Clouded Judgement 2.6.26 - Software Is Dead...Again...For Real this Time...Maybe?

ERROR 404 NOT FOUND DNS_PROBE_FINISHED_NXDOMAIN

.

.

.

.

Just kidding…Software dying hasn’t taken down Clouded Judgement, not yet at least! Subscribe while you can, legend has it if the median software multiple dips below 3.0x then Clouded Judgement spontaneously combusts. And in the phoenix’s ashes will rise…Hallucinated Judgement, and ode to our new AI overlords. Kidding again (maybe), that will never be the name

Software Is Dead...Again...For Real this Time...Maybe

Last week I wrote a post titled “Software is Dead…Again.” Since then, IGV is down ~20% (in just 1 week!). If software was dead a week ago what is it now, down an incremental 20%?!

First - some fun stats

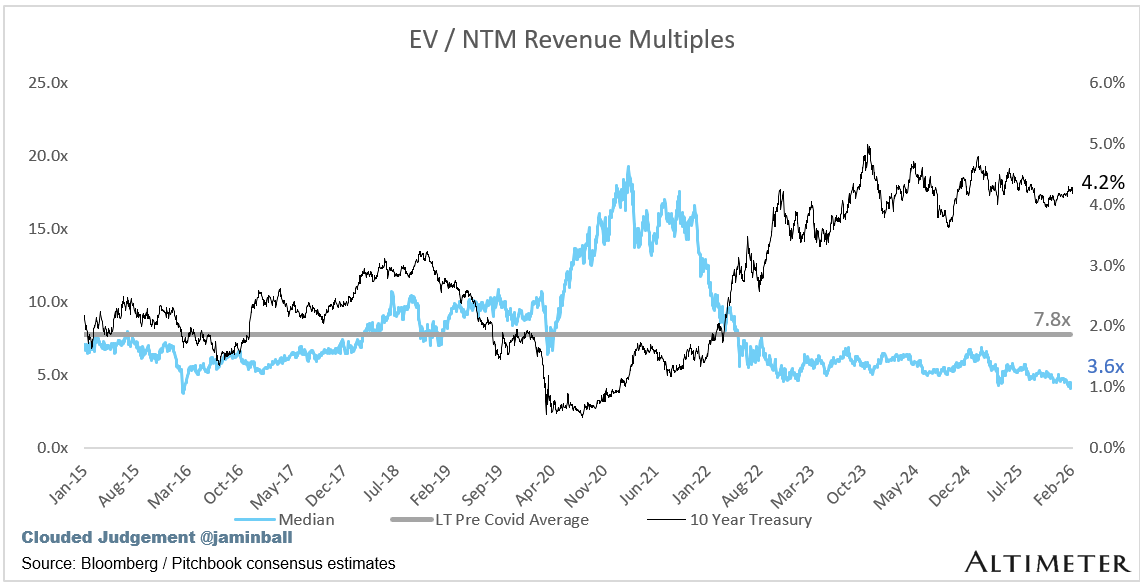

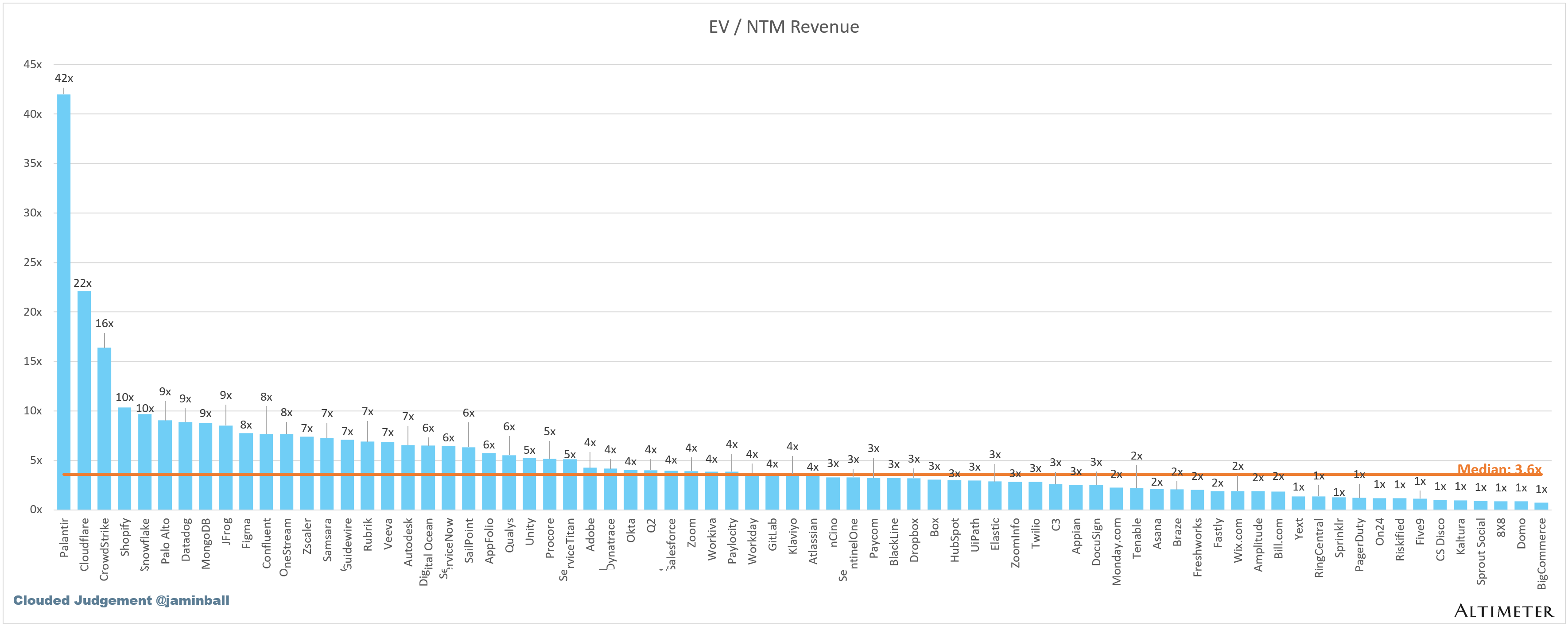

The median NTM revenue multiple (cue all the comments “he’s still talking about revenue multiples?!?”) is 3.6x. This is the lowest it’s been in the last 10+ years. For the revenue multiple haters, the median FCF multiple is 16x NTM FCF, for median growth rate of ~20% (alas, once again, cue another set of haters, saying none of the FCF is real and it’s all sitting in SBC). Can’t escape it, maybe software is a zero with no valuation support. Was good while it lasted.

