Confluent - Benchmarking the S-1 Data

Yesterday Confluent filed their initial S1 statement. A S-1 is a document companies file with the SEC in preparation for listing their shares on an exchange like the NYSE or NASDAQ. The document contains a plethora of information on the company including a general overview, up to date financials, risk factors to the business, cap table highlights and much more. The purpose of the detailed information is to help investors (both institutional and retail) make informed investment decisions. There’s a lot of info to digest, so in the sections below I’ll try and pull out the relevant financial information and benchmark it against current cloud businesses. As far as an expected timeline - typically companies launch their roadshow ~3 weeks after filing their initial S-1 (the roadshow launches with an updated S-1 that contains a price range). After the roadshow launch there’s typically ~2 weeks before the stock starts trading. So we’re looking at roughly 5 weeks before any retail investor can buy the stock.

Confluent Overview

From the S1 - “Confluent is pioneering a fundamentally new category of data infrastructure focused on data in motion for developers and enterprises alike. In order for enterprises to deliver rich customer experiences, it is critical for all of their business functions, departments, teams, applications, and data stores to have complete connectivity, be thoroughly integrated, and be able to analyze data as it is generated. Confluent is designed to be this intelligent connective tissue by having real-time data from multiple sources constantly streamed across an enterprise for real-time analysis.”

Product Overview

From the S-1: “Our offering enables organizations to deploy production-ready applications that run across cloud infrastructures and data centers, and scales elastically, with enhanced features for security and compliance. Our platform provides the capabilities to fill the structural, operational, and engineering gap that is required for businesses to fully realize the power of data in motion. We enable software developers to easily build their initial applications to harness data in motion, and enable large, complex enterprises to make data in motion core to everything they do. As organizations mature in their adoption cycle, we enable them to build more and more applications that take advantage of data in motion. The results have a dual effect: businesses continuously improve their ability to provide better customer experiences and concurrently drive data-driven business operations. We believe that, over time, Confluent can become the central nervous system for modern digital enterprises, providing ubiquitous real-time connectivity and powering real-time applications across the enterprise.”

Market Opportunity

From the S-1: “Today, we believe our product roadmap targets each of the following four core Gartner-defined market segments: Application Infrastructure & Middleware, Database Management Systems, Data Integration Tools and Data Quality Tools,2 and Analytics and Business Intelligence.3 According to Gartner’s 2021 estimates, the aggregate of these four markets represents a total market size of approximately $149 billion. We estimate that we serve approximately $50 billion of this total market today, broken down as approximately $31 billion in Application Infrastructure & Middleware (excluding Full Life Cycle API Management, BPM Suites, TPM, RPA, and DXPs), $7 billion in Database Management Systems (excluding Prerelational-era DBMS), $7 billion in Analytics and Business Intelligence (excluding Traditional BI Platforms), and $4 billion in Data Integration Tools and Data Quality Tools (excluding other Data Integration Software). Based upon the above Gartner data and Gartner’s estimates for 2024 total market size in these four segments, we have estimated that our total market opportunity will increase to $91 billion in these four market segments by 2024, representing a 22% compounded annual growth rate.”

How Confluent Makes Money

From the S-1: “We offer our software under licenses intended to protect our innovation. This includes our Confluent Community License and a traditional proprietary commercial license. Our Confluent Community License allows developers to access our source code to give them a chance to utilize some of our platform features, but explicitly restricts others, including cloud vendors, from taking this source code and using it to offer a competing software-as-a-service, or SaaS, offering.”

Benchmark Data

The data shown below depicts how the Confluent data compares to the operating metrics of current public cloud businesses.

