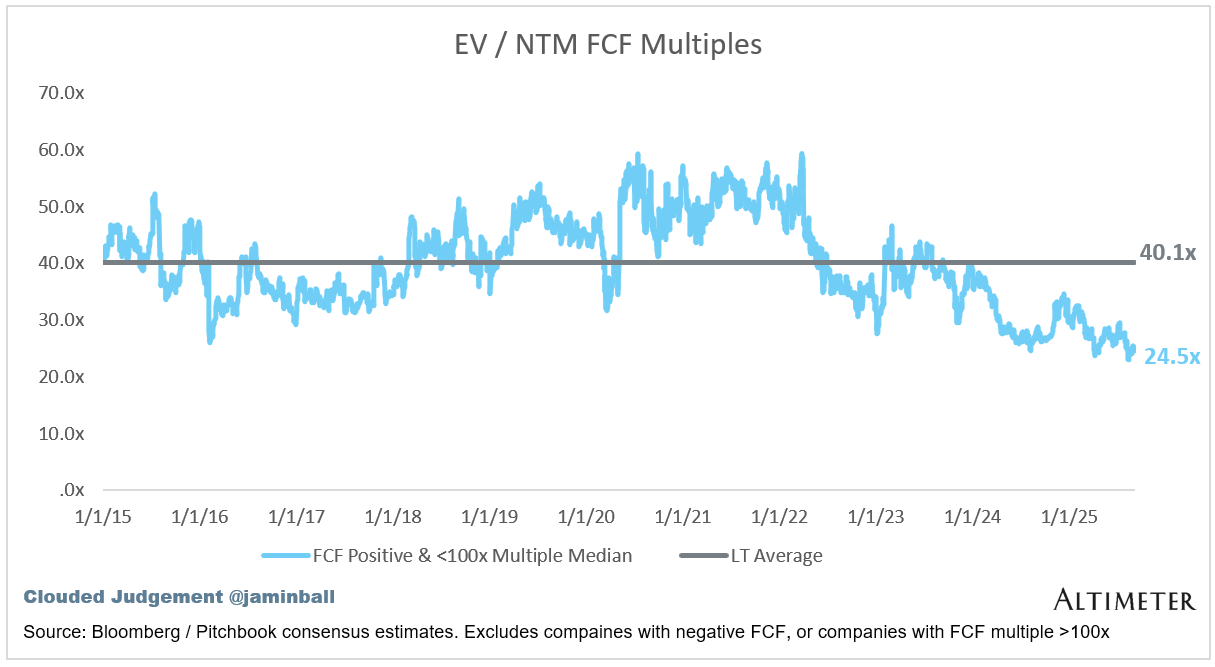

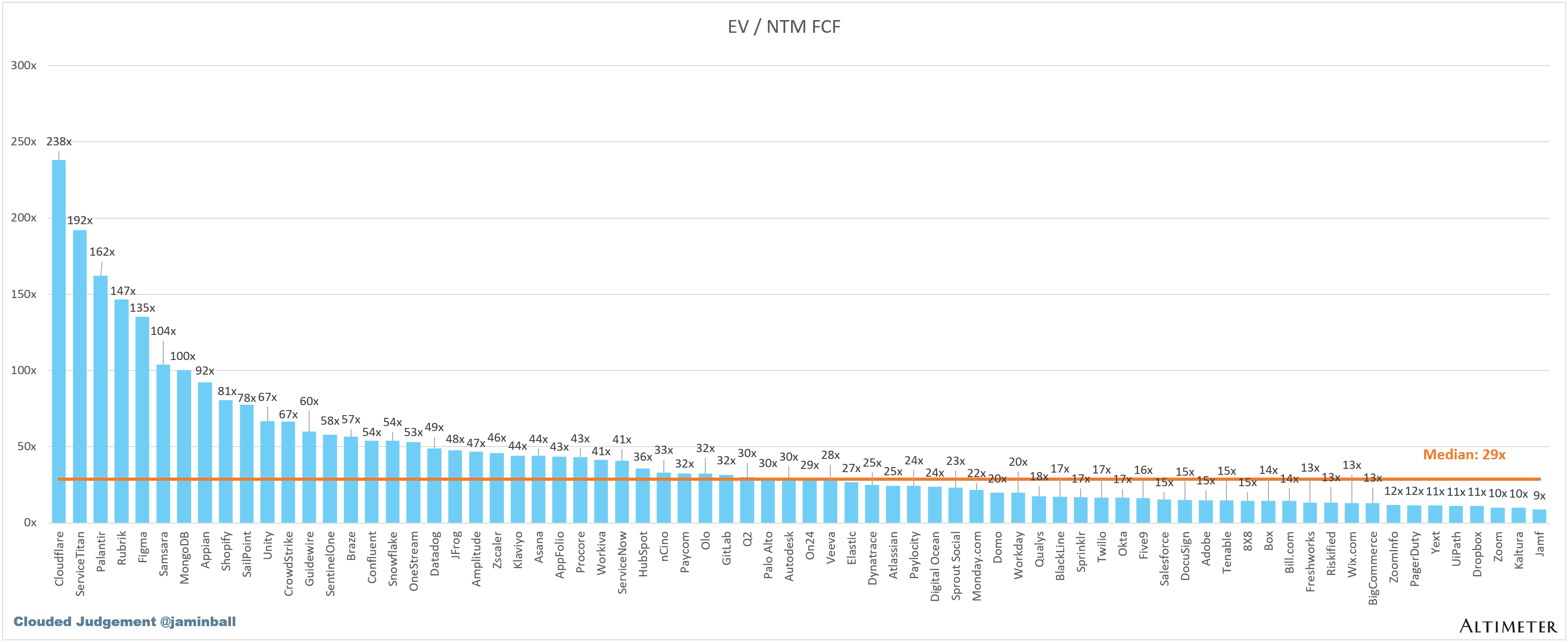

EV / NTM FCF

The line chart shows the median of all companies with a FCF multiple >0x and <100x. I created this subset to show companies where FCF is a relevant valuation metric.

