JFrog: Benchmarking the S1 Data

Today JFrog filed their initial S1 statement. A S1 is a document companies file with the SEC in preparation for listing their shares on an exchange like the NYSE or NASDAQ. The document contains a plethora of information on the company including a general overview, up to date financials, risk factors to the business, cap table highlights and much more. The purpose of the detailed information is to help investors (both institutional and retail) make investment decisions. There’s a lot of info to digest, so in the sections below I’ll try and pull out the relevant financial information and benchmark it against current cloud businesses. As far as an expected timeline - typically companies launch their roadshow ~3 weeks after filing their initial press release (this is where we get a price range). After the roadshow launch there’s typically ~2 weeks before the stock starts trading. So we’re looking at roughly 5 weeks before any retail investor can buy the stock.

JFrog Overview

From the S1 - “We provide an end-to-end, hybrid, universal DevOps Platform to achieve Continuous Software Release Management, or CSRM. Our leading CSRM platform enables organizations to continuously deliver software updates across any system. Our platform is the critical bridge between software development and deployment of that software, paving the way for the modern DevOps paradigm. We enable organizations to build and release software faster and more securely while empowering developers to be more efficient…We built the world’s first universal package repository, JFrog Artifactory, to fundamentally transform the way that the software release cycle is managed. Our package-based approach to releasing software enabled the category of CSRM, allowing software releases to be continuous and software to always be current. We enable organizations to store all package types in a common repository where they can be edited, tracked, and managed. Our unified platform connects all of the software release processes involved in building and releasing software, enabling CSRM. We empower our customers to shorten their software release cycles and enable the continuous flow of current, up-to-date software from any source to any destination. Our platform is designed to be agnostic to the programming languages, source code repositories, and development technologies that our customers use, and the type of production environments to which they deploy.”

“We believe that our products represent not only a functional tool to be used by IT, DevOps, and security professionals, but also a fundamental shift in the software development landscape. As DevOps practices are increasingly adopted around the world and across industries, we believe that our products can address the CSRM needs of organizations globally, while requiring minimal to no product localization. We estimate our current market opportunity for CSRM to be approximately $22 billion.”

Benchmark Data

The data shown below depicts how the JFrog data compares to the operating metrics of current public SaaS businesses.

Last Twelve Months (LTM) Revenue

As you can see, JFrog is on the smaller end with $128M of LTM revenue

LTM Revenue Growth

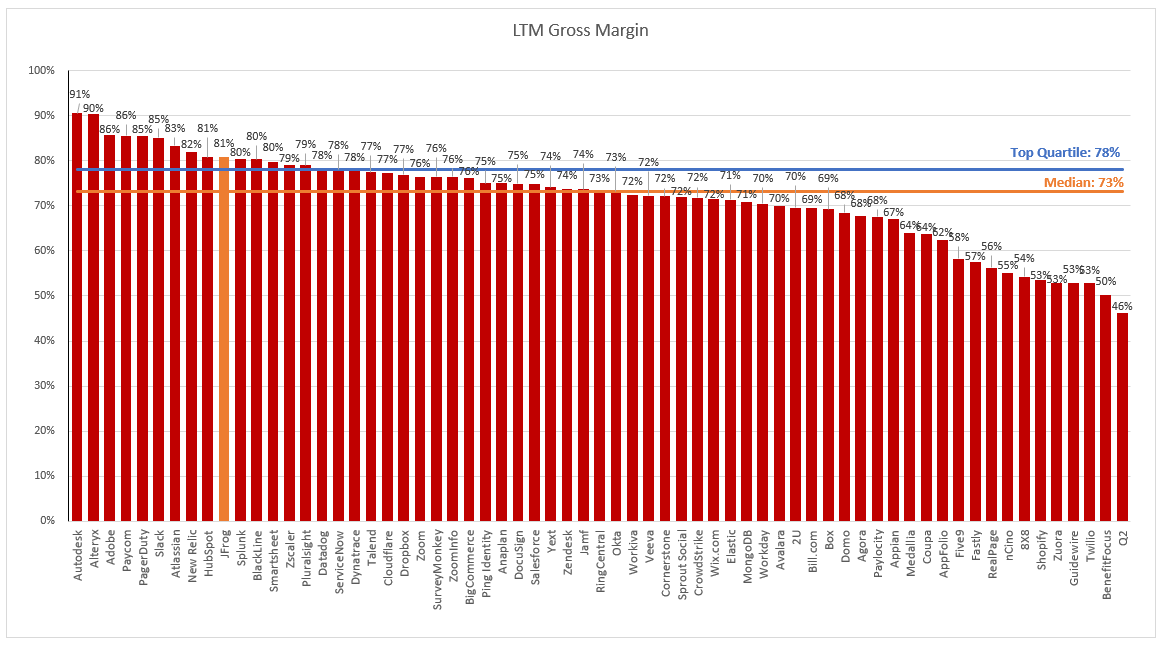

LTM GAAP Gross Margin

LTM GAAP Operating Margin

LTM Rule of 40

This is showing the LTM growth rate + LTM FCF Margin

Net Revenue Retention

This metric is calculated by taking the annual recurring revenue of a cohort of customers from 1 year ago, and comparing it to the current annual recurring revenue of that same set of customers (even if you experienced churn and that group of customers now only has 9, or anything <10).