39% of my software index is trading <3x NTM revenue

The median “high growth” software co is trading <10x revenue

Hyperscalers (specifically AWS and Google Cloud) CRUSHED it. Google cloud accelerated from 34% last quarter to 48% this quarter, and AWS accelerated from 20% last quarter to 24% this quarter. Their CapEx projections also exploded. Google guided to ~$180b of CapEx for the upcoming year vs estimates of ~$120b. Meta ~$125b vs estimates of $110b. Amazon $200b vs estimates of ~$150b. Microsoft is run-rating at $120b of CapEx (quarterly capex x 4). Here’s a fun tweet (chart below) showing how steep the ramp in CapEx has become.

Despite the massive ramp in expected CapEx, both Nvidia and TSM were down this week.

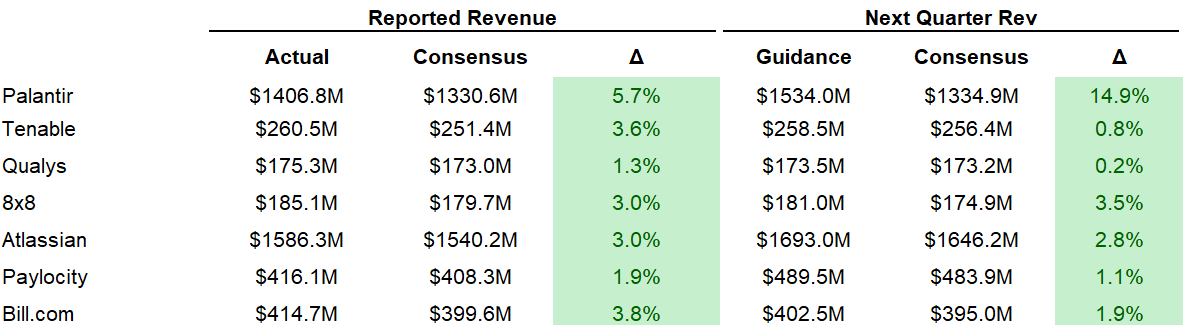

Then there’s the few software companies who have already reported earnings. ServiceNow, Atlassian, Palantir, Bill.com, Paylocity (and a few others). Results have actually been pretty solid. Median Q4 quarterly beat is 3.0%, and median guidance raise for next quarter is 2.0%. Both would be the highest mark in the last ~3 years. So far, the numbers aren’t deteriorating (but doesn’t matter, market voting machine moves quick!).

And finally there’s 8x8 - not all hope is lost. They are up ~70% in the last week. There’s always the diamond in the rough somewhere.

So how do I synthesize everything going on with public software companies? The voting machine is saying “shoot now ask questions later.” The voting machine is putting all of software in the “too hard” bucket. A new Anthropic model comes out, and the “AI will replace all software” narrative gets even more vociferous.

When I talk to software bears they say three things (among others):

They will all be vibe coded away

Classic software has hit its “late maturity” phase. TAMs have been exhausted, competition is up, and the entire industry’s growth rate will collapse, eventually to that of GDP growth, faster than most think. Because of this, the entire sector should trade on GAAP P/E multiple, like the other “late maturity” industries facing disruption.

Not only is are they late in the cycle, but they also won’t capture any “AI revenue.” They won’t innovate fast enough, and can’t attract the right talent to innovate. All future growth in software will come from AI agents, none of which the legacy SaaS providers will capture.

Operationally, they’re run terribly. SBC is rampant, and is a way of enriching insiders at the expense of shareholders. They all have way too many employees and operate very inefficiently (relative to how they could operate)

When I talk to software bulls they say in response:

Good luck vibe coding a system or record. Good luck vibe coding the classic “enterprise” features like RBAC, SSO, audit logs, data residency, SOC2 (and all other security certifications), audit reporting, etc. Good luck encoding all business logic and edge cases (what has taken the classic systems of record years to accumulate). Good luck offering support to your internal users. Good luck maintaining / upgrading / keeping up with the latest best of breed tech. And if you actually are able to do all of this, good luck doing it in a way that has a total TCO lower than just buying the original piece of software from a vendor…At the end of the day, companies aren’t in the business of building internal tools, they’re in the business of selling solutions to customers.

Software isn’t in it’s late cycle, it’s no where close (as an industry) to growing at the same rate as GDP growth, it’s way less cyclical than other industries, so still should trade at mor premium multiples

Existing players have a distribution and trust advantage, already being installed in the largest enterprises. They’ll capture the agents revenue, or at least their fair share

Ya, the bears probably right on point 4. For the most part these companies are run inefficiently, and all the SBC is quite the scheme.

Where do I sit? Personally I don’t think the “vibe code” risk is real…at all…At least not in the short term. I will acknowledge that it’s really hard to predict what the future looks like. And these models improve SO quickly. So what seems impossible to vibe code today will be entirely possible a year from now (and much more). The rate of change is extraordinary. I think it’s naive to underestimate the possibilities of what vibe coding will be able to achieve a year from now (let alone 2-3 years from now). But, I don’t think the overall attitude of “let’s build internally vs pay someone to manage internal software” will change…We’ll always settle on companies outsourcing internal software to vendors (be it legacy SaaS or new AI native startups).

What I do believe - there’s real “front door” risk. I wrote about it here in December. In summary, classic software could be reduced to something that looks more like middleware with agents capturing all of the incremental value on top of them. I mean, look at this graphic from OpenAI…It’s screaming “the classic system of records will be pushed down the stack.” The system of record is literally at the bottom…Down the stack = lower growth potential, and smaller profit pool to capture.

In this world, which I believe we will get to eventually (but the path from here to there is probably longer than what the market is pricing in, but sooner than most industry critics think…), the next growth vector of software won’t be captured by legacy cloud software businesses. And I don’t mean this in an absolute. Some value will, but most (vast majority, I think) of the incremental AI value created in software will go to agents. Incumbents just move to slow. Can’t attract the best talent (what great AI engineers want to work for a legacy company vs cutting edge startup?), have innovators dilemma, have to evolve their business models, etc. Said another way, expansion revenue will be MUCH harder to come by. There will be a small percentage of “legacy SaaS” companies that innovate and capture this new S-Curve. Maybe 10%. The rest won’t…But, not capturing

But, this doesn’t mean the doom of software is at our doorstep…Not capturing the next phase shift of explosive growth doesn’t mean that all growth disappears…I do think there is still a lot of growth left in classic cloud migrations. I was talking to the CEO of a very large business this week. They recently started a migration to SAP. The way they described this migration: I know SAP isn’t a modern company by any stretch, let alone an AI company, but what else was I going to do? There are no “AI-native SAPs.” And I’m not going to have my engineers building out our own SAP. I hear this sentiment all the time.