Companies with negative NTM FCF are not listed on the chart

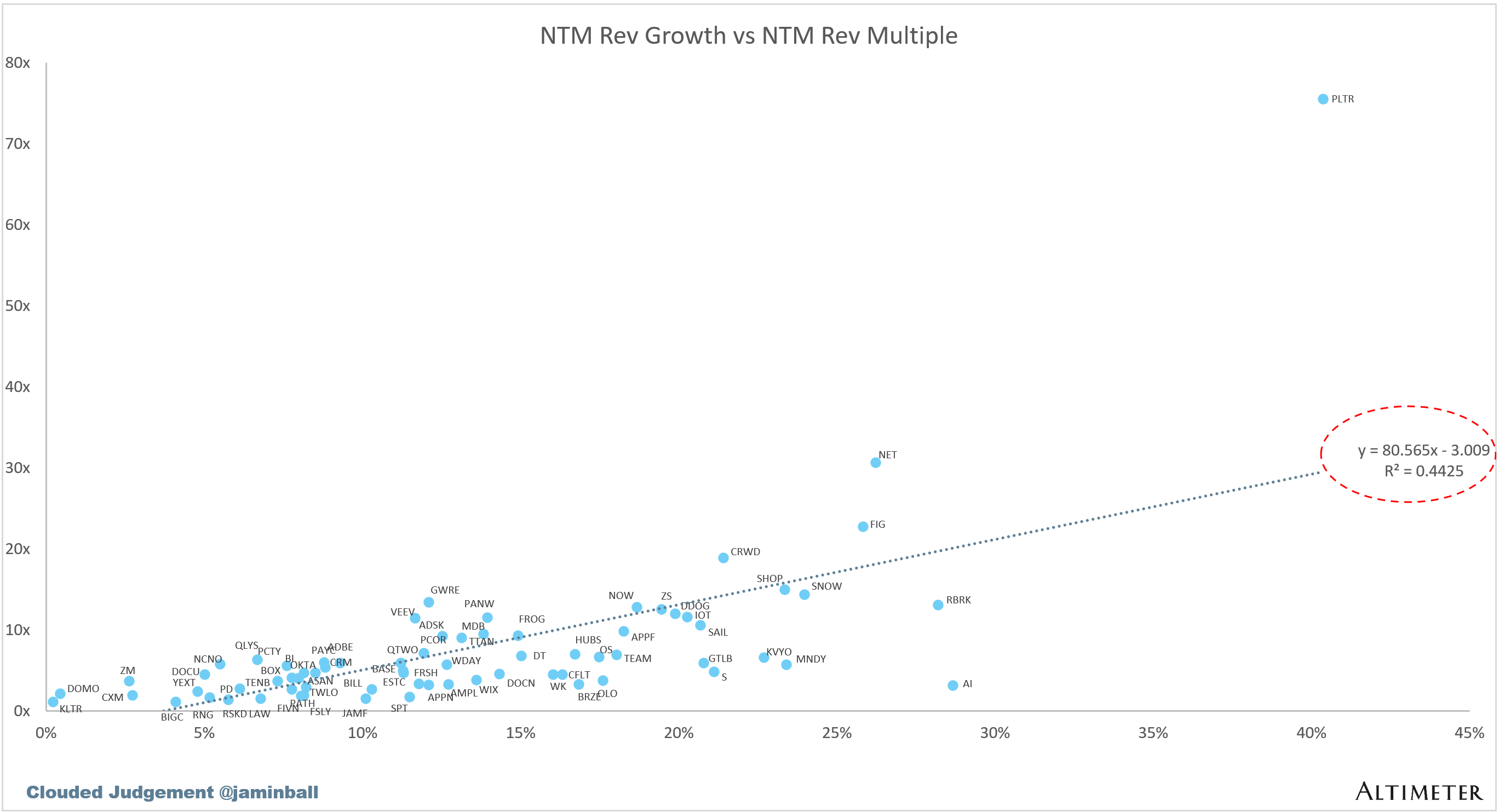

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Operating Metrics

Median NTM growth rate: 12%

Median LTM growth rate: 14%

Median Gross Margin: 76%

Median Operating Margin (3%)

Median FCF Margin: 18%

Median Net Retention: 108%

Median CAC Payback: 31 months

Median S&M % Revenue: 38%

Median R&D % Revenue: 24%

Median G&A % Revenue: 16%

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12. It shows the number of months it takes for a SaaS business to pay back its fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Sources used in this post include Bloomberg, Pitchbook and company filings

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

There might be a second mover advantage, if an AI company can find a leverage point the leader can't defend. Google had a technically more refined solution, FB was a much easier product to use, Datadog had a scope of use and low price point advantage. Current, I believe, the biggest challenge facing AI frontier companies is that they are losing so much money, the leverage points are access to capital and talent. It is great for consumers, as AI companies are subsidizing usage. I may pay $200+ per month to multiple AI companies, but I guarantee they lose money on me (and probably on you and most of their heavy users.)

I don't know if some company is going to "win" the AI wars, but the company that can innovate a self-sustaining, profitable business model will have a massive advantage.