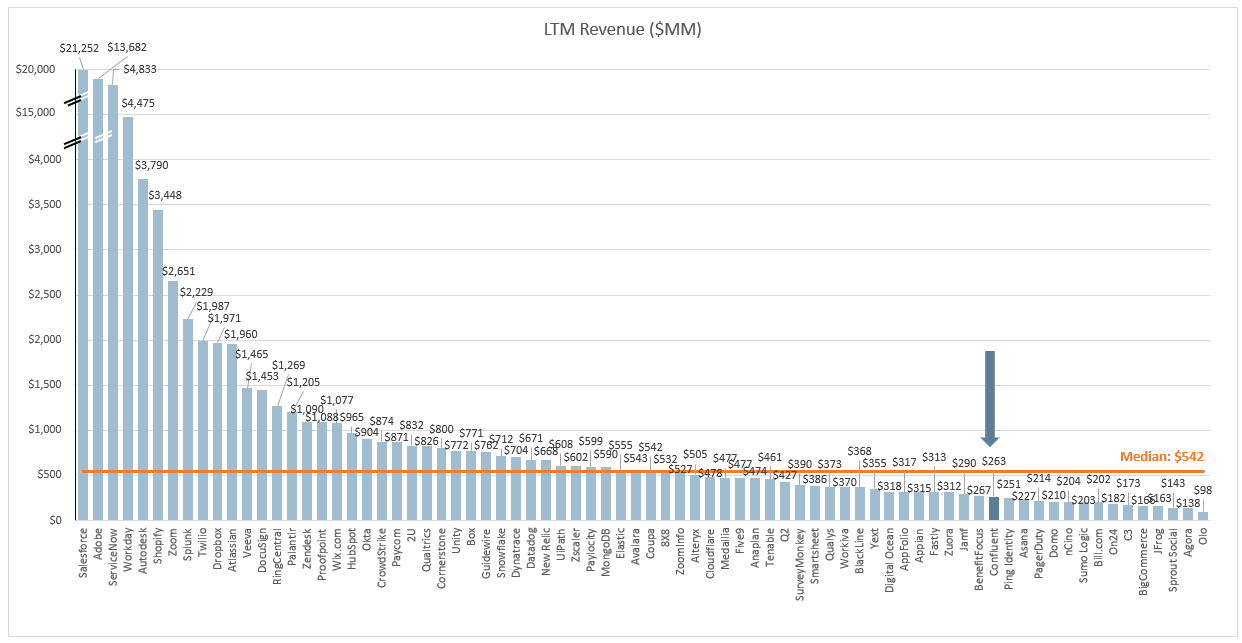

Last Twelve Months (LTM) Revenue

Confluent’s LTM revenue was $263M

LTM Revenue Growth

Confluent grew 53% over the last 12 months

Quarterly YoY Revenue Growth Trends

LTM GAAP Gross Margin

Confluent’s LTM gross margin was 69%

LTM GAAP Operating Margin

Confluent’s LTM operating margin was (93%). However, for reasons I get into in my embedded tweet below, I think the more appropriate figure to use for them is closer to (50%)

Net Revenue Retention

This metric is calculated by taking the annual recurring revenue of a cohort of customers from 1 year ago, and comparing it to the current annual recurring revenue of that same set of customers (even if you experienced churn and that group of customers now only has 9, or anything <10).

Confluent’s net revenue retention was 117%

Gross Margin Adjusted CAC Payback

(Previous Q S&M) / (Net New ARR x Gross Margin) x 12. This metric demonstrates how long it takes (in months) for a customer to pay back the cost at which it took to acquire them. In the chart below I’m taking the average of the 4 quarters leading up to IPO to normalize the business.