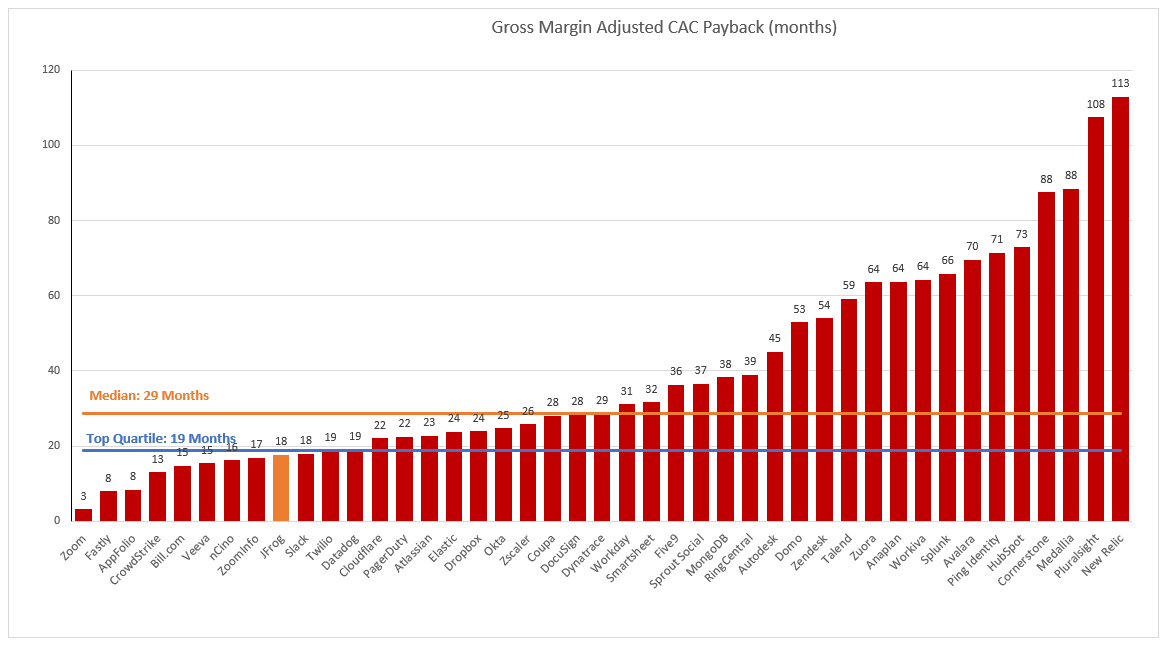

Gross Margin Adjusted CAC Payback

(Previous Q S&M) / (Net New ARR x Gross Margin) x 12. This metric demonstrates how long it takes (in months) for a customer to pay back the cost at which it took to acquire them. In the chart below I’m taking the average of the 4 quarters leading up to IPO to remove any seasonality out outliers.

Valuation

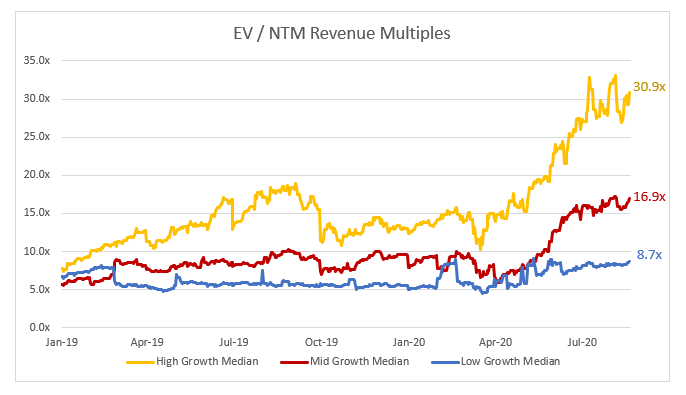

Predicting the valuation of pending IPOs is nearly impossible, but it adds to the fun to make predictions! In the SaaS / Cloud world companies are valued off a multiple of their revenue. Generally this is a projected revenue number, and for the purpose of this analysis I will be looking at NTM (next twelve months) projections. When I think about what a company will be worth I first like to look at how other public companies are valued. First, let’s look at what SaaS multiples are trading at today, bucketed by growth:

When I try and imagine where JFrog should trade, I like to look at the metrics in the section above. My takeaway - JFrog has some pretty incredible financials. Their revenue growth, gross margin, Rule of 40, net retention and GM adjusted CAC payback are all in the top quartile (and many are in the top decile!). And their GAAP Operating Margin is just outside the top quartile (they’re almost GAAP Profitable!) Because of this I’m quite confident JFrog will garner a PREMIUM multiple. Right now the top 10 SaaS multiples range from 30x - 43X. My take and prediction (pending any material change in mutiples) - JFrog will trade at ~39x NTM revenue out of the gate, giving it a valuation of $7B on the first day of trading!

hi Jamin, thanks for a very well written analysis of JFrog S1 filing great job :) May I check will you be doing benchmarking S1 data for Snowflake (SNOW) IPO filing ? Thanks, BK

As always, great summary Jamin. I love JFrog's unit economics and their operating metrics look almost just as impressive. I agree it should demand a premium when the stock starts trading. The TAM seems pretty small, but I think we constantly see these TAMs expanding with new uses cases as technologies develop.

I have a question as it relates to the service offering itself. Wouldn't edge computing render JFrog almost useless for companies? If developers are creating applications and building software updates at the edge closer to users, then a company wouldn't need a central repository to do so. This could definitely be me not fully understanding the technology, but something I was thinking about when reading through the summary.