Unity: Benchmarking the S1 Data

Today Unity filed their initial S1 statement. A S1 is a document companies file with the SEC in preparation for listing their shares on an exchange like the NYSE or NASDAQ. The document contains a plethora of information on the company including a general overview, up to date financials, risk factors to the business, cap table highlights and much more. The purpose of the detailed information is to help investors (both institutional and retail) make investment decisions. There’s a lot of info to digest, so in the sections below I’ll try and pull out the relevant financial information and benchmark it against current cloud businesses. As far as an expected timeline - typically companies launch their roadshow ~3 weeks after filing their initial press release (this is where we get a price range). After the roadshow launch there’s typically ~2 weeks before the stock starts trading. So we’re looking at roughly 5 weeks before any retail investor can buy the stock.

Unity Overview

From the S1 - “Unity is the world’s leading platform for creating and operating interactive, real-time 3D content. Our platform provides a comprehensive set of software solutions to create, run and monetize interactive, real-time 2D and 3D content for mobile phones, tablets, PCs, consoles, and augmented and virtual reality devices. As of June 30, 2020, we had approximately 1.5 million monthly active creators in over 190 countries and territories worldwide. The applications developed by these creators were downloaded over three billion times per month in 2019 on over 1.5 billion unique devices. Unity has built its reputation in gaming, and our scale and reach in this industry are significant. We estimate that in 2019, on a global basis, 53% of the top 1,000 mobile games on the Apple App Store and Google Play and over 50% of such mobile games, PC games and console games combined were made with Unity.”

“We believe today we address a total market opportunity of approximately $29 billion across both gaming and other industries. Gaming: In gaming, we estimate the market opportunity for our Create Solutions and Operate Solutions to be approximately $12 billion in 2019 across over 15 million potential creators, growing to over $16 billion in 2025, based on a 2020 study that we commissioned by a third party strategy consulting firm, Altman Vilandrie & Company. Industries Beyond Gaming: In industries beyond gaming, we estimate the market opportunity for our Create Solutions and Operate Solutions to be approximately $17 billion today, based on the number of software developers, architects and designers our solutions could potentially serve.”

How Unity Makes Money

“We generate subscription and associated professional services revenue from the sale of Create Solutions. We generate revenue-share and usage-based revenue from the sale of Operate Solutions. To a lesser extent, we also generate revenue from fixed fee, royalty and revenue-share arrangements through our Strategic Partnerships with hardware, operating system, device, game console, and other technology providers.”

Benchmark Data

The data shown below depicts how the Unity data compares to the operating metrics of current public SaaS businesses.