Said another way, I don’t think we’re necessarily “late cycle” of the cloud software market…I still think there is tons of room for classic cloud migrations. So I don’t think we can call cloud software a melting ice cube, yet. However, maybe the AI native co’s end up stealing the “first” cloud migrations for the industry laggards (that would be an anti-pattern, the laggards will probably not jump straight to AI native challengers).

The other reality - software has a longgggg half life…It takes a long time to “kill.” maybe this is why we’re on the “Software is Dead…Again…Again” blog post title. The software cat has lost 3 of it’s 9 lives! But it’s still alive. For now. With a few lives left.

So the right question - what is the right multiple now for this industry? A “not yet a melting ice cube, but future growth prospects look hampered, and more terminal risk with lots more uncertainty.”

Well, it’s certainly deserves a lower multiple than where it was! When uncertainty goes up, the discount rate must follow. And the uncertainty is WAY up. Dust hasn’t even come close to settling yet.

I do think growth prospects have changed. The voting machine sure believes it. I think it’s gone too far. But at the same time I think some of software universe is still over-valued. There will (could) be some epic returns from here if you pick the 10% who become more of an “AI winner” who can avoid being pushed down / reduced to middleware. Those looking at my multiple charts and saying “but the pre-covid average multiple was 8x NTM rev, we’ll bounce back eventually” will probably be disappointed. If we ever get back there (as an industry median) it will probably be because a new crop of “AI native Agent” companies in hyper growth mode go public and bring the median up. The basket of existing cloud software companies may never get back to a median of 8x NTM rev (mark that statement in case we do, and this is the bottom!)

We can analyze and debate this until we’re blue in the face, but the reality is uncertainty up, discount rate up (I’ll stop beating that dead horse).

If you want a “top line” (revenue, gross profit, etc) vs a “bottom line” (earnings, FCF) valuation metric, you have to be operating in hyper / high growth - because the assumption is if you (and the industry) is in (hyper) growth mode, then you’re early in the S-Curve. The only way top line valuation metrics can ever make sense is if you can grow fast enough to eat the multiple compression that will inevitably come as the industry matures and re-rates. Either that, or the market will just always place high multiples on industries early in a cycle :) We did value internet companies on a multiple of users / eyeballs at one point!

So the question becomes - will legacy SaaS co’s re-enter growth mode and capture a new S-Curve of growth with agents? Will their growth fall off a cliff as agents eat their lunch and turn them into middleware? Time will tell. There will be dispersion. Good luck! For those who don’t capture the AI Agent tailwind, their “death” will probably happen much slower than people think. For those who do, it’s been an elevator down, and will be a slow escalator up. Takes a while for the market to rebuild confidence in an entire sector.

In summary - I think the market is getting it wrong in the short term. These companies have stronger moats and will be more resilient than anticipated. However, I think the market is probably right in the long term. Agents will create a ton of creative disruption, hamper expansion revenue of legacy vendors, and history is against the incumbents capturing this new vector of hyper growth.