Confluent’s payback period was ~39 months

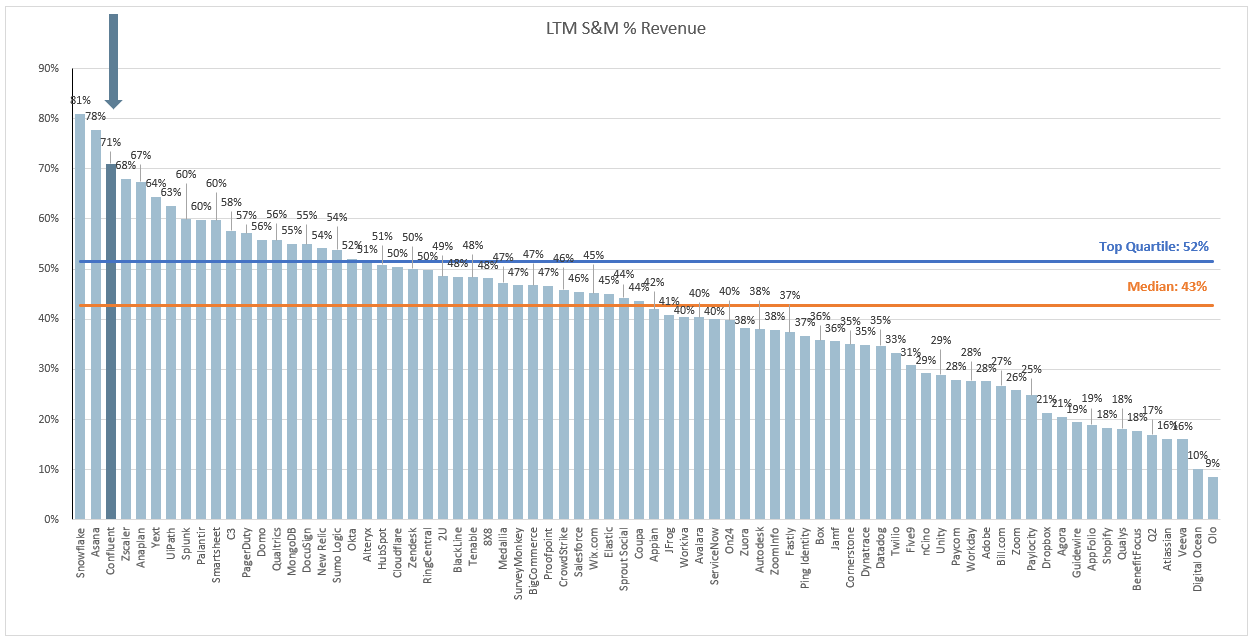

LTM S&M Expense as % of LTM Revenue

Confluent spent 71% of their LTM revenue on S&M

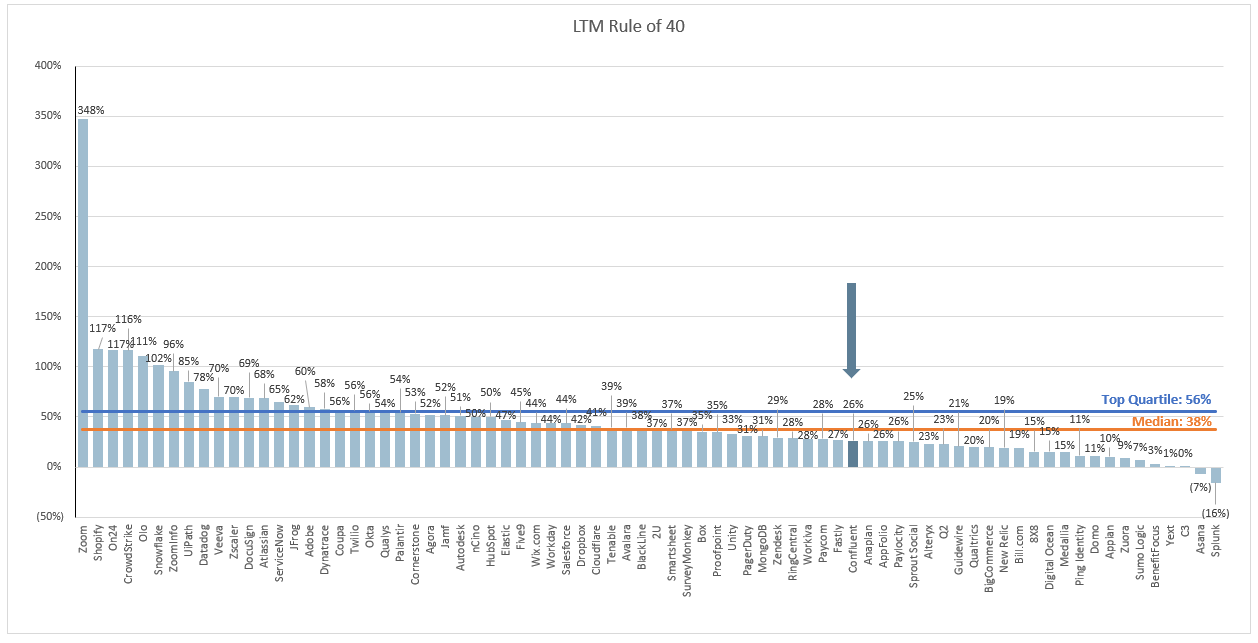

Rule of 40

In the below chart I’m showing LTM revenue growth + LTM FCF margin. Confluent’s LTM Rule of 40 was 26%

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

I was looking forward to this IPO but the financials don't seem to be anything special compared to other SaaS companies. Do you know what the valuation will be (EV / NTM)

Thanks for the great post, Jiamin. Just wondering why rule of 40 is calculated as LTM rev growth + LTM FCF margin as opposed to profit margin. Thanks.