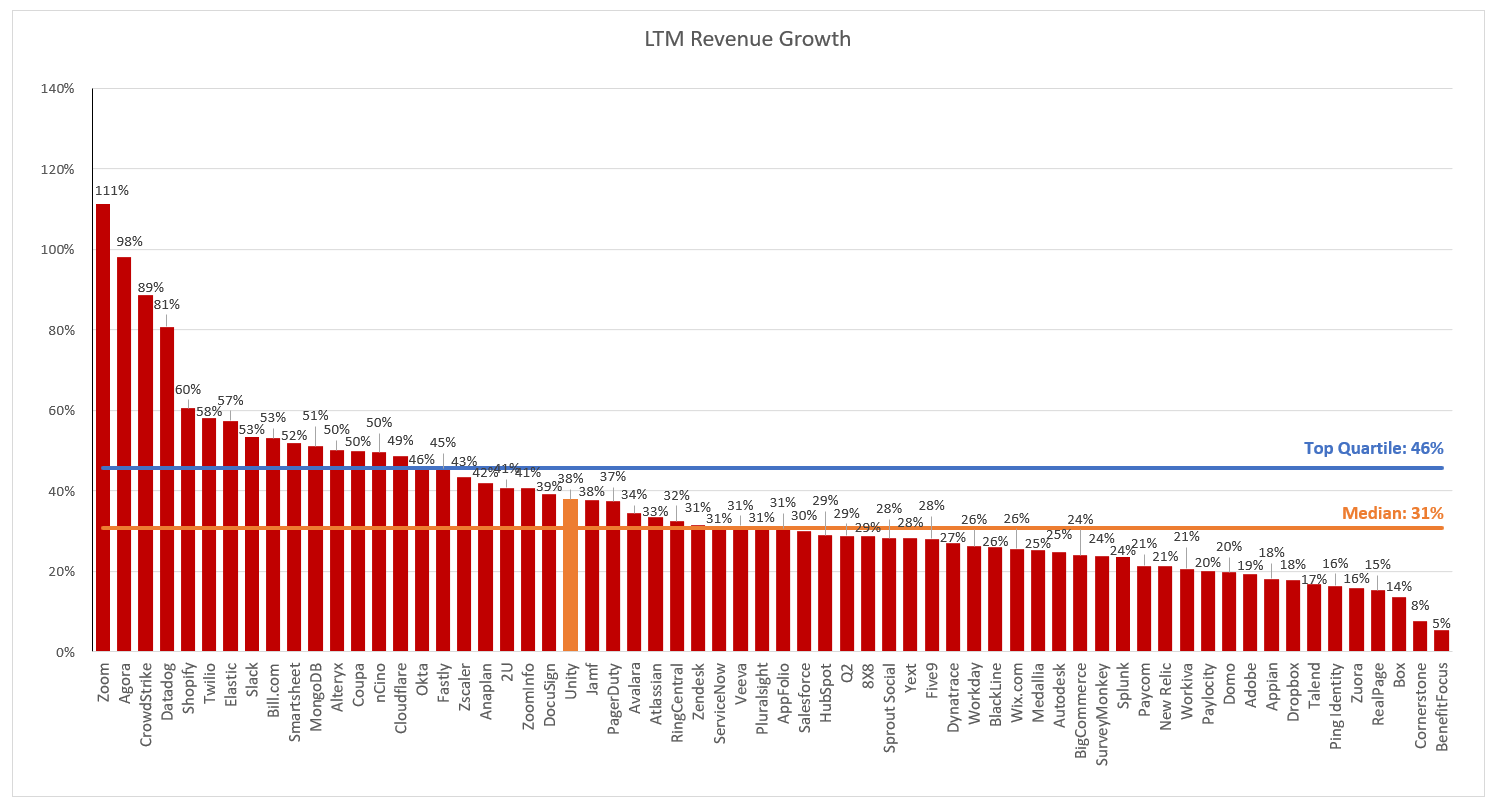

Last Twelve Months (LTM) Revenue

LTM Revenue Growth

Quarterly YoY Revenue Growth Trends