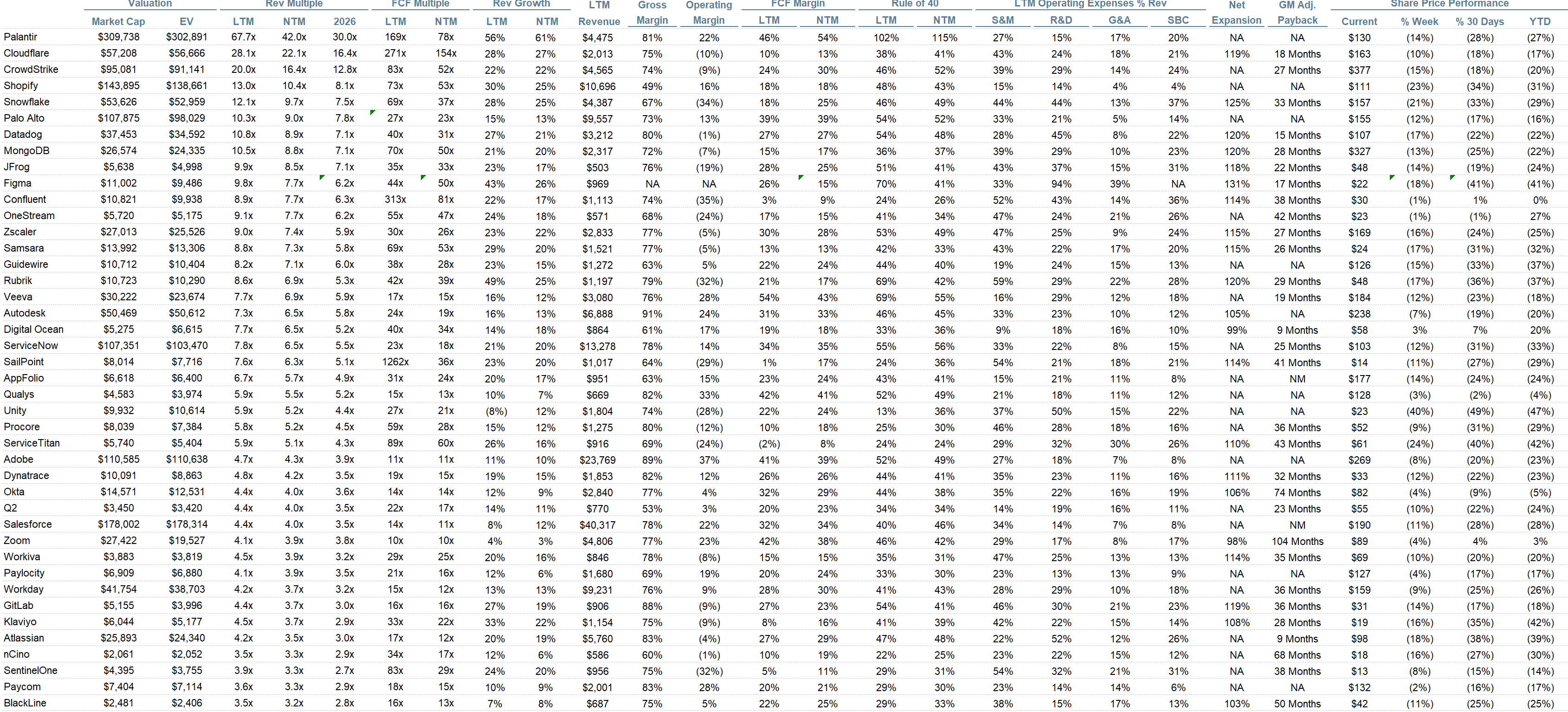

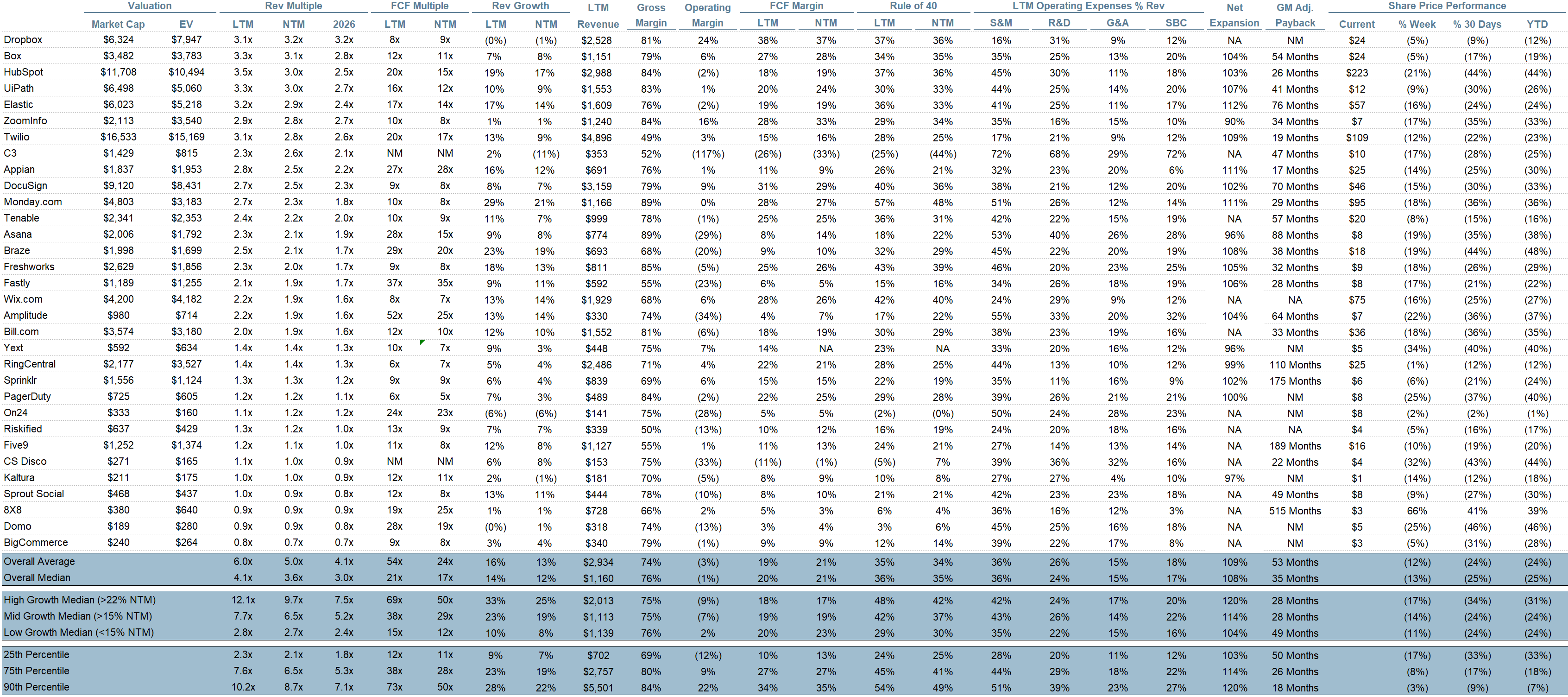

Quarterly Reports Summary

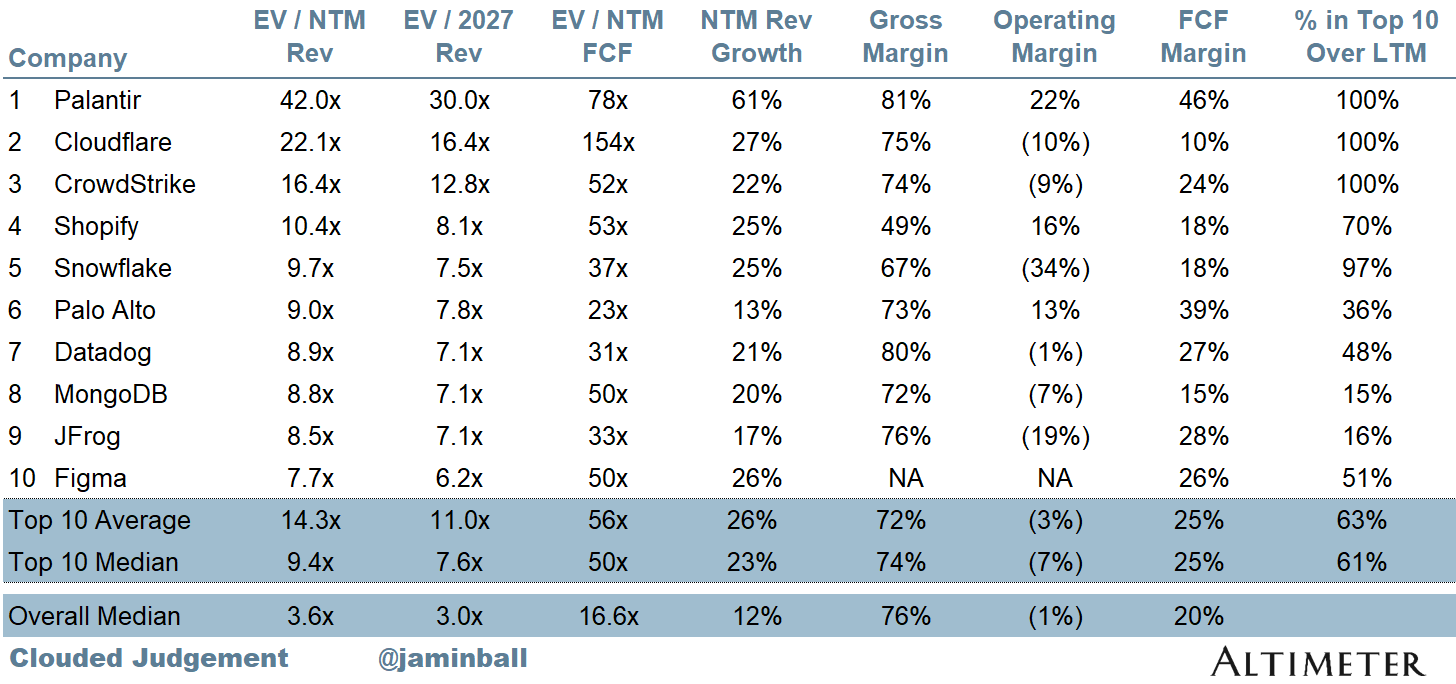

Top 10 EV / NTM Revenue Multiples

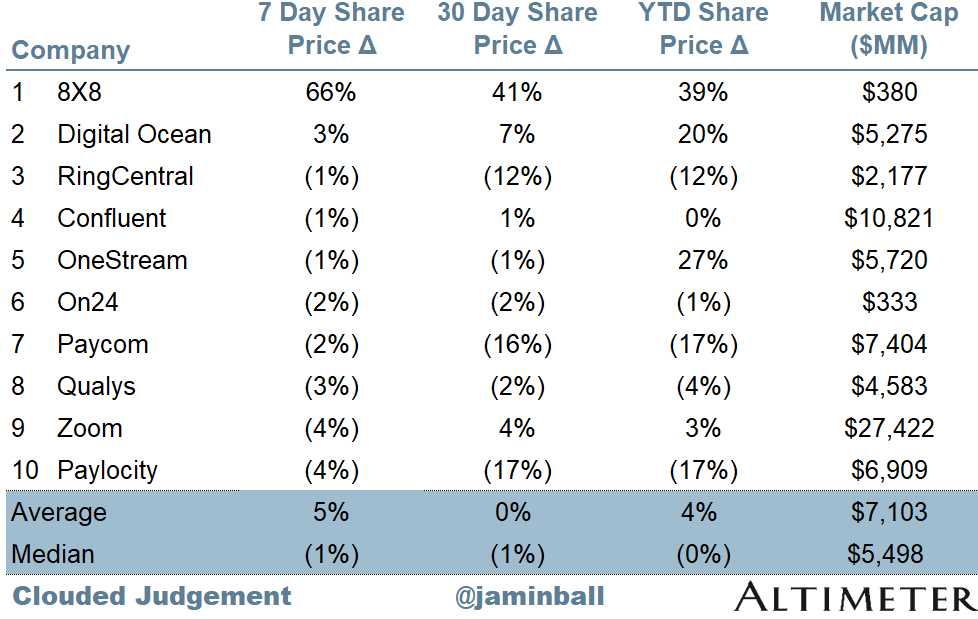

Top 10 Weekly Share Price Movement

Update on Multiples

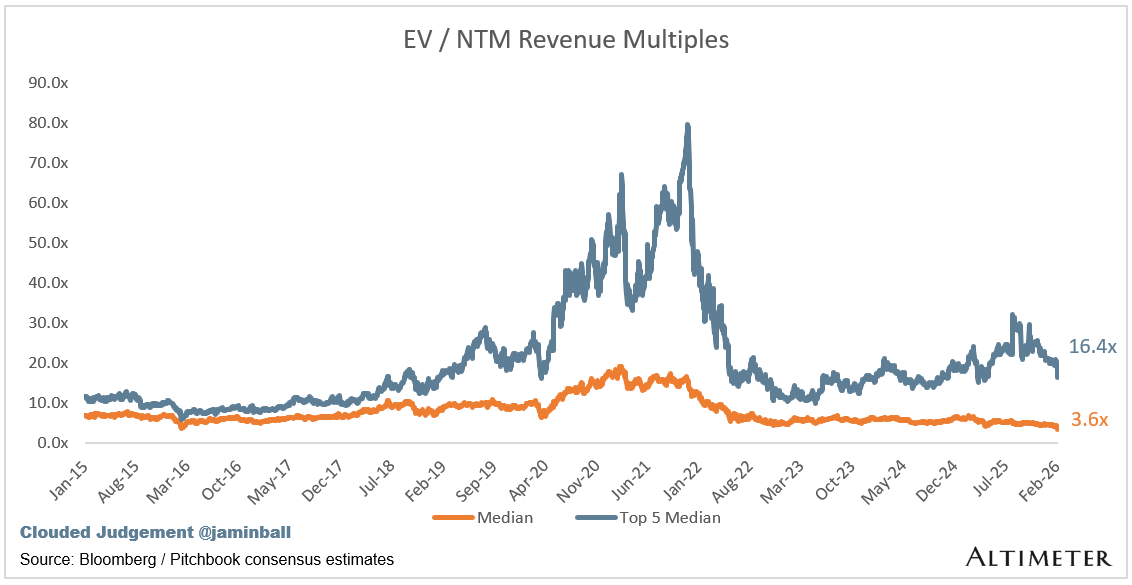

SaaS businesses are generally valued on a multiple of their revenue - in most cases the projected revenue for the next 12 months. Revenue multiples are a shorthand valuation framework. Given most software companies are not profitable, or not generating meaningful FCF, it’s the only metric to compare the entire industry against. Even a DCF is riddled with long term assumptions. The promise of SaaS is that growth in the early years leads to profits in the mature years. Multiples shown below are calculated by taking the Enterprise Value (market cap + debt - cash) / NTM revenue.

Overall Stats:

Overall Median: 3.6x

Top 5 Median: 16.4x

10Y: 4.2%

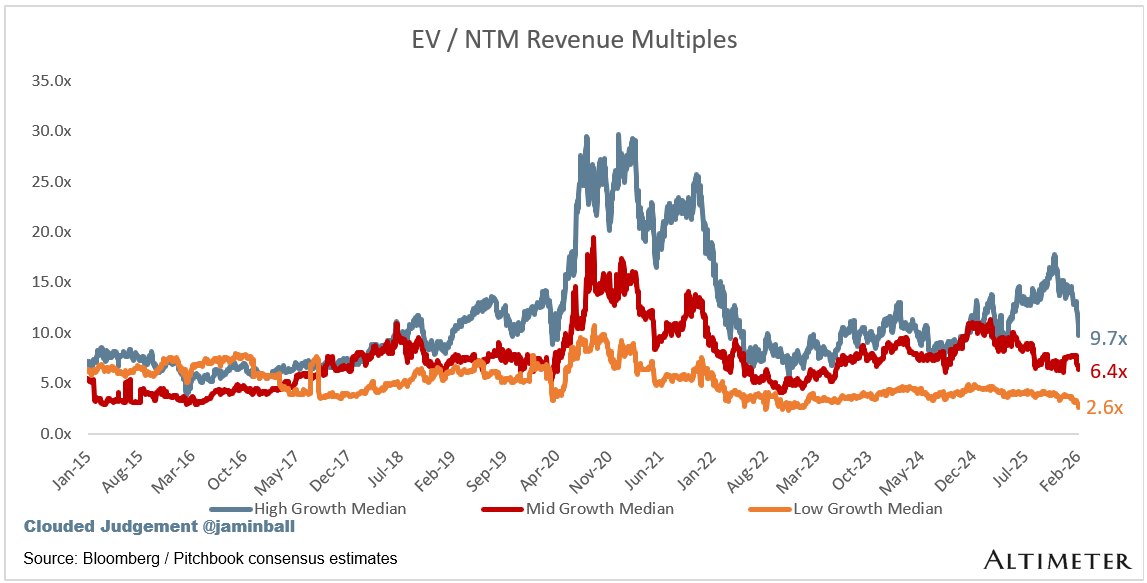

Bucketed by Growth. In the buckets below I consider high growth >22% projected NTM growth, mid growth 15%-22% and low growth <15%. I had to adjusted the cut off for “high growth.” If 22% feels a bit arbitrary, it’s because it is…I just picked a cutoff where there were ~10 companies that fit into the high growth bucket so the sample size was more statistically significant