It’s interesting to see revenue growth accelerating in the most recent quarter

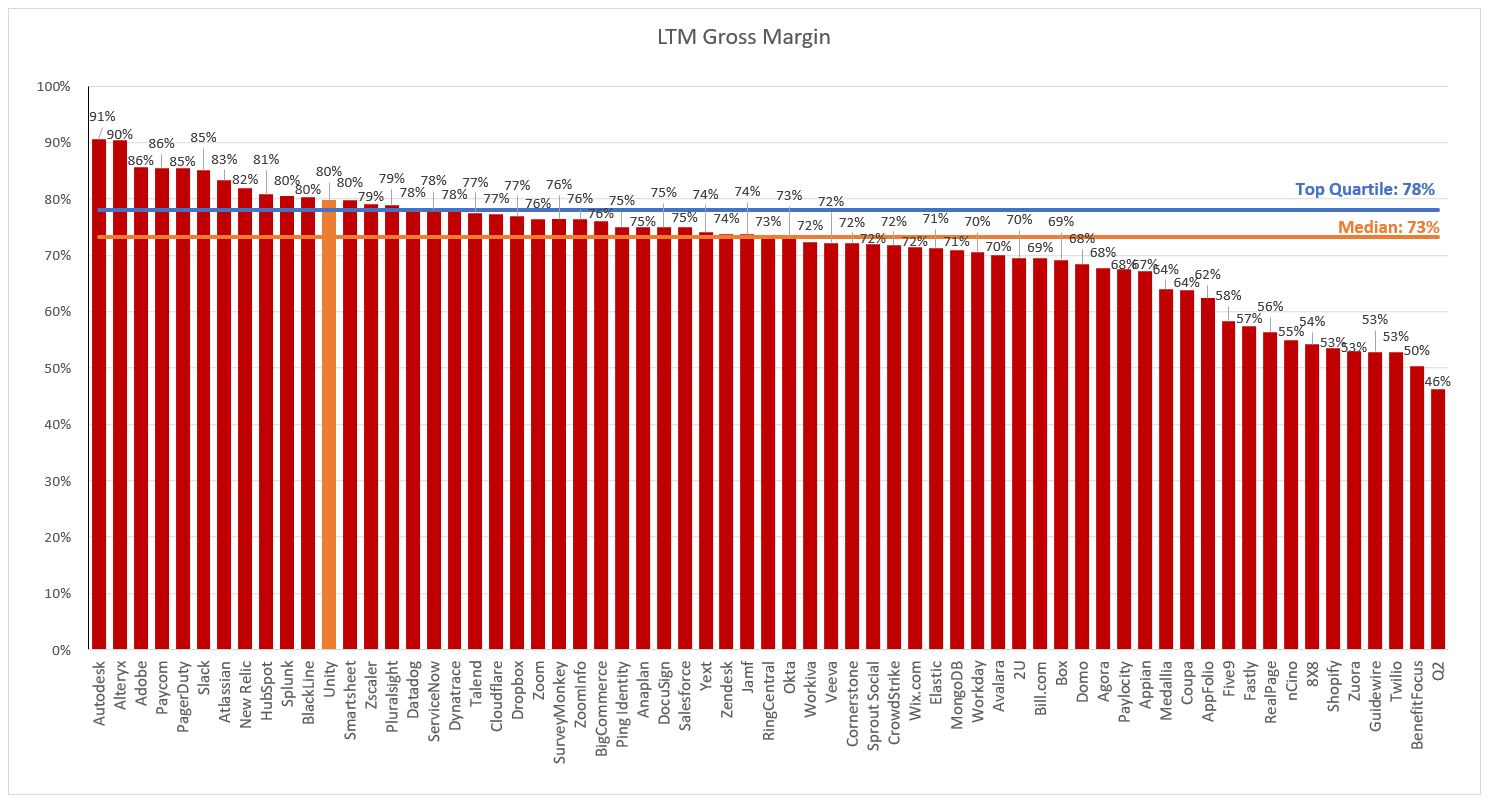

LTM GAAP Gross Margin

LTM GAAP Operating Margin

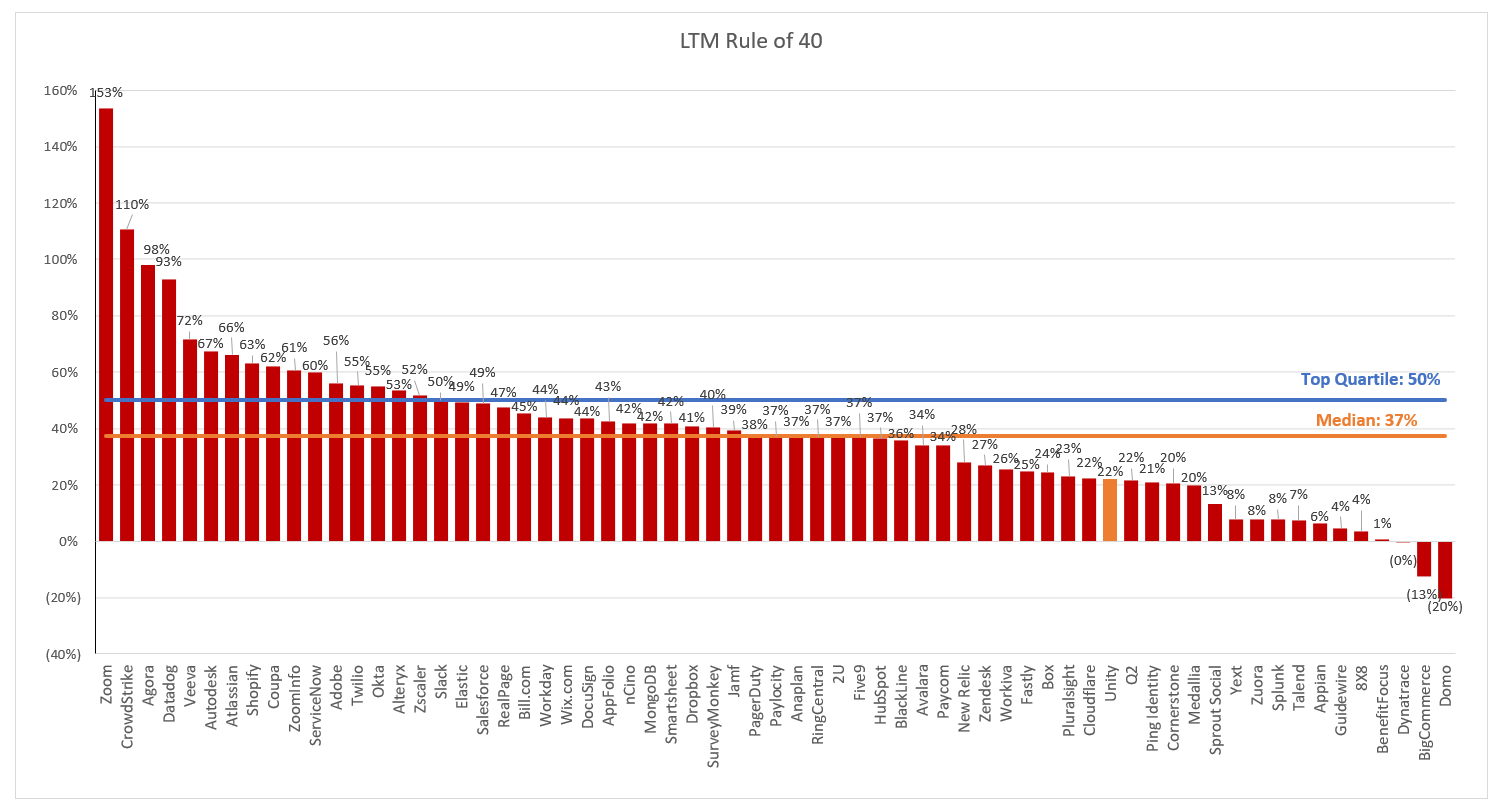

LTM Rule of 40 (LTM Growth + LTM FCF Margin)