High Growth Median: 9.7x

Mid Growth Median: 6.4x

Low Growth Median: 2.6x

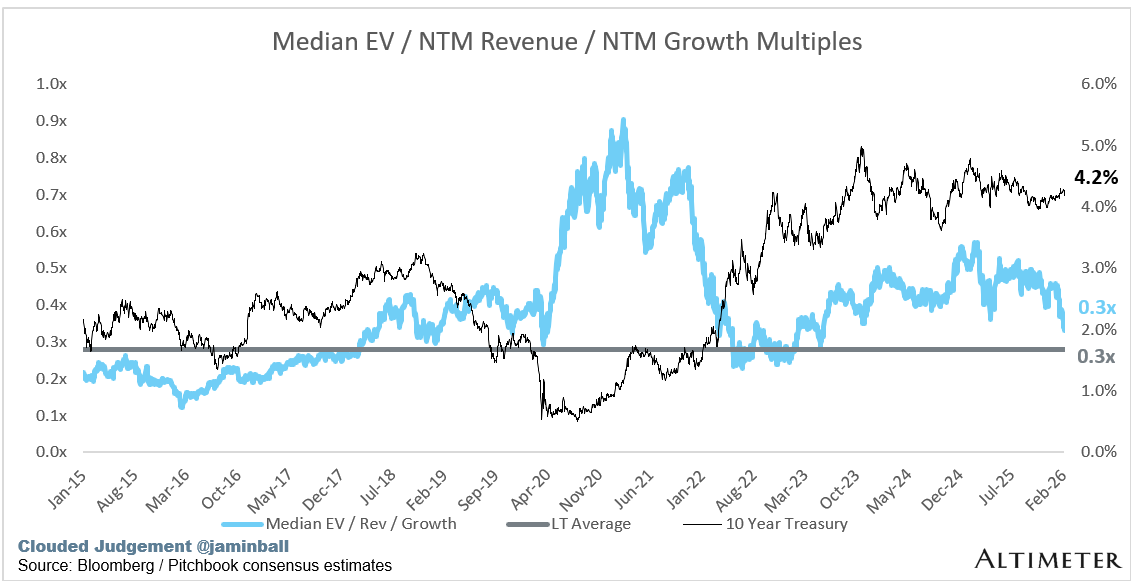

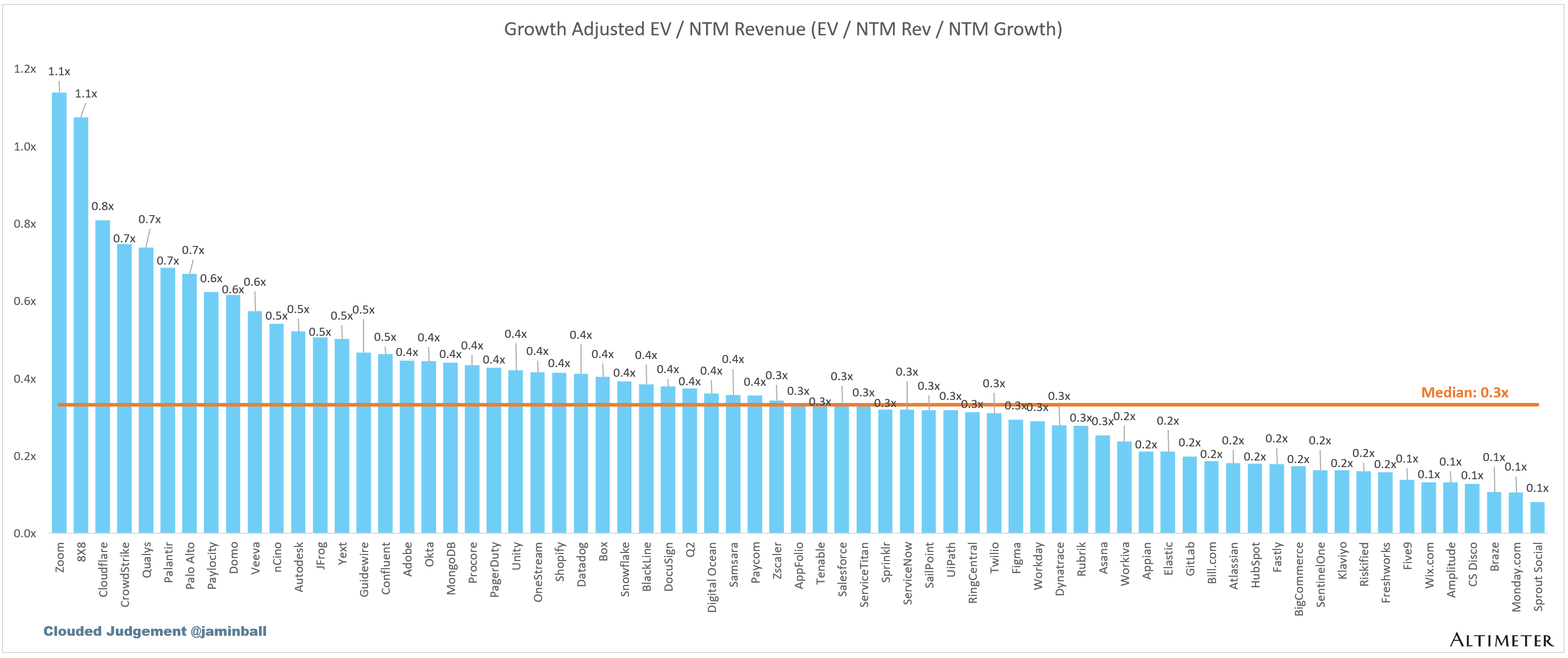

EV / NTM Rev / NTM Growth

The below chart shows the EV / NTM revenue multiple divided by NTM consensus growth expectations. So a company trading at 20x NTM revenue that is projected to grow 100% would be trading at 0.2x. The goal of this graph is to show how relatively cheap / expensive each stock is relative to its growth expectations.

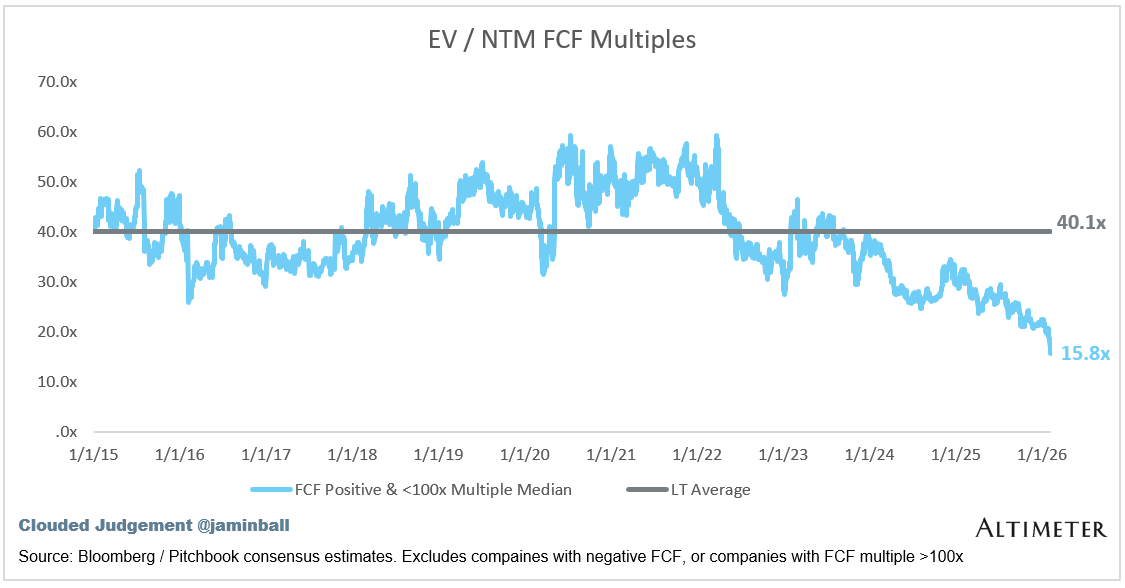

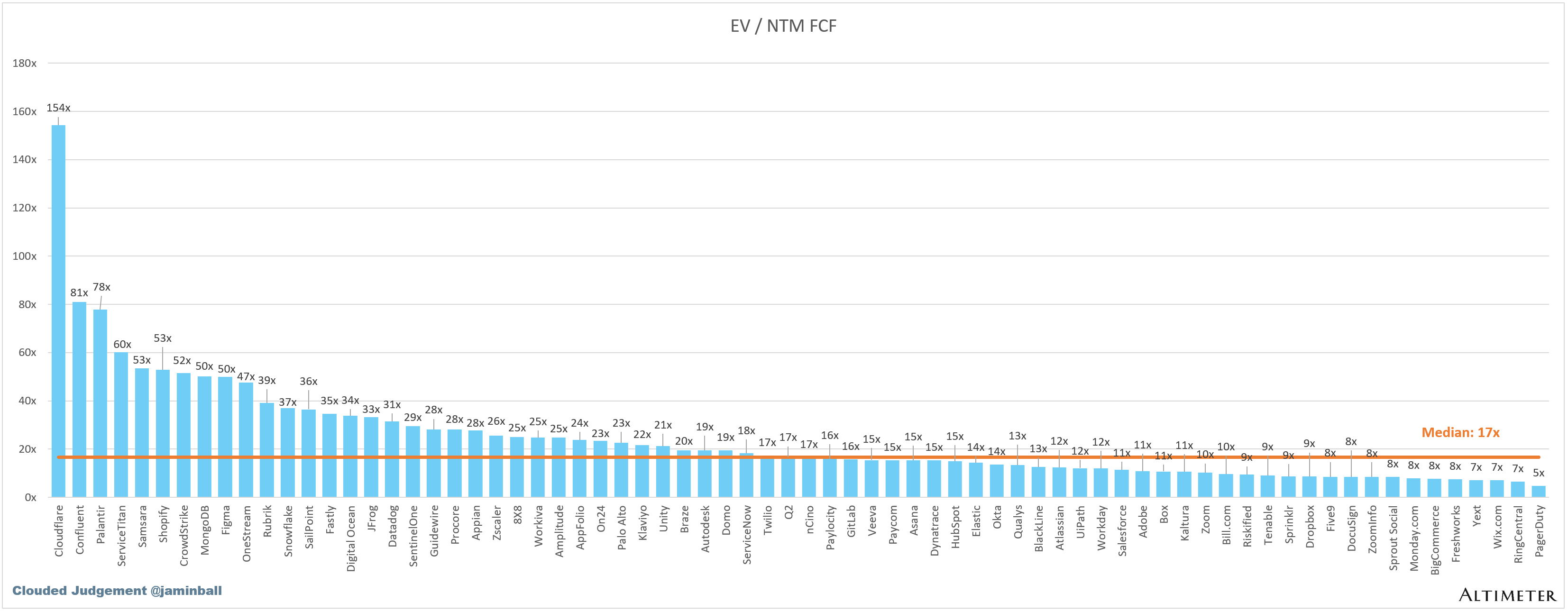

EV / NTM FCF

The line chart shows the median of all companies with a FCF multiple >0x and <100x. I created this subset to show companies where FCF is a relevant valuation metric.