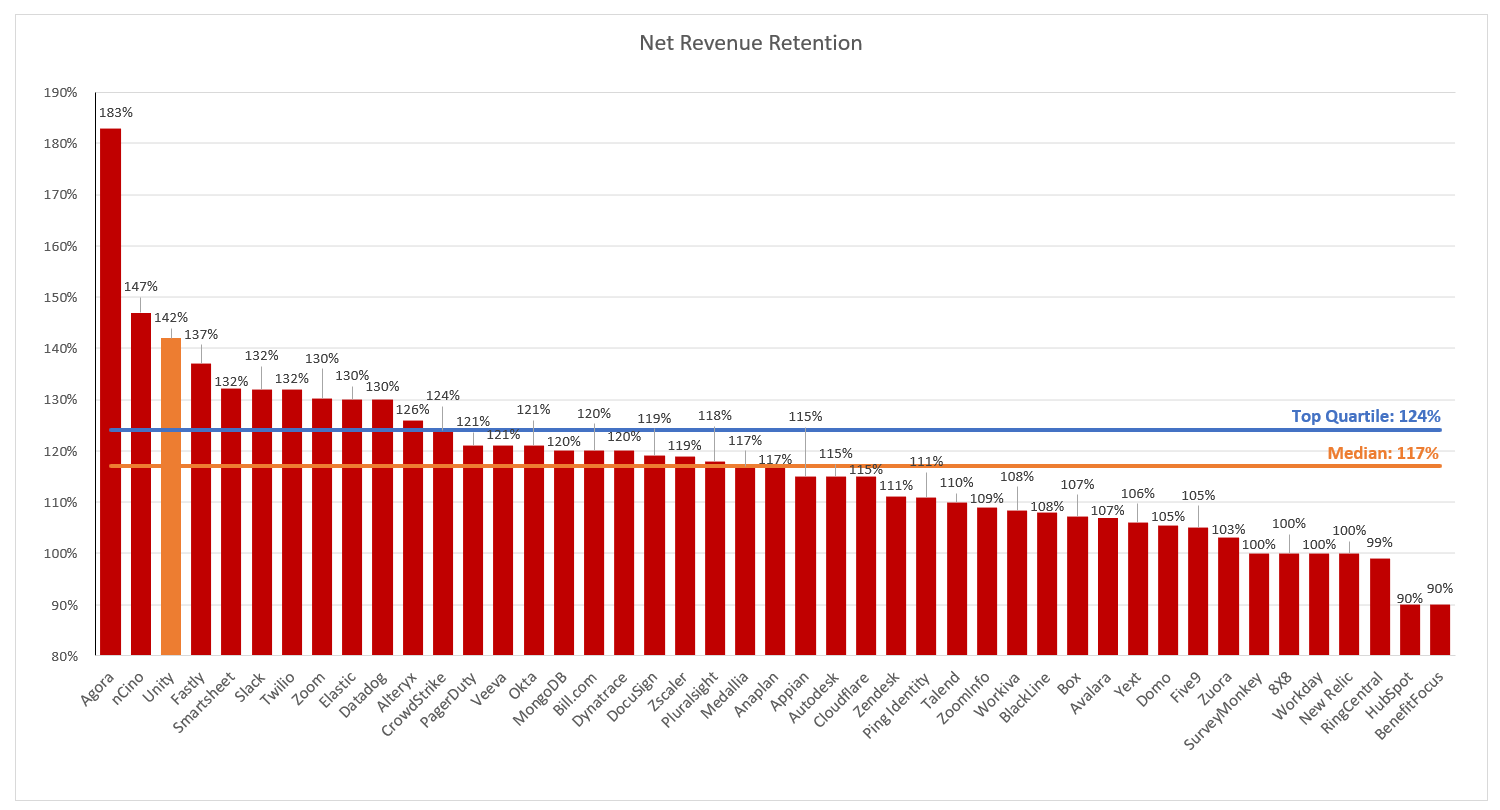

Net Revenue Retention

This metric is calculated by taking the annual recurring revenue of a cohort of customers from 1 year ago, and comparing it to the current annual recurring revenue of that same set of customers (even if you experienced churn and that group of customers now only has 9, or anything <10).

Gross Margin Adjusted CAC Payback

(Previous Q S&M) / (Net New ARR x Gross Margin) x 12. This metric demonstrates how long it takes (in months) for a customer to pay back the cost at which it took to acquire them. In the chart below I’m taking the average of the 4 quarters leading up to IPO to remove any seasonality out outliers. Normally I show this analysis, but I couldn’t find a breakout of Unity’s subscription rev vs professional services rev so am leaving out this analysis.

Valuation

Predicting the valuation of pending IPOs is nearly impossible, but it adds to the fun to make predictions! In the SaaS / Cloud world companies are valued off a multiple of their revenue. Generally this is a projected revenue number, and for the purpose of this analysis I will be looking at NTM (next twelve months) projections. When I think about what a company will be worth I first like to look at how other public companies are valued. First, let’s look at what SaaS multiples are trading at today, bucketed by growth:

Unity is a tricky one for me to predict. Up until this quarter I would have squarely pegged them in the mid tier growth bucket (for NTM revenue growth), but then revenue growth accelerated this quarter. Their net retention is also best in class (3rd highest of all public SaaS companies), but looking at their Rule of 40 (LTM growth + FCF margin) is quite unappealing (bottom quartile). My guess on this one is that a few of the other software companies to file S-1’s today will get more attention from investors when they all go public around the same time and suck the air out of the room (that hurt’s Unity). There’s also not a lot of great public comps (many of the direct comparisons like Epic Games are still private). Overall I think Unity is a very solid businesses, that will trade with a middle of the pack multiple. It’s not all truly SaaS recurring. Some of their revenue is a rev-share, and relies on their creators producing popular games (investors like more predictable subscription rev better). Overall, I’m predicting (pending any material change in multiples) - Unity will trade at ~15x NTM revenue out of the gate, giving it a valuation of $12B on the first day of trading. As a refresher for the chart below, Unity’s LTM revenue was $643M, and LTM growth was 38%