Companies with negative NTM FCF are not listed on the chart

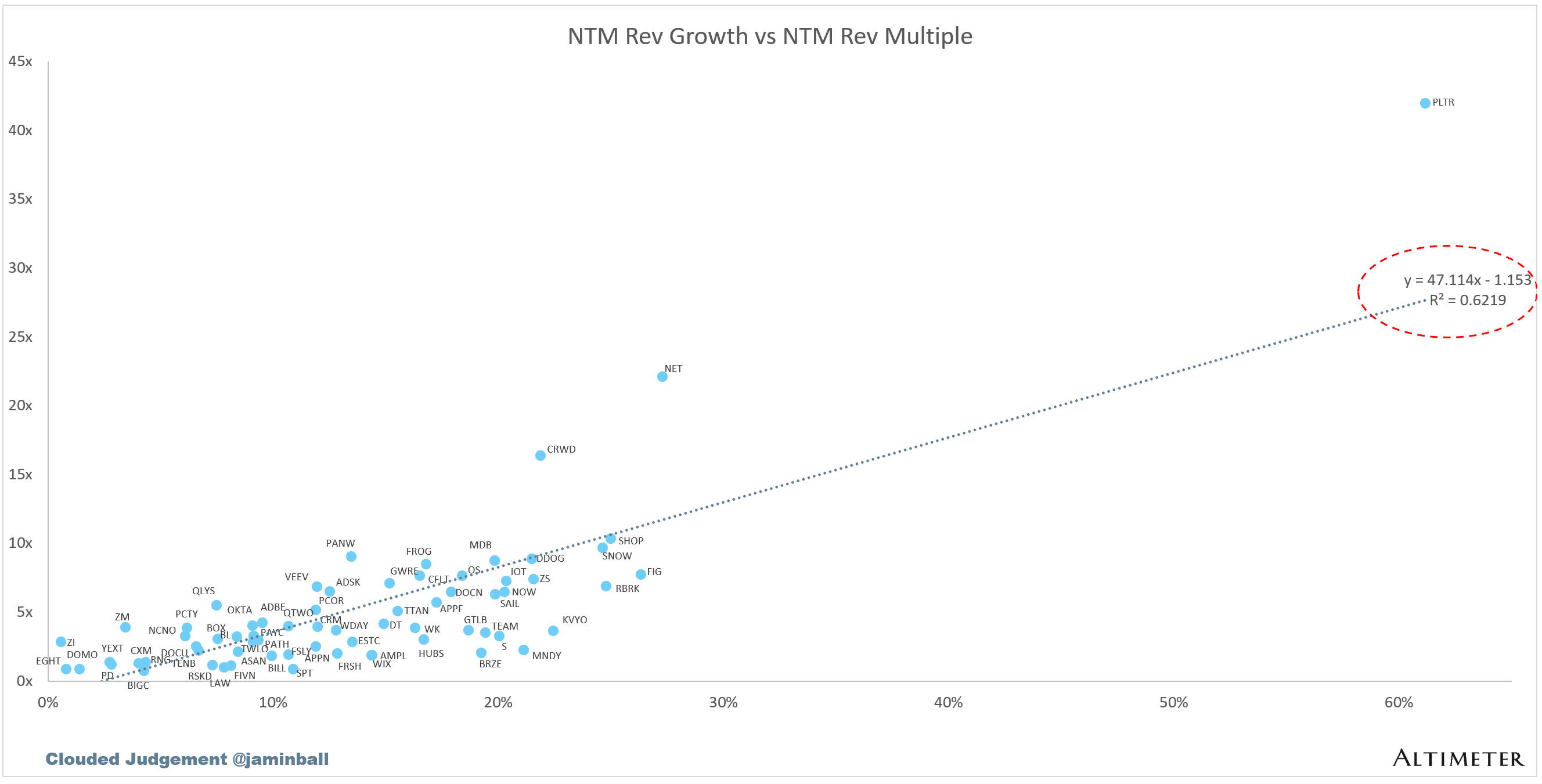

Scatter Plot of EV / NTM Rev Multiple vs NTM Rev Growth

How correlated is growth to valuation multiple?

Operating Metrics

Median NTM growth rate: 12%

Median LTM growth rate: 13%

Median Gross Margin: 76%

Median Operating Margin (1%)

Median FCF Margin: 19%

Median Net Retention: 108%

Median CAC Payback: 36 months

Median S&M % Revenue: 37%

Median R&D % Revenue: 23%

Median G&A % Revenue: 15%

Comps Output

Rule of 40 shows rev growth + FCF margin (both LTM and NTM for growth + margins). FCF calculated as Cash Flow from Operations - Capital Expenditures

GM Adjusted Payback is calculated as: (Previous Q S&M) / (Net New ARR in Q x Gross Margin) x 12. It shows the number of months it takes for a SaaS business to pay back its fully burdened CAC on a gross profit basis. Most public companies don’t report net new ARR, so I’m taking an implied ARR metric (quarterly subscription revenue x 4). Net new ARR is simply the ARR of the current quarter, minus the ARR of the previous quarter. Companies that do not disclose subscription rev have been left out of the analysis and are listed as NA.

Sources used in this post include Bloomberg, Pitchbook and company filings

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP (”Altimeter”). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

The challenge with the "most SaaS is untouchable if it's a system if record" is that essentially we are saying we are fine with being the COBOL and mainframes of the technical transition to AI native software.

This is also often where the technical understanding of most investors shows it's limitation - the power of coding models like Opus 4.6 is not just coming up with new stuff, but utilizing existing (mostly open source) tools and frameworks. If the so called vibe coded CRM is built on top of a widely supported open source relational database, the ability to protect that data and move it to alternative architecture if required is much higher.

Now add in the concept of "skills" which essentially is premade template of things the model will do to set these systems up, and the "SaaS killer" becomes very much a reality for many use cases.

Is not the main business case of SaaS is basically to enable workflows through the cloud and deliver it to clients CHEAPER than legacy on premise systems. The trick is that that cheap revenue is valued much much much higher than the old model. Hence, everyone and ttheir granmoms are in the SaaS business last 10-15 years punting like bandits.

Now, here we are, in a new junction, where the AI is offering you a completely natural language UI, doing all the complex tasks behind the scenes and then able to do it nonstop, factory like fashion. Now, anyone who defends SaaS or its legacy "system of record", "impossible to replicate" ya da ya da are either delusional or they dont remember how we come here from the days of mainframes to pre-internet era legacy set-ups.

Just think about what happened to print media with internet in early 2000s or, linear tv with VOD. I think everything we know about SW world will inevitable change and change fast, dramatically.